Analysis: China’s Covid stimulus plans for fossil fuels three times larger than low-carbon

Guest authors

09.23.20Guest authors

23.09.2020 | 4:45pmChina’s main energy-consuming and producing provinces are directing the equivalent of hundreds of billions of dollars into fossil fuel projects, analysis of spending plans reveals.

If the investments go ahead, they would exceed spending plans for low-carbon energy threefold.

The findings are from our new analysis of the “major project lists” for eight Chinese provinces, which account for half the country’s CO2 emissions. The lists reveal the priorities of provincial authorities looking to recover from Covid-19 and prepare for the 14th “five-year plan”, due early next year.

Our analysis of the lists has identified 4,348 projects, with a combined reported price tag of RMB19.9tn ($2.95tn). Some RMB6,200bn ($920bn) is earmarked for investment in energy or transport, of which fossil fuel projects and railways each account for around a third, or RMB2,100bn of the total.

In contrast, relatively little of the energy or transport spending plans are directed towards low-carbon sources, with RMB340bln for renewables ($49bn, 5.6%), RMB120bn for nuclear ($18bn, 2.0%) and RMB80bn ($11bn, 1.3%) for electric vehicles, batteries and energy storage.

Our findings suggest China is focusing its post-Covid recovery on high-carbon energy and infrastructure, as it did after the 2008-9 global financial crisis. But a repeat of its emissions surge in 2010 is unlikely, because the current scale of its Covid stimulus is far smaller than in 2008-9.

Nevertheless, continued spending on fossil fuel infrastructure is poorly aligned with the country’s pledge to strive to peak CO2 emissions as soon as possible. It also poses questions for the surprise pledge, made this week by president Xi Jinping, to achieve “carbon neutrality” before 2060.

Investment plans

Every year, each Chinese provincial government compiles a list of “key projects”. Inclusion on the list opens the doors for developers to obtain permits and project financing, by conveying a government-supported status.

Appearing on the list is no guarantee that the project will go ahead, but the lists do reveal the priorities of decision makers at provincial level governments and state-owned enterprises.

We analysed the project lists of the eight largest Chinese provinces in terms of energy production and consumption, namely Guangdong, Hebei, Henan, Inner Mongolia, Jiangsu, Shaanxii, Shandong and ShanXi.

Chinese provinces. Graphic by Carbon Brief. Source: Esri. The designations employed and the presentation of the material on this map do not imply the expression of any opinion whatsoever on the part of Carbon Brief concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries.

These provinces are home to a third of China’s population and produce 50% of the country’s CO2, 43% of GDP and 37% of investment in fixed assets. They also played a significant role in the 2008 stimulus, delivering 40% of the year-on-year increase in capital spending.

Within these provinces, we identified a total of 4,348 projects that would cost a reported RMB19.9tn ($2.95tn). Some two-thirds of this investment is directed towards sectors that are not directly linked to energy, including everything from ICT infrastructure and manufacturing to other non-energy intensive manufacturing, tourism, health care, education, culture and sports.

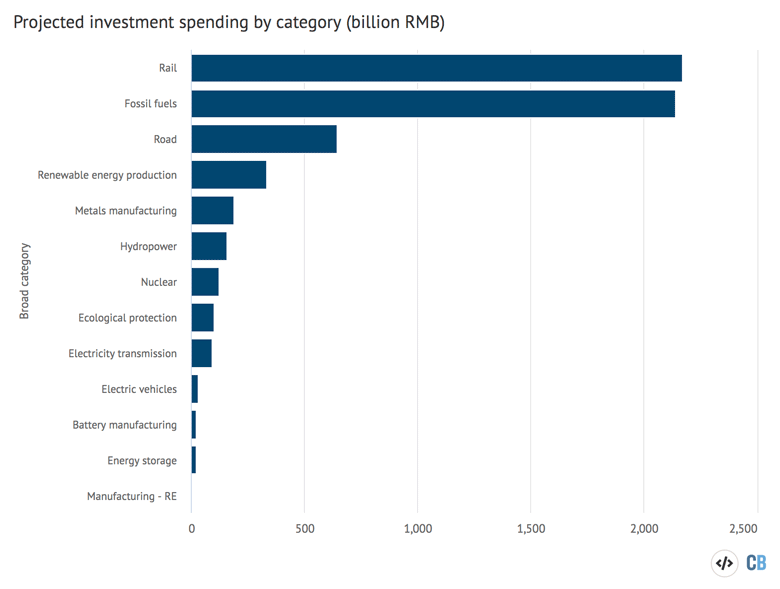

The remaining third – a potential investment of RMB6,200bn ($910bn) – is earmarked for energy and transport investment and is broken down in the chart below. This shows that rail and fossil fuel investments account for the majority of the planned spending, with far smaller shares allocated to low-carbon energy and electric vehicles.

