CCC: UK must cut emissions ‘78% by 2035’ to be on course for net-zero goal

Multiple Authors

12.09.20Multiple Authors

09.12.2020 | 12:01amThe UK needs to cut its emissions by 78% below 1990 levels over the next 15 years, according to the latest advice from the Climate Change Committee (CCC).

For the first time, the government’s climate advisers have proposed a legally binding “carbon budget” that is in line with the national target of “net-zero” emissions by 2050, which was first set last year.

More specifically, the CCC has now set a target for the five-year period 2033-37, which is known as the “sixth carbon budget”.

The report’s scope represents the degree to which the UK’s ambition to tackle climate change has scaled up recently. Just 18 months ago, when the national target was still set at an 80% reduction, the same level of emissions cuts were expected to take twice as long.

It comes as the UK – which will host the COP26 UN climate talks next year – aims to establish itself as an international climate leader, following an ambitious new “68% by 2030” commitment under the Paris Agreement and prime minister Boris Johnson’s new “10-point plan” for achieving net-zero.

However, with the country set to miss its upcoming fourth and fifth carbon budgets, the government’s own figures show current plans still fall “a long way short” of what is required, the CCC says.

Here, Carbon Brief draws out the key points from the CCC’s new guidance – made up of nearly 1,000 pages across three reports – which covers the sixth carbon budget advice and, more widely, the net-zero pathway it has mapped out for achieving a fully decarbonised economy by 2050.

Update 20/04/2021: UK media reported that the government intended to announce a new emissions target in line with the CCC’s sixth carbon budget advice ahead of a major climate summit led by US president Joe Biden. According to the Financial Times, “emissions from international aviation and shipping are likely to be included in the new UK target”.

Both the new target and the inclusion of international aviation and shipping in the budget were subsequently confirmed by the government later that day.

- What is the ‘sixth carbon budget’?

- What are the issues with existing budgets and ‘hot air’?

- What is the CCC’s new pathway to net-zero by 2050?

- How much will the sixth carbon budget and net-zero goal ‘cost’?

- Road transport and rail

- Buildings

- Manufacturing and construction

- Electricity generation

- Fuel supply

- Agriculture and land use, land-use change and forestry

- Aviation and shipping

- Waste

- F-gases

- Greenhouse gas removals

What is the ‘sixth carbon budget’?

The Climate Change Act, originally established in 2008, requires the UK government to set carbon budgets to act as “stepping stones” towards the 2050 emissions target.

These budgets are caps on the amount of greenhouse gases that can be emitted in the UK across a five-year period. So far, five carbon budgets have been put into law.

In the new report, the committee recommends that the sixth carbon budget, which will run from 2033 to 2037, should be set at 965m tonnes of CO2 equivalent (MtCO2e), equating to, on average, 193MtCO2e annually. In 2019, annual emissions stood at 522MtCO2e.

As the first carbon budget advice to emerge since the UK set a net-zero goal last year, it marks a critical point for the country’s trajectory towards addressing climate change.

Lord Deben, who chairs the CCC, has described it as “the most comprehensive advice we have ever produced”, while CCC chief executive Chris Stark told a press conference the legally binding goal is “the really important target that will shape UK emissions over the next 30 years”.

It comes only days after the government announced a new “nationally determined contribution” (NDC) for 2030 – its pledge for achieving the goals of the Paris Agreement, following advice from the CCC.

The NDC aims for an “at least 68%” reduction in emissions by the end of the decade, compared to the roughly 57% reduction currently set out in the fifth carbon budget over the same period.

This morning we have published our letter to @beisgovuk on the UK’s 2030 NDC.https://t.co/TpyUXvuiZm

— Chris Stark (@ChiefExecCCC) December 3, 2020

The UK should commit to reduce emissions by at least 68% from 1990 to 2030 – and make clear commitments on international aviation and shipping, climate finance and adaptation.

The committee is clear that its guidance, both on the new domestic climate budget and the international NDC, is informed by the same net-zero analysis. It describes its advice as “fair” and “compatible with global efforts to limit warming to 1.5C”.

Achieving the sixth carbon budget will be a significant undertaking, requiring “almost all new purchases and investments are zero-carbon by around 2030”, widespread behaviour changes and rapid deployment of emissions removal technologies, the CCC says.

According to the CCC, the 2030s will need to be a period of particularly dramatic drops in emissions as high-carbon technologies, such as petrol and diesel cars, are phased out. The report recommends a completely decarbonised power system by 2035 and an end to gas boiler sales by 2033.

Taking its lead from the UK’s recent climate assembly, which saw citizens offer their views on achieving net-zero emissions, the committee has tried to ensure societal fairness and prioritise “reductions where known solutions exist”.

Crucially, unlike previous budgets, the CCC says this one should incorporate the UK’s share of international aviation and shipping emissions.

Until now, carbon budgets have not included emissions from these high-polluting sectors, but have allowed “headroom” for them by setting lower targets for other sectors.

Nevertheless, the ability of the government to include emissions from planes and ships in carbon budgets, if it chooses to, has always been enshrined in the Climate Change Act.

In its new advice, the CCC states that the existing approach is unsustainable, highlighting the need to apply pressure to these industries, as well as their non-CO2 environmental impacts which are not covered by carbon budgets.

UN convention means the NDC does not include these emissions. However, the CCC says the UK must make “clear commitments” in its NDC to act on them regardless.

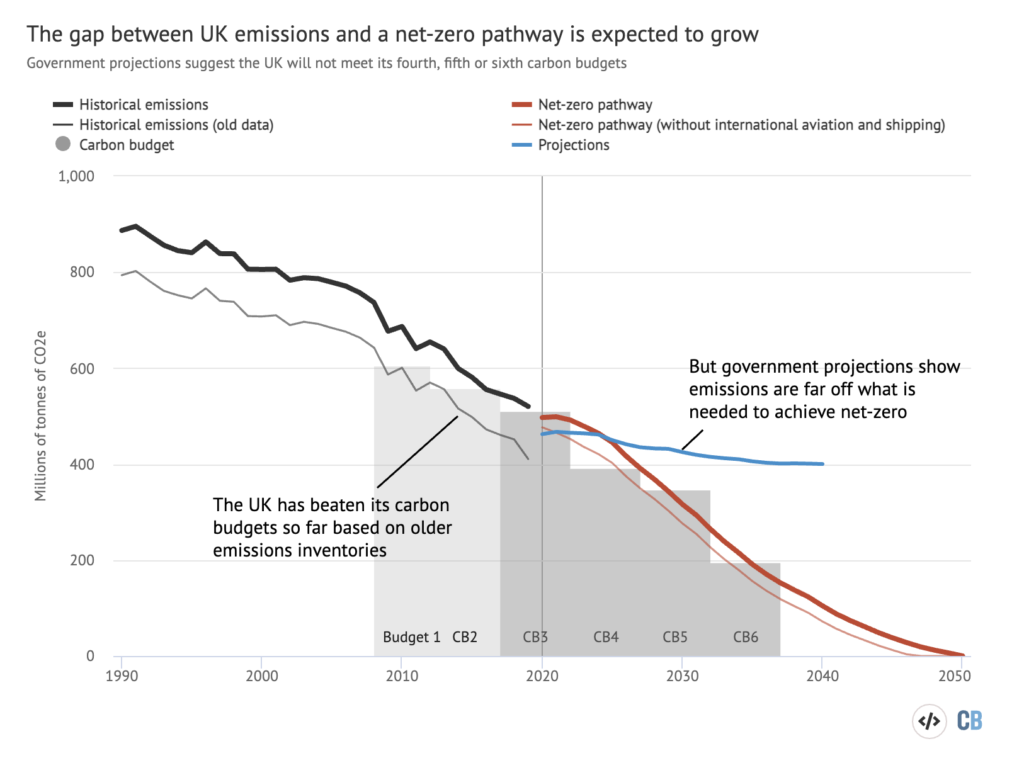

Despite talk of ambitious future commitments, the CCC itself notes that while the UK will likely meet its third carbon budget, which ends in 2022, it is “off track” for the next two.

