Influential academics reveal how China can achieve its ‘carbon neutrality’ goal

Lauri Myllyvirta

10.14.20Lauri Myllyvirta

14.10.2020 | 4:52pmChina’s electricity system would need to reach net-zero CO2 emissions by 2050 if the country is to meet its recently announced target of “carbon neutrality” before 2060.

This is one of the key insights from new scenarios and policy recommendations for meeting the goal, published separately by two leading – and highly influential – Chinese climate research institutes.

The scenarios hint at the thinking behind Chinese leader Xi Jinping’s announcement and offer a glimpse of what it might mean for the energy system in China – and the world. China accounts for almost 30% of the world’s CO2 emissions, more than half of its coal use and half of coal-fired power capacity.

Both scenarios come close to phasing out fossil fuels, with more than 85% of all energy and more than 90% of electricity coming from non-fossil sources – renewables and nuclear – by 2050.

The energy pathways unveiled since the goal was announced on 22 September show how the thinking on China’s future energy system is already shifting, but also highlight some of the questions that are still left open by the one-sentence announcement, where, according to the official translation, Xi said: “We aim to have CO2 emissions peak before 2030 and achieve carbon neutrality before 2060.”

New scenarios

The first of the new scenarios is from Tsinghua University Institute for Climate Change and Sustainable Development (ICCSD) and 18 other Chinese research institutes, which released their “China Low-Carbon Development Strategy and Transformation Pathways” (presentation, English) on 12 October.

Meanwhile, Prof Zhang Xiliang of Tsinghua University’s Institute of Energy, Environment and Economy (Tsinghua 3E) recently gave a presentation (in Chinese, starting from 3:46) on the energy and economic implications of reaching carbon neutrality by 2050, 2060 or 2070, which appears to have informed the 2060 target date.

Both scenarios indicate that the electricity sector would need to get to zero emissions by 2050 and start delivering “negative emissions” thereafter – assumed to come from bioenergy with carbon capture and storage (BECCS) – to offset hard-to-eliminate emissions from industrial processes, agriculture and other sectors.

The Tsinghua 3E scenario foresees power generation from coal without carbon capture and storage (CCS) essentially ending in 2050, but it maintains a significant amount of coal use outside the power sector until 2060. In the ICCSD scenario, the share of coal in the overall energy mix already falls below 5% in 2050.

The phasing out of fossil fuels means that more than 85% of all energy and more than 90% of electricity should come from non-fossil energy – renewables and nuclear – by 2050.

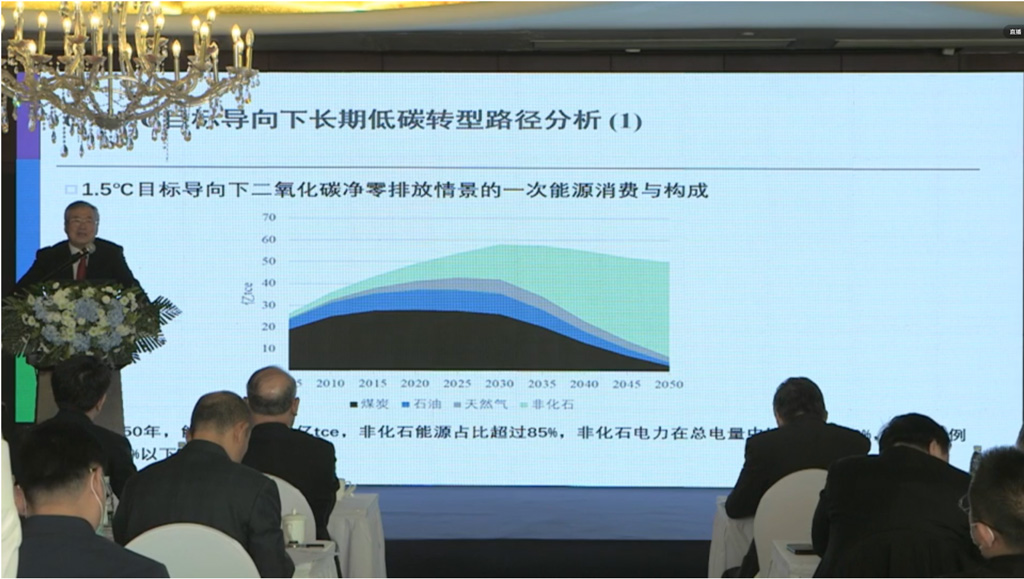

Tsinghua University’s Prof He Jiankun presenting the evolution of China’s total energy demand and energy mix under the 1.5C emission pathway at the release event of the “China Low-Carbon Development Strategy and Transformation Pathways” on 12 October (black: coal, grey: oil, light blue: fossil gas, green: non-fossil energy). Source: Screen capture from Tsinghua’s presentation live-stream.

