China is the world’s largest emitter of greenhouse gases. Historically, it has been reluctant to cut emissions, fearing that doing so could impede its economic growth. But there are signs that position is shifting.

Late last year, the government banned the building of new coal power plants in particular areas due to air pollution concerns. Now it has announced it will seek to implement a national carbon market by 2016.

The announcement wasn’t much of a surprise. Since 2011, China has been developing seven pilot carbon markets with the aim of one day creating a national scheme. The National Development and Reform Commission – the department responsible for the schemes – has long said it wants to include plans for a national market in China’s next five year plan.

But could a carbon market form the backbone of China’s response to climate change?

Rationale

China has pledged to reduce the carbon intensity of its economy – the level of greenhouse gas emitted for each Yuan of GDP generated – by 40 to 45 per cent. That means its economy is destined to become more efficient, but doesn’t guarantee an overall emissions cut.

The government is putting a range of policies in place to help hit that goal. It’s now clear a carbon market is also part of the plan.

China has been relatively slow to jump on the carbon market bandwagon. The EU’s emissions trading scheme (ETS) – the world’s largest – was set up in 2005. There are now 46 carbon markets operating worldwide, including China’s.

The basic principle behind all the schemes is that polluters should pay. Market regulators set a cap on how much carbon dioxide companies can emit. They then allocate a certain number of permits – normally one per tonne of carbon dioxide emitted – to companies participating in the scheme.

Companies that need to emit more than the allowances they hold can buy them from companies that make the effort to reduce their emissions – setting a carbon price. Regulators gradually tighten the cap over time, reducing overall emissions.

At least, that’s the theory. Since the recession hit, many carbon markets – most prominently the EU ETS – have suffered from an oversupply of permits and low carbon prices. That means companies don’t need to make as much effort to reduce emissions.

Perhaps wary of repeating other markets’ mistakes, China is taking a cautious approach to carbon trading.

Pilots

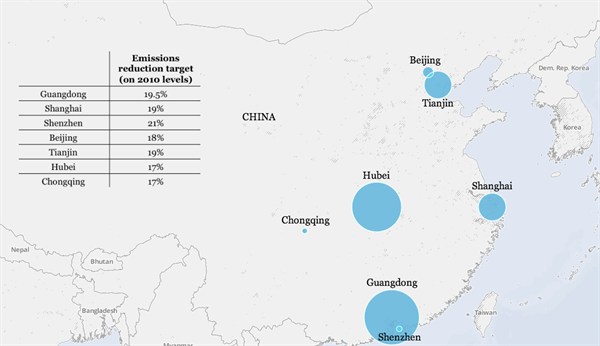

In 2011, China’s government announced plans for seven experimental markets: four in the cities of Beijing, Tianjin, Shanghai and Shenzhen and the three in the Chongqing, Guangdong, and Hubei provinces. All of the schemes are now up and running and together cover just over a billion tonnes of carbon dioxide.

Map created using CartoDB. For an interactive version of this map, click here. The size of the bubble represents the amount of emissions covered by each scheme.

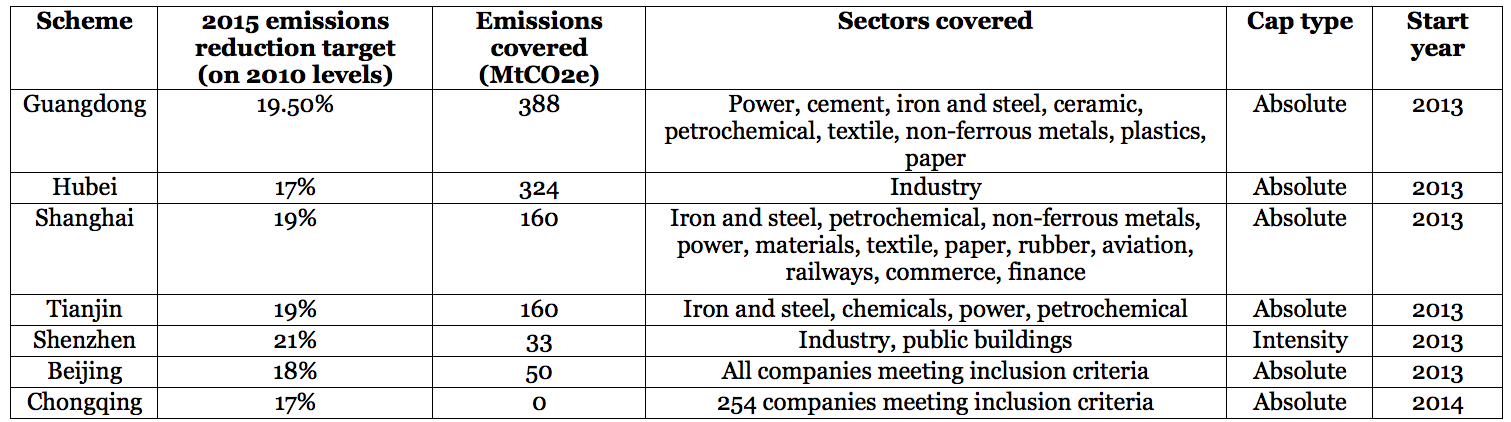

Each market was established with slightly different characteristics.