The chart below shows the new sixth carbon budget and the UK’s progress on its existing carbon budgets. As indicated by the blue line, current government projections show the nation is not on track to achieve its fourth or fifth carbon budgets and is far from the net-zero trajectory set by the CCC.

The “policy gap” between the UK’s current trajectory and where it needs to be to arrive at net-zero has not gone unnoticed.

There’s been a growing “policy gap” between where UK is heading vs where it needs to be on climate

— Simon Evans is on paternity leave (@DrSimEvans) November 17, 2020

Basically cos UK hasn’t had a credible attempt at a plan for years

In latest govt projections, the gap grew again & was larger than ever…https://t.co/vMyxqsmuJv

3/ pic.twitter.com/RpcdD7ufto

A recent analysis of Boris Johnson’s 10-point plan by the consultancy Cambridge Econometrics, which also contributed cost analysis to the CCC guidance, found that it “does not align” with the longer term strategy.

Similarly, in its advice the CCC notes that while the 10-point plan included “a number of welcome measures…gaps remain”.

A progress report published by the committee in June documenting the government’s progress towards its climate targets stated that just two of 31 key policy milestones had been met over the past year.

The Climate Change Act requires the government by law to develop policies and proposals that “enable” its carbon budgets to be met and the CCC is meant to advise on this.

The committee highlights a number of policies in the works, including the long-awaited energy white paper, the building and heat strategy and a hydrogen strategy. It calls on the government to bring these policies forward “as soon as possible”.

“We have begun to see the consultations, policies and strategies that show that the government is taking the net-zero policy challenge seriously,” the report states.

Later sections of this article examine the sectoral recommendations made by the CCC in order to set a course for net-zero and achieve the sixth carbon budget.

The CCC’s report includes specific advice for Scotland, Wales and Northern Ireland, which together cover a fifth of UK emissions. It notes that nearly 60% of all the required abatement in these nations is in sectors where key powers are partially or mostly devolved.

Following this advice, the government is required to legislate the carbon budget by the end of June 2021.

In a year that will see the UK take up the presidency of both the COP26 climate summit and the G7, the CCC emphasises the importance of a strong new carbon budget to demonstrate leadership.

“Our influence in the wider world rests ultimately on strong domestic ambition,” the report states.

What are the issues with existing budgets and ‘hot air’?

A combination of factors including Brexit, changes to the way greenhouse gas emissions are assessed and the inclusion of international aviation and shipping have added complications to the way the UK’s carbon budgets are calculated and accounted for.

These issues are important because they will define whether or not the budgets are met, as well as whether they are applying meaningful pressure to cut emissions for years to come.

Previous carbon budgets have been set on the basis that the UK is a member of the EU and participates in the EU emissions trading system (ETS).

Instead of the country’s actual emissions, the budgets have been based on the UK’s “net carbon account”. This is the sum of all the emissions allowances the country receives from the ETS for sectors such as power, heavy industry and domestic aviation, plus emissions not covered by the trading scheme.

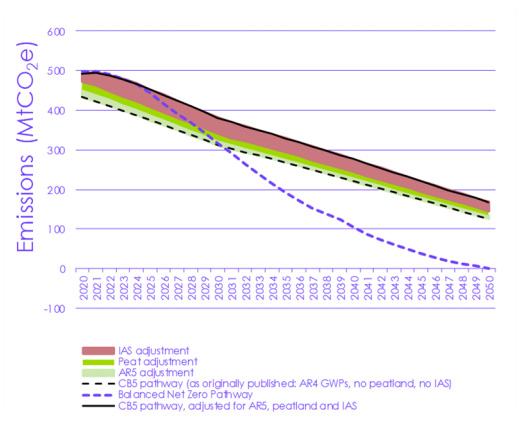

As a result of this accounting quirk and the fact the ETS allowances are fixed independently of real-world emissions, the UK’s net carbon account is significantly higher than the emissions actually produced in the country. (The difference can be seen in this chart.)

Leaving the EU and the ETS means the net carbon account would no longer make sense. As a result, the new advice recommends the sixth budget is set on the basis of actual emissions.

Dr Stephen Smith at the University of Oxford, who previously led both the government and the CCC’s climate science teams, tells Carbon Brief that he would also expect existing carbon budgets to be “modified accordingly” if the UK is outside the ETS.

In a letter on the implications of Brexit written in 2016, the CCC wrote that accounting of carbon budgets would indeed need to change if the UK left the ETS and such action would likely “require an adjustment to the budget”.

It currently remains unclear what interaction, if any, the UK will have with the ETS in the future. However, the CCC does not recommend modifying any existing budgets in its report.

Mike Thompson, director of analysis at the CCC, tells Carbon Brief that even if there is a new trading scheme linked to the EU, a new cap would simply be set in line with actual emissions:

“We can stop worrying about the net carbon account in the future. Everything we are proposing is about actual emissions.”

The new CCC report states that the “net” approach was “confusing and did not drive action in all areas”.

Thompson notes that while actual emissions figures are currently lower than the net carbon account, more accounting changes mean they are due to increase to similar levels over the next few years.

Adjustments to the UK greenhouse gas inventory, which will more accurately account for emissions from peatland and the global warming potential of methane and other non-CO2 gases, are expected to be made by 2025. The impact of these adjustments can be seen in the green area of the chart below.

Another issue relating to the adjustment of existing budgets is that of net-zero alignment, seeing as the fourth and fifth carbon budgets were created before the current 2050 target was set.

Although the committee says that for the fifth budget (2028-2032) in particular emissions must fall faster than is currently required to remain on a net-zero trajectory, it also explicitly notes that it does not require the UK to set new budgets in line with net-zero.

According to the CCC, the level of the fourth carbon budget (2023-2027) is “broadly appropriate” for its net-zero trajectory if aviation and shipping are not included, as has always been planned.

As for the fifth carbon budget, Thompson tells Carbon Brief that, in the CCC’s view, this is currently “too loose” and will require significant overachievement to stay on a net-zero pathway.

The CCC even calculates what a net-zero aligned fifth carbon budget would mean, changing it from 1,725MtCO2, excluding international aviation and shipping, to 1,585 MtCO2e including them.

However, rather than doing this, it says that the fourth and sixth carbon budgets being “in the right places” combined with the additional pressure of the UK’s new NDC for 2030 is enough to get the budget in between on track.

Thompson also says that, as with the sixth carbon budget, the government could bring international aviation and shipping into the scope of its fifth carbon budget.

“That’s a way of tightening the budget without going back and changing the actual legislated number,” he says. Thompson adds:

“There’s a very big programme of policy here that needs to be developed and, frankly, that’s what we want the government to be getting on with rather than messing around with carbon budgets which are already not far off the right place.”

Smith tells Carbon Brief there is a historical precedent to this approach, referring to previous plans to raise the ambition of the first three carbon budgets.

“Reopening climate legislation was seen as [opening] a can of worms…So it was seen as better to stick with those and then, when it came to legislating the fourth carbon budget, make that more ambitious.”

However, climate lawyer Jonathan Church is more sceptical. He tells Carbon Brief:

“It’s quite bold to just assume that the sixth carbon budget set in the right place can have sufficient traction now on what government needs to be doing, when experience suggests that having those budgets in place doesn’t necessarily mean you get the policies you need from government. That’s why we still have these policy gaps.”