Fossil fuel spending plans on the “major project lists” of eight Chinese provinces, broken down by type, billion RMB. Source: CREA analysis of public project lists and news reports. Chart by Carbon Brief using Highcharts.

Spending plans directed towards rail investment is the single-largest category in our analysis, at 36% of energy-related spending, with similar levels going towards fossil fuel-related projects – some 35% of the total. Road building is the third-largest category, at just over 10% of the total.

Looking at all planned low-carbon energy investments combined, another 10% of the total is directed towards renewables, nuclear and hydro. This is outweighed by the value of listed fossil fuel projects, by more than three to one.

In combination, just 13% of the spending plans could be categorised as broadly low-carbon, including renewables, nuclear, hydro, electricity networks, electric vehicles and batteries.

Investment targeted towards the energy-intensive metals industry is also of a similar magnitude to levels directed at renewable energy.

Key provinces

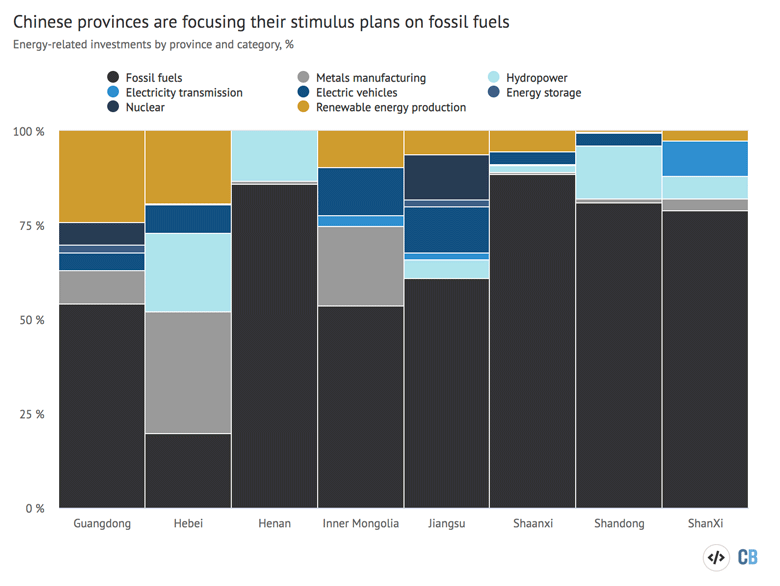

The eight provinces chosen for our analysis are the country’s most important in terms of energy use and production. Looking at their energy-related spending plans alone, most of these provinces appear to be putting a particularly heavy emphasis on fossil fuels.

Only two of the eight provinces – Guangdong and Hebei – are directing more capital spending at low-carbon energy projects than fossil-related schemes, as the chart below shows.

Energy-related spending plans in eight key Chinese provinces, by category, %. Source: CREA analysis of public project lists and news reports. Chart by Carbon Brief using Highcharts.

While Hebei’s “major projects” list includes significant plans for renewables and hydro, it is also heavy on projects boosting energy-intensive metals industry capacity. As such, high-carbon investments plans still account for the majority of Hebei’s total.

The mix of spending plans shows the priorities of these provinces as the 14th five-year plan is being finalised. These provinces are likely to favour the same sectors – and the same major projects – for inclusion into the five-year plan, to enable further expansion or financing.