Higher ambition

The 2060 announcement is clearly creating room for more ambitious energy plans. This becomes clear when comparing the latest scenarios towards 2060 with earlier projections.

For example, last year’s China Renewable Energy Outlook 2019 by the National Renewable Energy Center – a thinktank under China’s top economic planning ministry the NDRC – saw non-fossil energy reaching only 65% in 2050. Yet this annual report has a history of presenting a bullish case for renewables.

In the new scenarios, the main strategy for phasing out fossil fuels outside of the power sector is electrification, which means that emissions-free power generation will need to replace not only China’s coal-fired power plants – half of the world’s total – but also much of the coal and oil consumption in industry, transport and heating sectors.

Delivering the energy needs of the world’s largest energy consuming economy from non-fossil sources appears a huge undertaking.

Based on Tsinghua 3E’s work, it means growing China’s solar power capacity about 10-fold and wind and nuclear power capacity seven-fold by 2050. At that point, China would have more than four times as much solar power capacity and three times as much wind power capacity as the entire world has today, while nuclear power capacity would reach 80% of the current global total.

However, what is striking about the scenarios is that the actual increase in rates of clean energy uptake are quite modest, given the scale that the industry has already reached in China.

Solar and wind power installations would need to almost double, while nuclear growth would need to more than double over 2020-2050, compared with the 2016-2020 period.

The Tsinghua 3E sees total energy consumption peaking by 2035, after which the growth in clean energy would go entirely towards displacing existing fossil fuel use. This would be in contrast with the dynamic so far, with emissions increasing in spite of the increasing share of clean energy, due to rapid growth in overall energy demand.

Highlighting the role of electrification, in the ICCSD scenario that is estimated to be in line with a global temperature target of 2C, essentially all energy-sector investment goes towards electricity.

Both sets of scenarios find that getting to a 1.5C compatible pathway – and to carbon neutrality – requires significant investment in negative emissions from the power sector, which they plan to realise with biomass CCS (BECCS).

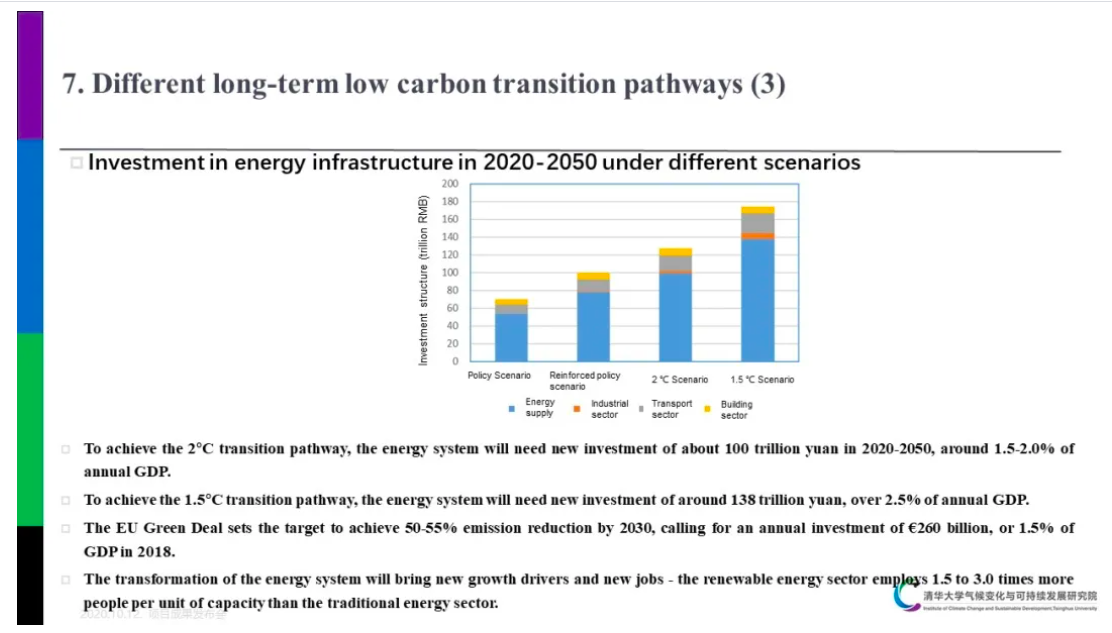

The ICCSD 2C scenario requires investment of RMB100tn ($15tn) between 2020 and 2050, This is 1.5-2.0% of China’s GDP over the period, which the researchers argue is similar to the investment required in the EU to meet a target of reducing emissions by 50-55% by 2030. Required investment increases to RMB140tn ($21tn) in the 1.5C pathway.