A CCC-commissioned report released last year concluded that, even though the first and second carbon budgets were comfortably met, it was not due to sufficient policy interventions and was, in fact, largely the result of the global financial crisis a decade ago.

Church notes that without changes the UK will be in a situation where its less ambitious fifth carbon budget covering 2028 to 2032 will be governed by the nation’s legal system, which is “stronger” than the system governing its more ambitious 2030 NDC.

“That’s problematic,” he says. “it makes it far less likely we’ll ever get to our 2030 NDC if our legally binding target, our domestic target, isn’t even at that level.”

A final concern around budgets comes from the “hot air” that can be injected into them due to an allowance within the Climate Change Act to “carry forward” overachievements on carbon budgets to meet subsequent budgets.

Previously, the CCC has emphasised that these “flexibilities” are meant to be used sparingly, if at all.

Nevertheless, the government already stated last year an intention to use this mechanism to ensure changes in greenhouse gas inventories do not mean it misses future budgets.

Given the “extremely large outperformance” for the third carbon budget “for reasons other than policy” – namely Covid-19 and changes in the EU ETS system – the CCC’s new report says it is very important any “surplus” is not carried forward:

“Existing budgets are already on track or too loose for a path to net zero, so there could be no justification to carry forward outperformance of the third or subsequent carbon budgets.”

(The report also notes that performance against the new budget should not include the use of international carbon credits, of the kind set out in Article 6 of the Paris Agreement.)

Church tells Carbon Brief that there is a danger that the fourth and maybe the fifth budget could end up being met using hot air “without taking the kind of systemic action you need”.

This is “all very problematic when you get to the sixth carbon budget,” he says.

What is the CCC’s new pathway to net-zero by 2050?

As part of its net-zero advice, the CCC has published a methodology report detailing the analysis and evidence it has used to construct a set of pathways to net-zero, which form the basis of the report.

In its original net-zero guidance, the committee presented a single scenario dubbed “further ambition” which acted as a “proof of concept”, but which is, the new report says, “relatively conservative”.

While this provided a vision of what a “net-zero UK” would look like, Stark told journalists this week that in the CCC’s new guidance it wanted to present a detailed “route map” for how to get there.

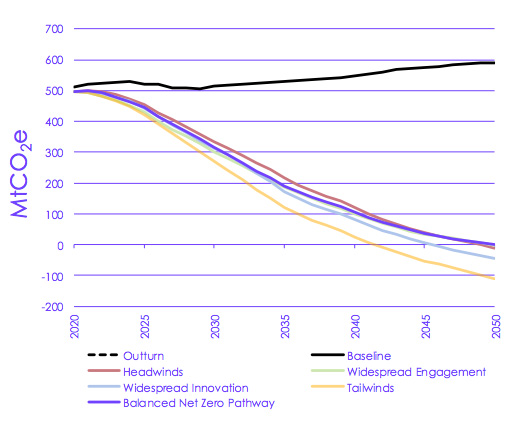

In total, the CCC modelled 70 scenarios and used different combinations of these to construct five core “exploratory” scenarios for reaching net-zero by 2050. These scenarios can be seen in the chart below.

Chief among these was the “balanced net-zero” (BNZ) pathway, which was informed by the other four. This is the pathway the CCC has used to advise on the sixth carbon budget, as well as the 2030 NDC target.

“It’s ambitious, it’s very challenging, it’s also, we think, entirely feasible and, crucially, I think very, very appealing,” Stark said in his introduction of the BNZ pathway.

The scenario requires emissions cuts of around 21MtCO2e from 2019 to 2035 – and then 13MtCO2e to 2050. Stark says this “front-loaded” path would go hand-in-hand with post-coronavirus economic recovery.

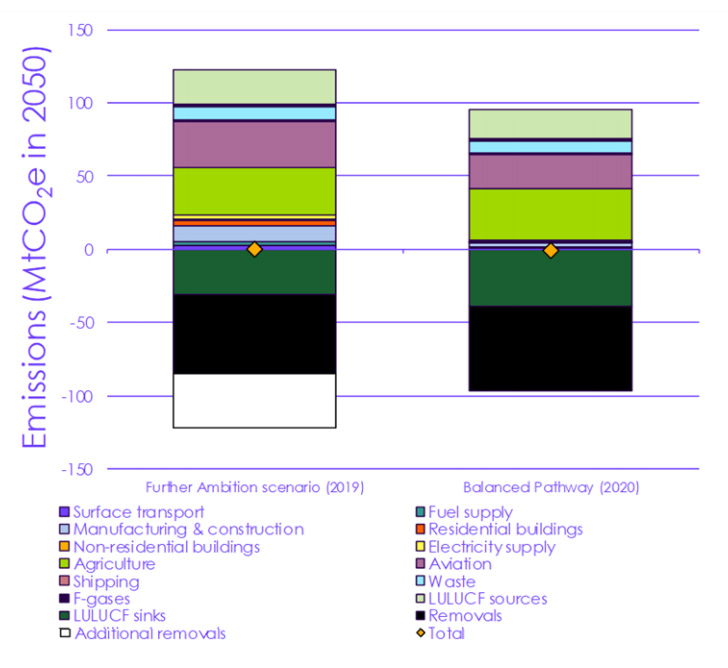

Key differences between this and the “further ambition” scenario include lower use of fossil fuels and less remaining emissions in hard-to-decarbonise sectors, such as aviation and heavy industry, due to more ambitious assumptions about the rollout of technology.

There is also less use of carbon capture and storage (CCS) in the BNZ pathway and more use of natural emissions removal methods, such as tree planting. This is consistent with feedback from the climate assembly and also lowers overall costs.

The chart below showing remaining emissions in 2050 indicates key differences between the two net-zero pathways. The BNZ pathway has fewer remaining emissions and, therefore, does not need to rely on potentially expensive additional removals.

Behavioural changes also play a bigger role in the BNZ scenario, including a 35% reduction in meat consumption by 2050 compared to 20% in the further ambition scenario.

Generally, the report highlights the increasingly important role of behavioural changes in getting to net-zero, noting that “to date, much of the success in reducing UK emissions has been invisible to the public”.

CCC analysis finds that 43% of emissions cuts on its main route to net-zero require a degree of consumer choices combined with low-carbon technologies, such as driving electric cars and installing heat pumps. An additional 16% is primarily societal or behavioural changes, such as avoiding planes or eating healthier diets.

The remaining core scenarios mapped out by the committee are: “headwinds”, which is similar to “further ambition” in terms of ambition; “widespread engagement”, which is characterised by higher levels of societal and behavioural changes; and “widespread innovation”, which involves greater success in cutting technology costs.

The final “tailwinds” scenario involves extensive behavioural change and innovation. In doing so, it diverges the most from the BNZ pathway, with emissions 36% lower over the course of the budget period.

In a further exploratory scenario, the CCC looked at whether it would be possible to achieve net-zero with virtually no CCS, meaning low-carbon hydrogen and gas-based power would be ruled out and only nature-based emissions removals could be used.

The committee found that, by following this path, it would be possible to achieve net-zero by 2050, but only in the most ambitious “tailwinds” scenario possible and with no room for underperformance from other sectors.

“Overall, this supports our message that CCS is essential to achieving net-zero, at lowest cost, in the UK,” the report concludes, emphasising the urgency of scaling up this technology.

How much will the sixth carbon budget and net-zero goal ‘cost’?

Estimating the “cost” of the net-zero goal has been a hot topic ever since the UK government made its commitment last year.