Fossil fuel imports

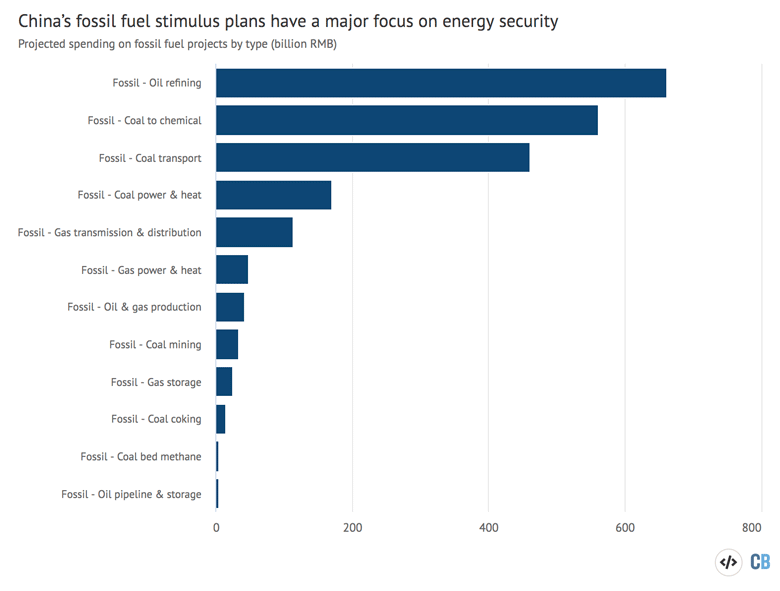

Within the broad category of fossil fuels, the major theme that emerges from our data is self-sufficiency and import substitution. The three largest types of fossil fuel investment, shown in the chart below, are all related to this goal.

More oil refining capacity would allow China to import cheaper crude oil, in place of expensive refined products. Some imported oil could be substituted with domestic coal feedstocks via “coal to chemicals” investments. And coal transport makes it easier for domestic producers in the inland provinces to compete against overseas miners, for deliveries to coastal consumers.

Fossil fuel spending plans on the “major project lists” of eight Chinese provinces, broken down by type, billion RMB. Source: CREA analysis of public project lists and news reports. Chart by Carbon Brief using Highcharts.

These types of investment are buoyed by two central policies: chairman Xi’s recent emphasis on “dual circulation” and premier Li’s earlier focus on energy security, both of which stress relying on domestic supply and import substitution.

These policies could be proving a major boost for domestic coal-to-chemicals production as well as oil and gas production. There is a long list of coal-to-chemicals schemes on province project lists, indicating that the industry is hoping for revived ambition after previous false starts.

Coal-to-chemicals

With 35 projects and targeted investment of RMB600bn ($90bn), coal-to-chemicals stands out as a favourite of the Chinese provincial governments whose investment plans we mapped.

These extremely large investment plans are particularly noteworthy given that the sector remains quite novel, with relatively few projects already operating on the ground.

Coal-to-chemicals means production of petrochemical products out of coal – everything from synthetic liquid and gaseous fuels to plastics and fertilisers – rather than from hydrocarbons.

This route is even more carbon-intensive than conventional petrochemical industry, meaning that it would not only lock in fossil fuel infrastructure with a long expected operating life, but would also increase the emissions intensity of fossil fuel consumption.

The vision of building a large petrochemical industry on domestic coal resources has a long history and has faced political ups and downs. It featured strongly in the 12th five-year plan (2011-15), but only a fraction of the projects were built due to economic, technical and environmental obstacles.

Oil refineries

Another large category of investment plans emerging from our data is oil refining, where seven large projects are targeted. This would represent an investment of RMB420bn ($70bn) and would create capacity for more than 80m tonnes of refined oil products per year, able to increase the amount processed in 2019 by some 14%.

China is already the second-largest oil refiner in the world, after the US. Like coal and steel, China’s oil refining industry also faces overcapacity, particularly for low-end products, such as petrol and diesel, whereas the country still imports most high-end petrochemical products.

The current five-year plan for the petrochemical industry set out to establish seven very large scale petrochemical industry bases located in Shandong, Hebei, Jiangsu, Shanghai, Zhejiang, Guangdong and Fujian, with major petrochemicals investments related to these plans showing up in our data in Shandong, Hebei, Jiangsu and Guangdong.

Investment in refining is motivated by national security and also aims to transform the country from a net importer to exporter of refined oil products.

Electricity generation

As explained above, the large majority of planned investments in fossil fuels is aimed at reducing reliance on oil imports. This means it is largely outside the power sector.

The energy security drive is also unlikely to endanger renewable energy development. To the contrary, given China’s position as the largest producer of renewable energy equipment in the world, fully domestic supply chains and cost competitiveness.

China’s investment in renewable energy appears to be building up after a stumble in 2019. Last year, it launched some 21GW of “subsidy-free” wind and solar projects, where prices are pegged to regional benchmarks for coal. This year, China has announced another 44GW of such projects, with investments set to total around RMB270bn ($40bn).

The fact that renewables are being deployed at scale, at cost parity with coal, shows that the economic scales have tipped. Despite this, our analysis shows provincial planners continue to direct investment towards coal power, with the number of projects accelerating steeply this year.

An earlier mapping by Greenpeace found that Chinese province investment plans for 2020 contained a total of 48 gigawatts (GW) of coal-fired power projects. This can be compared to the 32 projects, with a total capacity of 32GW, in the eight provinces we analysed.