A slide from the ICCSD presentation where energy infrastructure investment under different emission pathways is compared to investment required under the EU’s 2030 emissions goals in terms of ratio to total GDP. Columns left to right: current policies; strengthened Nationally Determined Contribution; 2C emission pathway and 1.5C emission pathway (Orange: electricity, blue: carbon capture and storage (CCS), yellow: oil, gray: gas.) Source: ICCSD.

Crucial details

Comparison of the different projections also highlights the importance of some crucial details that are still open to interpretation.

Different assumptions about which emissions are included in the pledge and how much CO2 can be taken up by ecosystems, or removed using negative emissions technologies, lead to widely varying budgets for energy-sector emissions.

Optimistic assumptions about CO2 removal from afforestation would leave more space for residual fossil-fuel emissions, as highlighted by remarks from an environment ministry researcher.

Another important question is whether the target covers only CO2 or all greenhouse gases (GHGs). Energy sector emissions would likely need to fall faster and deeper if the latter is the case, as some of the sources of the other GHGs are hard to eliminate.

The ICCSD scenario is relatively ambitious among the different projections, in part because the researchers interpreted the target to include all greenhouse gas emissions.

But, according to China Dialogue, which cites “one expert close to China’s policy on non-CO2 greenhouse gases”, this interpretation remains an assumption by the researchers at ICCSD rather than an official government position.

Challenges

The Chinese economic model is very good at mobilising large amounts of investment, so scaling up clean energy, electrified transport and other new, clean technologies might not be the largest challenge in reaching carbon neutrality by 2060.

Instead, managing the economic, regional and political impacts of phasing out fossil fuels is likely to be a bigger issue for the country.

By 2050, in the ICCSD low-carbon development pathway, coal would supply less than 5% of China’s energy – and much less than 10% in the power sector. This would mean closing down all but a few of the 3,000 coal-fired power units and 5,000 coal mines operating in China today.

Coal-fired power plants would close at an average age of 30 years. This is in line with the experience so far in China – more than half of the capacity built in any year before 1990 has retired already, indicating an average plant life of 30 years. However, for any new projects permitted this year or in the coming years, 2050 is starting to draw close.

A demonstration of the challenge was seen when China’s coal consumption and CO2 emissions started to fall in 2013 to 2015, as the effect of stimulus measures wore out.

The leadership’s initial response was to brand the development as a part of a transition to a new economic model – the “New Normal”. By 2015, however, financial distress was building up at state-owned mining and smokestack industry enterprises. Rather than put these firms through a restructuring, the government responded with even more stimulus.

The fallout might be even more dramatic for overseas economies depending on fossil-fuel exports. China’s new economic policy of “dual circulation” (reducing its reliance on overseas markets and technologies) and new emphasis on energy security mean ever greater efforts to replace imports with domestic supply.

Combined with the carbon-neutrality pledge driving down demand for fossil fuels, along with heavy investment in domestic coal, oil and gas production and transport, this could mean a very rapid exit from fossil-fuel imports.

It is also clear that realising the carbon-neutrality vision will require work on deep decarbonisation options in sectors that are currently viewed as “hard to address”, particularly steel, cement and chemical industry process emissions, as well as agriculture and aviation.

These initial studies take a simplified approach and assume that BECCS will be an easier or more affordable solution than decarbonising these sectors, but more affordable mitigation options could emerge.

For its part, the ICCSD main report will be followed by no less than 17 sectoral reports diving deeper into the possible solutions. ICCSD’s policy recommendations and the environment ministry’s statement on the 2060 target call for key industrial sectors to take action towards peaking emissions during the next five-year plan period (2021-25).

Ambition gap

ICCSD also gives recommendations for upgrading China’s commitments under the Paris Agreement. The recommendations include committing to no further CO2 emission growth from 2025 onwards, one step short of an emissions “peak”.