When the CCC offered its first net-zero advice in 2019 it estimated 1-2% of GDP would need to be invested to reach the net-zero target, prompting then-chancellor Philip Hammond to place a figure of “more than £1tn” on the target.

This unevidenced figure faced pushback from those who argued it did not account for the benefits of targeting net-zero. However, the CCC’s original net-zero report itself did not place a figure on these benefits.

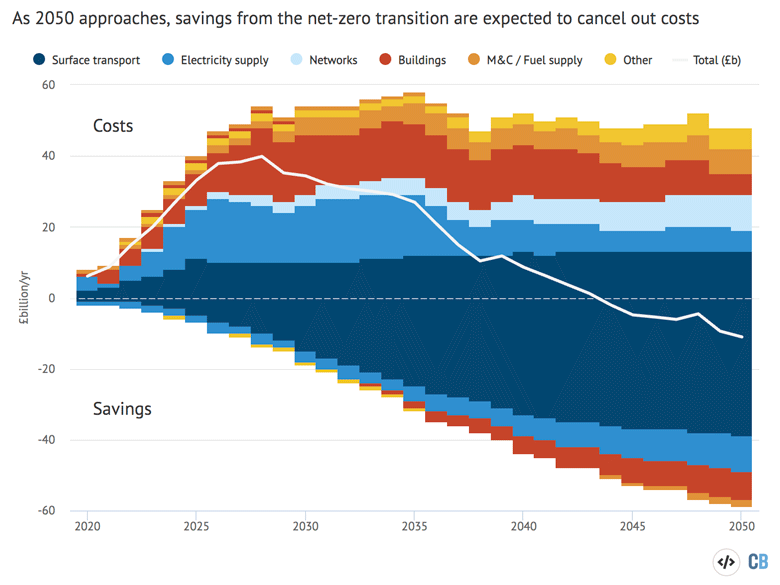

The sixth budget advice not only estimates lower costs overall, but it also looks at the longer-term impact on GDP of transitioning to a cleaner society. It concludes that it could see a GDP boost of around 2% within a decade.

The CCC’s analysis suggests that the yearly cost of achieving net-zero would be 0.6% of GDP by the early 2030s, before falling to around 0.5% by 2050.

This would involve increasing low-carbon investment from around £10bn in 2020 to around £50bn by 2030, “primarily” from private companies and individuals, the committee says. It notes that the total economy-wide investment in the UK last year was £390bn.

“This investment generates substantial fuel savings, as cleaner, more-efficient technologies replace their fossil-fuelled predecessors,” writes Lord Deben in his introduction to the report.

The chart below shows how, by 2050, the savings cancel out the investments entirely.

The CCC notes that costs, expressed as fractions of GDP, “will not necessarily reduce GDP by an equivalent amount, particularly given the spare capacity following the pandemic”. By its analysis, even when costs still outweigh savings in the 2030s, the UK’s GDP could actually increase as resources are redirected from fossil fuel imports to UK investment (see below).

Deben also notes that, while the costs are low, “that must not hide the need to distribute the costs and the benefits fairly”. While new low-carbon job opportunities will arise, “there will also be high-carbon sectors that shrink,” he adds.

Stark told journalists in a press conference that he was particularly “excited” to reveal the new numbers:

“It’s now clear that, at worst, we’ve got a very small cost overall, in order to unlock those very big benefits of tackling climate change.”

As for the reasons behind this change, Stark said this was, in part, because the initial net-zero assessment was deliberately conservative in its assumptions – for example, regarding the price of generating electricity.

With the price of offshore wind falling in the latest auction round by around a third compared to the previous one two years earlier, more optimistic scenarios are becoming available.

The report also details more opportunities for electrifying or using green hydrogen produced using renewable power in industry, which, in turn, can bring down prices. Stark added:

“One of the reasons for [the fall in cost] is that we’re not doing so much greenhouse gas removal, which tends to be one of the more expensive strategies, because we’ve found more ways to cut carbon in the first place.”

Costs are calculated compared to a hypothetical scenario in which there is no further climate action, but also, crucially, where the climate is not changing and there are no resulting costs from this.

While the report does mention other co-benefits – for example, to people’s health and the environment as a result of efforts such as more plant-based diets and mass tree planting – these are not factored into these costs.

As a result, the CCC says it is likely to be “overstating” the costs, even though they are “very small”.

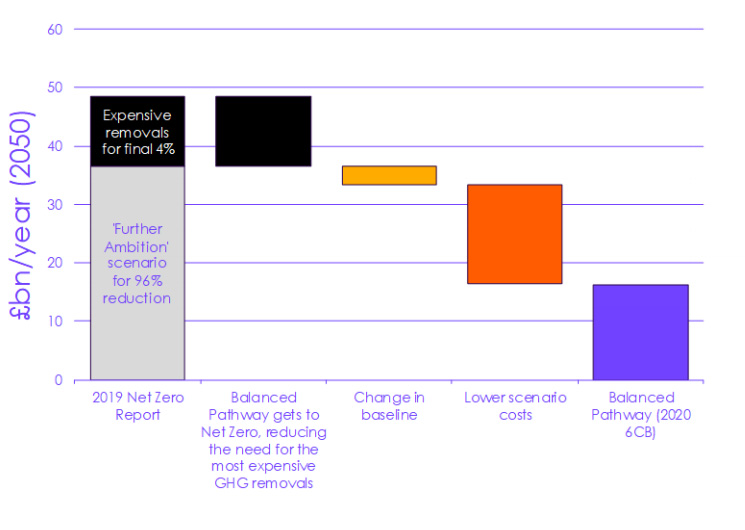

The chart below shows the reduction in costs estimated for the BNZ pathway compared to the “further ambition” scenario outlined by the CCC previously.

Besides generally lower costs for decarbonisation, a big portion comes from the previous assumption that the remaining 4% of emission, after everything else had been removed, would have to come from direct air carbon capture with CCS (DACCS), one of the most expensive emissions reduction options.

Another reason for the lower costs is the fact that the new scenario is compared to a world in which some climate action has already been taking place up to today. The previous baseline was a world in which climate action stopped in 2009, meaning less progress had already been made.

Phil Summerton, chief executive officer at economic modelling consultancy Cambridge Econometrics, which undertook analysis that fed into the new CCC guidance, tells Carbon Brief the framing of “cost” has not helped the messaging around net-zero:

“The problem is that the overall narrative has become cost rather than investment…It’s a natural thing to do because we are talking about making purchases.”

The CCC commissioned Cambridge Econometrics to use its macroeconometric E3ME model to demonstrate “the wider implications for the UK economy” of achieving the sixth carbon budget.

The result was an increase in GDP of around 2% by 2030 and 3% by 2050, with a boost to employment of around 1% over the next decade. The CCC’s report notes:

“The results show that despite there being an overall cost in bringing about the technologies to reduce carbon emissions, there is an increase in economic prosperity, in terms of an aggregate increase in GDP, jobs and real disposable incomes.”

The changes were largely the result of cutting oil and gas imports and, instead, spending that money on the UK economy, as well as falling electricity prices from switching to cheap renewables.

Finally, the CCC builds on its previous call for a “green recovery” from Covid-19. It notes that climate investments do not only support jobs at a time of high unemployment, they can also take advantage of current low interest rates.

Given the opportunity to invest and stimulate the UK’s struggling economy, the CCC says “it is more important than ever” to assess economic effects based on more than just simple costs.

Road transport and rail

Surface transport emits more greenhouse gases than any other sector in the UK. Policies to tackle these emissions are already in place – for example, in order to pave the way for electric vehicles (EVs), the sale of new petrol and diesel cars and vans will not be permitted after 2030.