Still, these coal-power projects would involve investments of some RMB170bn, less than half the total earmarked for spending on renewable energy, nuclear and hydropower.

‘New’ infrastructure

The current emphasis in China on “new infrastructure”, such as 5G, “internet of things”, industrial internet, cloud computing, blockchain, data centers, smart computing centres and smart transportation, is not evident in the spending priorities we identified.

There is a large number of such projects – particularly manufacturing of electric vehicles, batteries and charging stations, smart grids and so on – but their average cost is so small that they are dwarfed by the spending plans for a few oil refineries alone.

There is also little sign of economic diversification in the investment plans. Provinces with a heavy dependence on fossil fuels appear keen to continue to deepen their dependence, while Hebei, with the country’s largest iron and steel industry, leads in investment into metals manufacturing.

One aspect of the spending plans that could be characterised as green or low-carbon is the large investment directed towards railways, outweighing road schemes by three to one.

China’s world-leading high-speed rail network has been successful in decarbonising domestic travel. But further expansion entails links with less and less traffic, where the emissions from building the new rail lines and running low-occupancy trains could overwhelm avoided emissions from air and road travel.

High-carbon recovery?

China’s recovery from the global financial crisis in 2007-09 took the form of an unprecedented boom in heavy industry and construction, leading to the largest three-year increase in CO2 emissions for any country, in all of history.

As Chinese decision-makers look to stimulate the economy and engineer a recovery after the Covid-19 lockdowns, the key question for global emissions is whether this pattern will repeat.

So far, the recovery is again largely being driven by public investments – with private investment and consumption in the doldrums – leading many analysts to speak of a “two-speed” recovery.

The energy sector is playing a central role, as one of the few sectors where investment spending has seen double digit growth, even as overall spending in January-August was down marginally compared with levels in 2019.

This massive injection of public spending could be a major opportunity to accelerate the low-carbon transition. However, at the highest political level there has not been systematic emphasis on green or low-carbon infrastructure. Our analysis confirms that, as a result, the opportunity to build China’s recovery around low-carbon is not being taken.

Yet the current stimulus does not look like a repeat of 2008, if only because of its scale. In relation to GDP, it has been much more measured than it was 10 years ago, when investment spending grew 30% in one year. Now, total investment has barely increased year-on-year.

All the institutional and systemic factors that make China’s stimulus fossil-heavy remain.

The 2060 carbon neutrality target, and earlier CO2 emissions peak target – announced by president Xi this week – could spell a rearrangement of spending priorities.

Speaking to the UN General Assembly on Wednesday, Xi said that China would aim to peak CO2 emissions before 2030 and achieve carbon neutrality before 2060. He also pledged to “scale up” China’s 2030 climate pledge under the Paris Agreement.

Oil refinery and railway marshalling yard, China. Credit: Zoonar GmbH / Alamy Stock Photo.

The brief announcement leaves plenty of space for different readings, the least ambitious being that there is still another decade of time to build more fossil fuel infrastructure and increase emissions. A more progressive interpretation would see China slowing down its emissions growth immediately and getting into a clear decline before 2030.

A key indicator of what the announcement means in the near term will be the fate of the planned investments in high-carbon infrastructure, which we identified in our analysis.

As it stands, hundreds of billions are being directed towards coal power plants, coal-to-chemical plants, oil refineries and other high-carbon capacity, with an expected lifetime that would extend well beyond mid-century.

Methodology

We sourced the “major project lists” of eight provinces, where publicly available from provincial Development and Reform Council websites, and complemented this information with news reports on investment plans.

Of the 4,348 projects we identified, 72% included estimated costs if the projects were to go ahead. We estimated the costs of remaining projects by taking the average cost of other schemes in the same category.

For most schemes, the project lists only include a name, so we sought further information online. Projects were categorised where explicit reference was made to the purpose, for example coal transport or renewable energy equipment.

Many other transport infrastructure investments are likely to be related to coal or other energy sources, but carrying out such a categorisation was not feasible.

Many manufacturing and energy projects use labels such as “new materials”, “new energy” or “new energy vehicles”. Where possible, we tried to evaluate the basis for such labels. For example, our “electric vehicles” category only includes manufacturing facilities dedicated to making EVs or EV components, not components with a broad array of applications that includes electric vehicles.

-

Analysis: China’s Covid stimulus plans for fossil fuels three times larger than low-carbon

-

Analysis: Fossil fuels dominate China’s post-Covid stimulus plans for energy