Six schemes require companies to reduce emissions by a set amount, known as an absolute cap. In contrast, the Shenzhen scheme aims to improve companies’ carbon intensity – their emissions per unit of economic activity.

While an absolute cap guarantees emissions will be reduced, overall emissions can still rise under an intensity target – even if companies become less carbon intensive.

The schemes also cover different sectors: from the power, cement, metals, and textiles sectors in Guangdong, to the heat sector and public buildings (amongst others) in Tianjin.

Likewise, the schemes have different criteria for which companies need to participate. Some schemes force companies that emit more than a specified amount of carbon dioxide each year to take part. Others base participation on how much energy a company or building consumes.

This table summarises the key differences:

Teething problems

All the markets are experiencing teething problems. For starters, China’s political culture and recent history means many participants have little experience of this sort of trading. As a consequence, things have been slow to get going.

There have been numerous reports of exchanges handling only a few trades a day with many firms struggling to understand how to trade, the Economist Intelligence Unit reports.

There are also problems with transparency. Some companies can’t provide robust records of their historical emissions, making it hard for regulators to know what level to set a cap at. Likewise, regulators don’t have the tools to verify the companies estimates when they are provided, potentially leading to fraud.

One year on

The seven pilot schemes are all feeling the effects of these problems, to a greater or lesser extent.

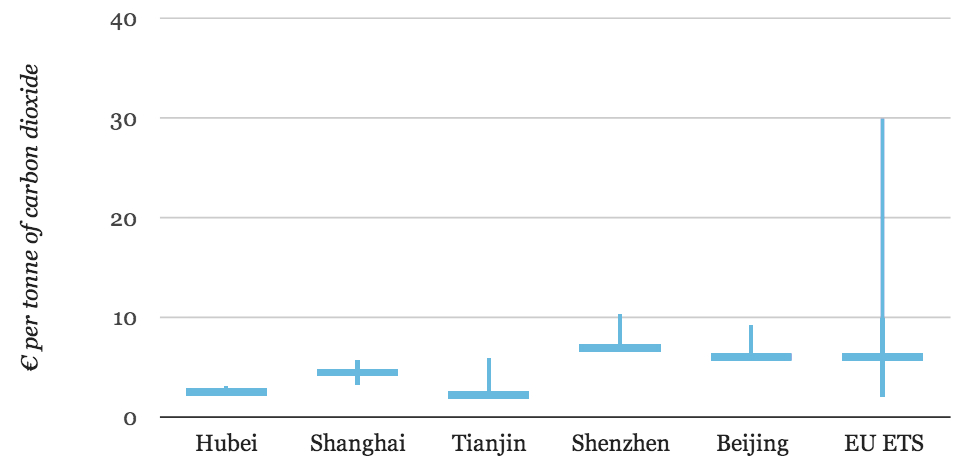

Carbon prices vary widely between the schemes. The chart below shows the highest, lowest, and current carbon prices of each of the schemes and the EU ETS.

Data from China Carbon, graph by Carbon Brief. Vertical bars show the range, horizontal bars show approximate current prices as of publication. Data for Guangdong and Chongqing was not available.

Prices reached a peak of Â¥86 (about â?¬10) per tonne in Shenzhen in March, and a low of Â¥17 (about â?¬2) in Tianjin in July. The EU’s carbon price is currently about â?¬6, having fluctuated between about â?¬2 and â?¬7 over the past year.

The enthusiasm of participants also varies. In its first year, companies traded the equivalent of 1,608,000 tonnes of carbon dioxide in Hubei’s scheme, according to the World Bank’s annual review of carbon markets. But Beijing’s scheme saw the equivalent of just 96,000 tonnes traded.

Shenzhen’s market is leading the way in terms of reforms. Last week, it announced that it would allow foreign investors to trade on the market. Trades can also now be completed in foreign currencies, which regulators hope will encourage participation. It remains China’s smallest market, however.

But Shenzhen’s progress isn’t being emulated everywhere. Guangdong added 8 million permits to its already oversupplied scheme after companies threatened to refuse to participate in the second phase. Beijing’s carbon price is doing better, but the scheme is hamstrung by the city’s lack of industry, limiting its potential to reduce emissions.

Future prospects

Despite such issues, the government has announced plans to launch a national market in 2016. But the details remain unclear.

A new “best practice” market could be established, taking the most effective bits from across the pilot schemes. Alternatively, the pilot markets could be linked with a new overarching national framework to smooth out the current differences.

Once the scheme is fully operational, it could dwarf the EU ETS in terms of the emissions it includes. But given the problems the pilot schemes are experiencing, that could still be some way off.

At least in the short-term, a carbon market is likely to remain an experiment rather than the backbone of China’s climate change response. But with China emitting more than twice as much carbon dioxide as the whole of the EU each year, its decision to explore carbon trading could prove to be significant.