However, the CCC’s report finds that “policies are off-track to contribute to the net-zero target and need strengthening”.

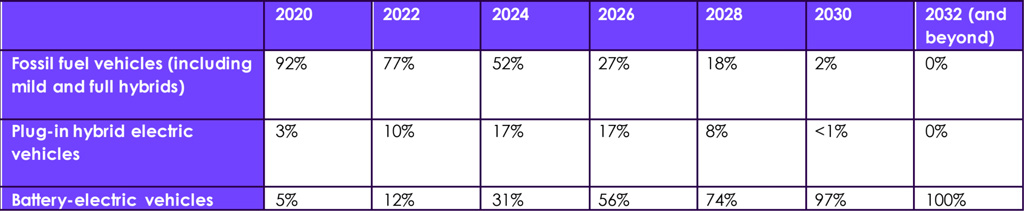

The report argues that a “zero-emission vehicle mandate” is needed, requiring car and van manufacturers to sell an increasing proportion of zero-emission vehicles, reaching 100% by 2030 and with only a small proportion of hybrids allowed until 2035.

Ambitious goals for diesel and petrol vehicles emissions are needed, as too is a “rigorous testing regime” more frequent than the five-year interval used in the EU, according to the report.

Many EVs currently cost thousands of pounds more than equivalent petrol or diesel vehicles, the report notes, and only 73,000 EVs were sold in 2019, compared with 2.2m petrol and diesel vehicles in the UK. This CCC highlights that “the supply of zero-emissions vehicles will need to scale up so that it doesn’t constrain demand”.

The government has committed £1.3bn towards charging infrastructure, with £500m in “Project Rapid” dedicated to charging on motorways and major roads. This is “around the right level of investment at present” according to the report, but investment is still needed throughout the 2020s and beyond.

The CCC identifies battery life as an important area of research and “welcomes” the government’s plans to develop gigafactories in the UK to scale up the production of batteries for EVs.

Furthermore, the report states that the government needs to extend its commitment to making 100% of its central car fleet zero-emissions by 2030 to include all government vehicles.

Despite comprising only 5% of UK road vehicles, heavy-goods vehicles (HGVs) produce 17% of greenhouse gas emissions from the surface transport sector. The report “welcomes” the government’s promise of £20m for zero-emission trials for HGVs in 2021 and says that trials should begin to collect data by 2023, with all vehicles fully operational by 2025.

However, according to the report, decarbonising the sector by 2050 requires the sale of new diesel HGVs to end by 2040. Furthermore, CO2 emission standards at least matching those of the EU are needed for HGVs, the CCC says, requiring a 15% reduction in carbon-intensity by 2025 and 30% by 2030.

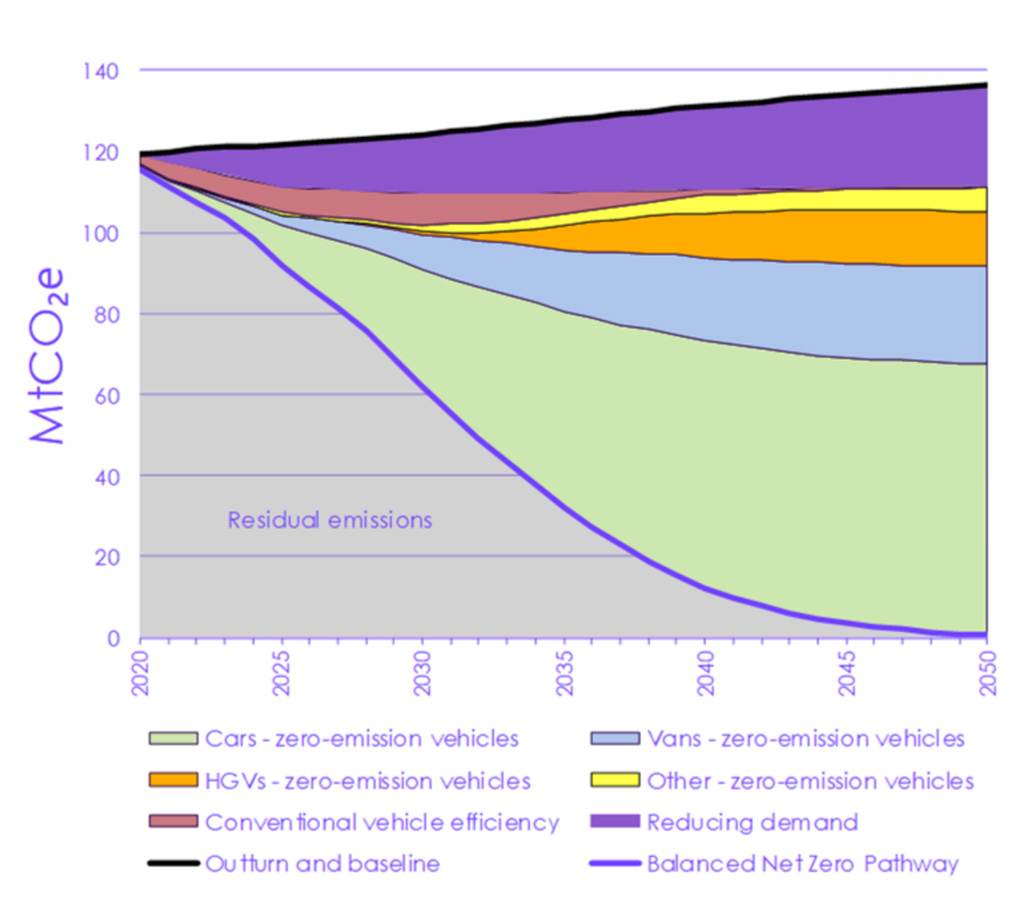

The figure below shows how the proportion of emissions from different types of vehicles would need to change in order to reach net-zero by 2050 under the BNZ pathway.

Finally, the report finds that the government must deliver on the target of removing all diesel trains by 2040 and improving local transport policies to encourage people to walk, cycle and take public transport.