In practice, this would mean setting a cap on total emissions at 10.5bn tonnes. The institute also recommends increasing China’s non-fossil energy target to 20% by 2025 and 25% by 2030 (from 15.3% in 2015).

It also says the five-year plan’s targets for 2025 should include peaking coal consumption and strictly controlling new coal power capacity.

One potentially important proposal for the next five-year plan is to set CO2 peaking targets for energy-intensive industrial sectors and key cities, to enable the national peak later on.

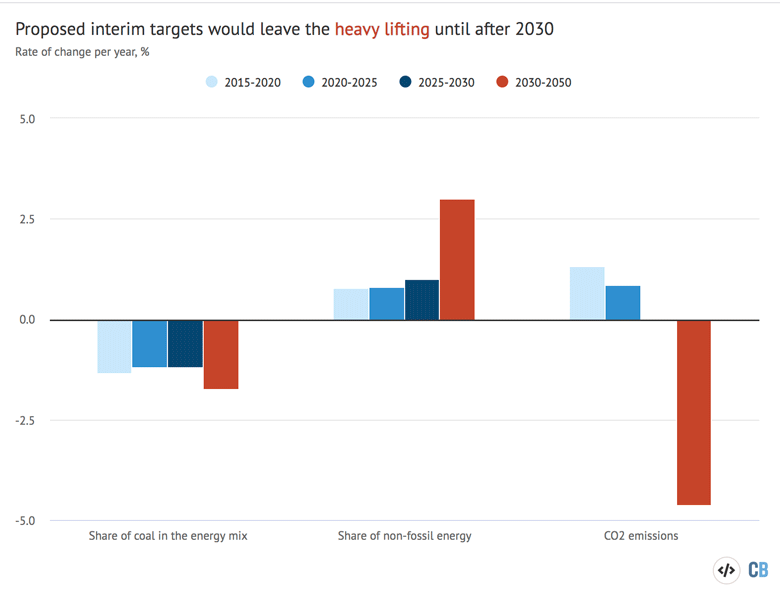

However, under the proposed cap on CO2, emissions would still increase by 4% from 2020 to 2025, almost 1% per year. The researchers recognise that continued increases in CO2 emissions from China are not in line with the 1.5C or 2C targets, but argue that “inertia” in the system means the country will fall behind those goals and will have to catch up later.

Under the Tsinghua proposals of 20% non-fossil energy in 2025 and 25% in 2030, non-fossil energy would be increasing at the same rate as China has to date – about 1 percentage point per year. Thereafter, throughout the 2030-2050 period, non-fossil energy would have to increase three times as fast, at three percentage points per year.

Similarly, the growth in CO2 emissions would slow down only slightly from 1.5% per year in 2015-2020 to 1% in 2020-25 and then stop in 2025-30. After that, emissions would have to fall by around 4% per year to reach net-zero by 2060.

Therefore, adapting China’s near-term targets, policies and commitments to the long-term goal will remain challenging – or else the bulk of the effort required to reach carbon neutrality will be left for the following decades, as shown in the chart below.

All eyes on China

Presenting ICCSD’s findings, Prof He Jiankun, chair of the ICCSD academic committee and deputy director of China’s Advisory Committee on Climate, noted that China’s 14th five-year plan is attracting a lot of attention internationally as the country’s success in controlling Covid-19 is allowing the economic recovery to start earlier than other countries.

Xi Jinping has also emphasised the importance of a green recovery from the crisis. If such a green recovery is translated into domestic policy action, then it could put the country on the path to carbon neutrality much faster. [Carbon Brief is tracking how governments around the world are introducing “green recovery” stimulus measures.

There is also the possibility that the energy targets for the upcoming five-year plan could be revised after Xi’s announcement to reflect the increased long-term ambition. While the plan is only due to be published in 2021, the drafting process had been gravitating towards targets that are close to what the Tsinghua researchers proposed.

Research on cost-optimised emissions reduction strategies suggests that a more linear path towards the 2060 target would be economically optimal (see e.g. IPCC special report on 1.5 degrees), not to mention more credible to the outside world. Furthermore, targets championed by Xi personally tend to be overachieved by the government and wider bureaucracy.

Therefore, there are multiple factors that could lead to a faster shift in emissions trends, as different parts of the economic planning machinery, local governments and state-owned enterprises chart their own pathways to realising the overall 2060 vision.

-

Influential academics reveal how China can achieve its ‘carbon neutrality’ goal

-

New research sheds light on thinking behind China’s ‘carbon neutrality’ goal