Buildings

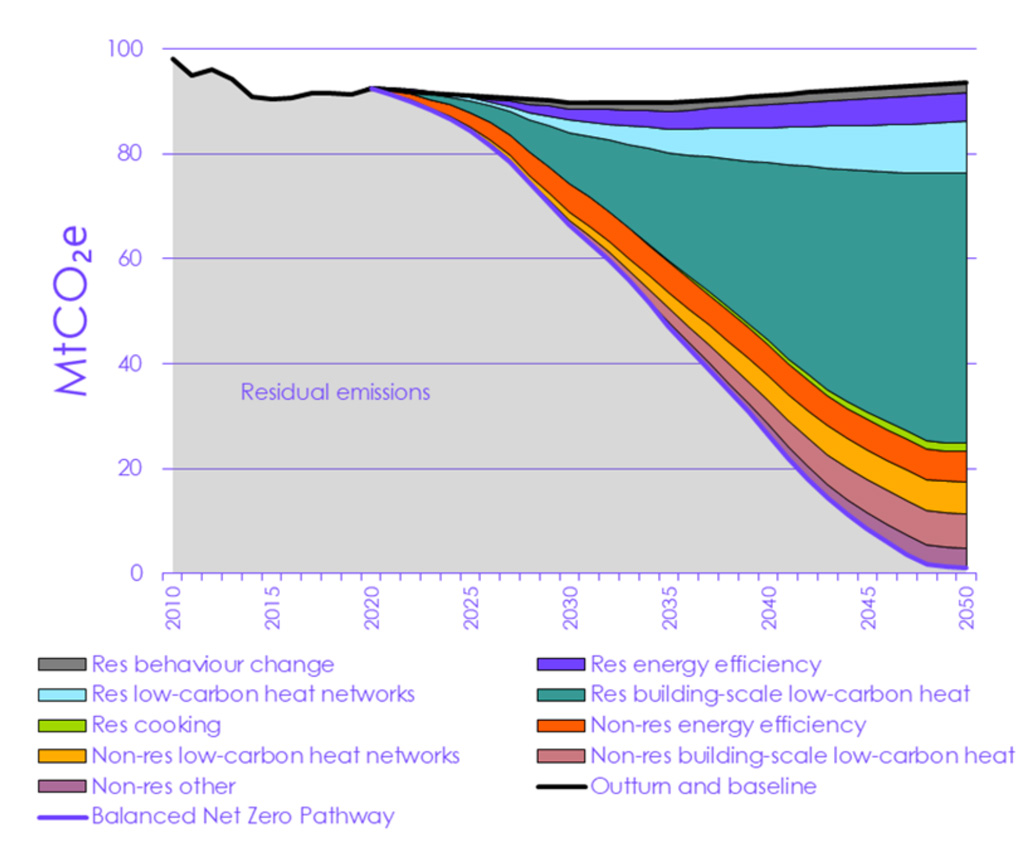

UK housing is diverse and relatively inefficient, the CCC says, so a range of approaches are needed to achieve net-zero emissions. Building emissions need to fall by roughly 50% of their 2019 levels by 2035 on their way to reaching net-zero in 2050 in order to align with the BNZ pathway, the report finds.

The chart below shows the BNZ pathway for the types of energy production in homes that will enable the UK to reach net-zero emissions by 2050.

This report states that a full conversion to hydrogen as a fossil-fuel alternative would be “unwieldy due to low system efficiency” and it recommends hydrogen hybrid heat pumps for use in homes. Hydrogen trials should start in 2023 and all boilers should be “hydrogen-ready” by 2025.

As the average lifetime of a boiler is around 15 years, the phase-out date for boilers is likely to be ahead of 2035. In the recent UK Citizens Assembly report, 86% of people supported a ban on new gas boilers between 2030-35, the CCC notes.

To align with the BNZ pathway, the report also states that all new buildings need to achieve net-zero emissions by 2025. To do this, the report recommends deploying 5.5m heat pumps in homes by 2030, 2.2m of which should be in new build homes.

This means deploying 1m heat pumps in homes per year by 2030 – a significant step compared to the 26,000 per year currently deployed. The government needs to invest more into scaling up markets and supply chains to cover the new installations so that they can service 1.8m homes and 50% of the non-residential heating market by 2033, the CCC says.

To meet the BNZ pathway, the report also states that by 2033:

- Natural gas should be phased out in any areas not designated for low-carbon district heat or hydrogen-conversion areas.

- The heat pump industry should scale up to manage over 1m installations a year in homes.

- Low-carbon heat supply chains should service up to 1.8m homes and 50% of the non-residential heating market.

Fossil fuels are currently responsible for 11% of energy consumption for heating and hot water. As such, the report states that electrification is “of primary strategic importance” in order to achieve net-zero emissions and that the government should publish a proposal on phasing out oil and coal by 2028.

Finally, there is “an urgent need to upskill our workforce”, the CCC warns, as there are significant skill deficits in areas such as repair and maintenance. Government intervention will be required to ensure that skills are developed on the scale needed and in adequate time, the report adds.

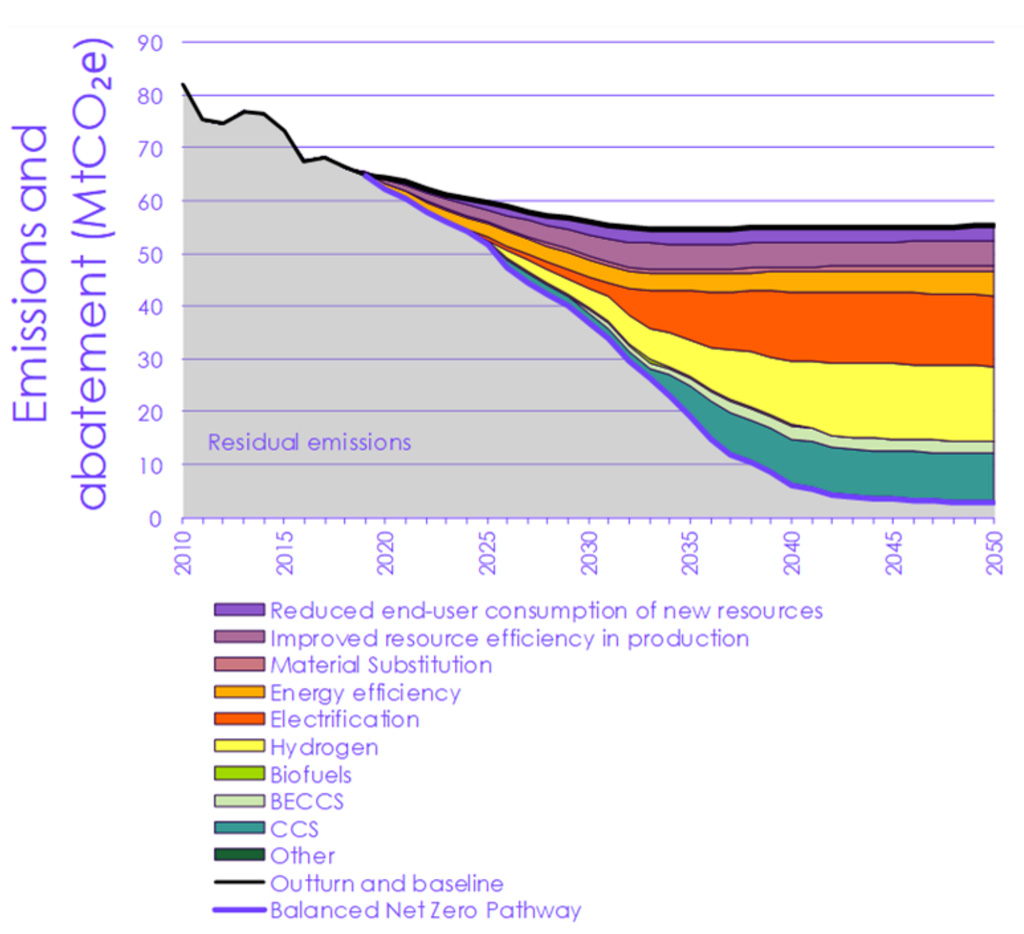

Manufacturing and construction

The CCC recognises that manufacturing and construction are among the most challenging of all sectors to fully decarbonise. It believes that existing policies – such as capital funding schemes, incentives and energy-efficiency strategies – are “insufficient” and “frequently piecemeal”.

Instead, it says the upcoming “industrial decarbonisation strategy”, due in early 2021, must rapidly accelerate progress by focusing on key areas, such as supporting job creation, fuel-switching to electricity and hydrogen, providing a “clear vision of the long-term policy mechanisms”, and setting target dates for “near-zero” emissions in the UK’s steel and cement industries (2035 and 2040, respectively).

The figure below shows the extent to which the CCC believes fuel-switching in particular can play, with electrification in orange and hydrogen in yellow accounting for more than half of the abatement across manufacturing and construction by the 2040s in the BNZ pathway.

However, the CCC highlights one other area for special attention. It states that the “design of policies…must ensure that it does not damage UK manufacturers’ competitiveness and drive manufacturing overseas” – something that many refer to as “carbon leakage”.

To date, the government has looked to the combination of an emissions trading scheme (ETS) with a free allocation allowance. But the CCC warns that, in the future, this “may not be the most efficient way to achieve the combined goals of deep decarbonisation and avoiding carbon leakage”. (The government has signalled that it will replace the EU ETS with a national scheme from January 2021, when the Brexit transition period is scheduled to end.)

The CCC recommends that “policies to protect competitiveness are likely to need to transition from being taxpayer-funded in the near-term towards applying border carbon tariffs or minimum [mandatory carbon] standards”. It adds:

“This transition reflects the likelihood that the government would seek to pass costs through to industry and subsequently consumers, once there is an alternative to subsidy mechanisms. The timing of this transition might be delayed in some areas where other benefits of subsidy approaches (such as reducing the risk from carbon pricing) make them desirable for longer. We estimate that providing support in this way would cost the exchequer around £2-3bn per year in the early 2030s, after which taxpayer support would fall.”

The CCC also notes that carbon prices and taxes on manufacturers are “currently below the levels that we estimate are consistent with our BNZ pathway”. It says they should be “strengthened” and that, additionally, “electricity pricing is reformed to reflect the much lower costs of supplying low-carbon electricity in the mid-2020s and beyond”.

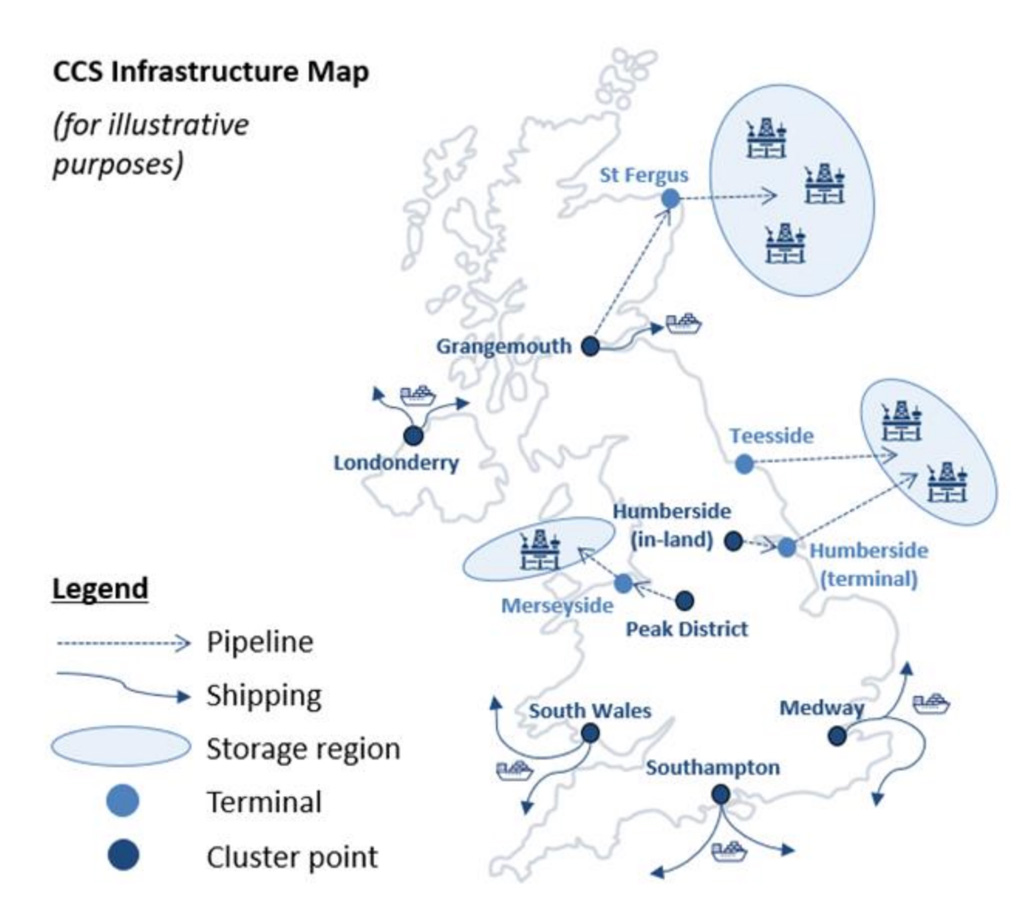

There will be a reliance on carbon capture and storage (CCS) across these sectors, stresses the CCC. It says that the government should establish “at least two CCS clusters (terminals or cluster points) in the mid-2020s, at least four by the late 2020s, and further clusters around 2030, to ensure our BNZ Pathway can be met”.

It includes an “illustrative” map, below, of “potential cluster points and terminals” around the UK.

terminals for CO2 transport and storage infrastructure. Source: Element Energy (2020) Deep-decarbonisation pathways for UK Industry, report for the Climate Change Committee. Taken from the CCC’s Policies for the Sixth Carbon Budget and Net Zero (2020).

Overall, the CCC estimates that its balanced net-zero pathway – when based on fuel-switching, CCS and improvements to resource and energy efficiency – sees manufacturing and construction emissions reduced by 70% by 2035 and 90% by 2040 from 2018 levels. It adds:

“We estimate the annualised cost of the BNZ pathway for manufacturing and construction to be around £1bn/year in 2030, £2bn/year in 2035 and reaching £4bn/year through the 2040s. In 2040 this represents an average cost of abatement across all measures of around £75/tCO2e.”

Electricity generation

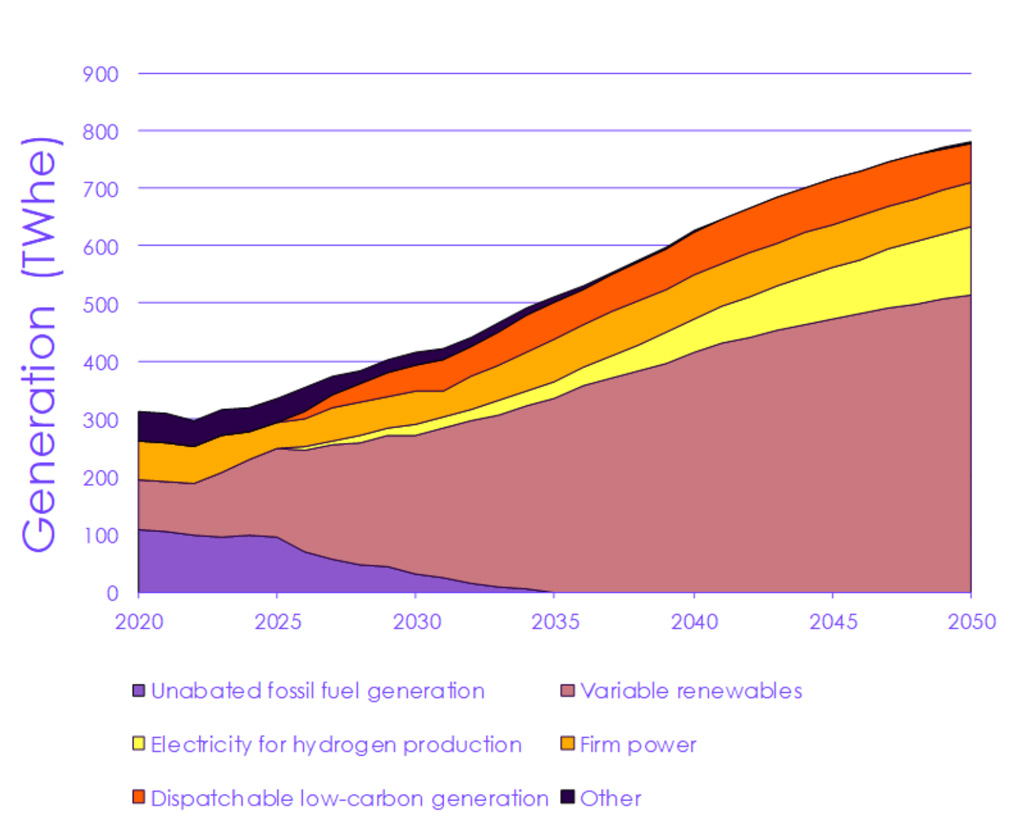

The CCC has a very ambitious vision for decarbonising the UK’s generation of electricity while, at the same time, seeing a dramatic increase in demand through the ramping up of electrification across a variety of sectors.

Overall, it recommends “fully decarbonising” electricity generation by 2035, while meeting a 50% increase in demand over the same period (and 100% by 2050), through:

- Delivering 485TWh of generation by 2035, which should all be low-carbon. This will require 400TWh of new low-carbon generation.

- Deploying variable renewables at scale, including 40GW of installed offshore wind capacity by 2030 and sustaining that build rate to support deployment of up to 140GW by 2050.

- Deploying at least 50TWh of dispatchable and flexible generation (e.g. gas CCS and hydrogen) by 2035 that can balance a system driven by renewables at low emissions.

- An increasingly flexible system, including from demand-side response (with 20% of demand being flexible in 2035), storage, hydrogen production and interconnection.

The CCC also urges the government – by the end of 2021 – to “commit to phasing-out unabated gas generation by 2035, subject to ensuring security of supply”.

It adds that any new gas power plants are “properly CCS- and/or hydrogen-ready as soon as possible and by 2025 at the latest”. To do so, the government needs to “ensure unabated gas generation faces a carbon price” which is consistent with this goal.

In addition, it says “no new unabated gas plant should be built from 2030 and those built prior to this should be suitable for retrofit”. And a range of barriers need to be “overcome” to ramp up low-carbon electricity at the scale required.

For offshore wind, it says “supply chains will require long-term signals over capacity needs to provide a predictable environment to investors and developers”.

Hydrogen plays a key role in all its scenarios, it stresses: “Policy will need to support the uptake of hydrogen in the 2020s and the accelerated deployment in the 2030s.”

By contrast, the CCC does not offer much in the way of advice about new nuclear power, other than to say: “The government should consider contracting models which help make new nuclear projects commercially viable for private developers.” It adds: “The BNZ pathway reaches 10GW of total nuclear capacity by 2035, with 8GW of new-build capacity.”

When it comes to storage, the CCC opts for hydrogen as the “primary source”, with an assumption that hydro stays roughly the same as now and batteries offering 18GW of “within-day flexibility” by 2035. Interconnectors triple from a capacity of 6GW today to 18GW by 2050.

Overall, the CCC presents an “illustrative” generation mix for its BNZ pathway, below, with “variable renewables” providing the majority of electricity supply from the 2030s onwards.

When it comes to the “cost” of transitioning towards a “near-zero” electricity system, the CCC says there is an additional cost in 2035 via the BNZ pathway of £3bn compared to a high-carbon system.

However, by 2050, these costs decrease with the uptake of “relatively cheap” renewables to the point where the cost saving reaches £5bn. The net result of this, says the CCC, is that, by 2050, the operational cost savings under the BNZ Pathway “more than offset” the additional investment required in electricity generation.

Fuel supply

To some extent, much of the CCC’s advice for decarbonising fuel supply echoes what it says for other sectors, such as manufacturing and electricity generation – for example, fuel-switching and CCS.

But the CCC does focus on three distinct areas: minimising methane leaks and flaring; decarbonising the supply of hydrogen; and improving the “sustainability” of bioenergy.

And it sees a lot of effort in the near-term with its BNZ pathway requiring fossil fuel supply emissions to be reduced by 75% by 2035 from 2018 levels.

In terms of recommendations across this sector, the CCC says that, from 2025, flaring and venting on offshore oil and gas rigs should “only be permitted when necessary for safety reasons”. It adds that the government “should work with industry and the international community to develop carbon-intensity (or broader) measurement standards for gas and oil” – and, to help achieve this, it should use its influence as the host of both the G7 and COP26 meetings in 2021.

The CCC also looks forward with hope to the government’s hydrogen strategy which it says will be published in “spring 2021”. The CCC says hydrogen end-use applications must grow and “make good progress” in the 2020s. However, when it comes to hydrogen production, it says:

“Our assessment of the path for build rates in the electricity system is that it will be highly challenging to provide very substantial volumes of electrolytic hydrogen over the period to 2040, while also meeting strongly growing demands for electricity during the 2030s. Thereafter, we anticipate that the rate of electricity demand growth will slow, enabling a more rapid scaling-up of electrolytic hydrogen supply with further deployment of zero-carbon generation.”

In the interim, it recommends a “blue hydrogen bridge”. (See Carbon Brief’s in-depth Q&A on hydrogen.) Additionally, it says that “requiring gas turbines and boilers to be hydrogen ready would reduce risks of them becoming stranded assets and would provide ready-made markets for low-carbon hydrogen”.

In terms of costs, the CCC says that the “costs of hydrogen supply will remain well above that of fossil gas supply before any carbon price, probably all the way to 2050”.

Despite all this, it still sees hydrogen demand growing significantly from near zero in 2025 up to beyond 200TWh in 2045, as the chart below shows.

Regarding decarbonising the supply and use of bioenergy, the CCC says the details of the government’s biomass strategy, due in 2022, will be “critical”. The CCC says its BNZ pathway sees overall primary bioenergy supply (including biomass, biogas, biofuels and the biogenic fraction of waste) available to the UK growing from 175TWh/year today to 225TWh/year by 2050.

And because 80% of bioenergy used in the UK will need to be linked to CCS by 2050, the CCC says a “significant investment programme will be required, with construction of new bioenergy facilities with CCS occurring in the late 2020s and early 2030s, across multiple end-use sectors – transport fuels, hydrogen, manufacturing and power”.

Overall, it says the cost of decarbonising the entire fuel supply sector will peak in 2040:

“We estimate the annualised cost of the BNZ pathway for decarbonising (mainly fossil) fuel supply to be around £1bn/year in 2030, peaking just below £2bn/year in 2040 before declining to £1bn/year in 2050s. In 2035, this represents an average cost of abatement across all measures of around £70/tCO2e.”

Agriculture and land use, land-use change and forestry

Progress in the sector of agriculture and land use, land-use change and forestry – known as “LULUCF” – has been “slow, with emissions broadly unchanged over the past decade”, the report says.

Some of the challenges of reducing emissions in line with a net-zero pathway include high upfront costs, price uncertainty in existing schemes and a lack of awareness on everything from low-carbon options for farmers to the climate impact of diets, the report notes.

The UK’s combined agriculture and land GHG emissions were 67MtCO2e in 2018, the CCC says, which could fall to 40MtCO2e by 2035 in the BNZ pathway. This would require a “transformation” in the way that land is used, the report says:

“Around 9% of agricultural land will be needed for actions to reduce emissions and sequester carbon by 2035 with 21% needed by 2050.”

This will require “investment of £1.5bn per year by 2035”, the CCC says, but “there will be co-benefits for health and recreation, air quality, flood alleviation and biodiversity”.

At the beginning of this year, the CCC published a report entitled, “Land use: Policies for a Net-Zero UK”, which “set out a comprehensive framework to deliver deep emissions reduction in agriculture and land”.

This framework was designed to deliver other objectives as well – such as adaptation and biodiversity benefits, the new report says. Key elements were endorsed by the UK Climate Assembly in its own report, the CCC adds.

The recommendations in the land-use report “remain valid”, the CCC says, and so they are set out in the new report again.

The CCC suggests that regulations should be strengthened to make sure “low-regret” options are taken up. This includes banning “damaging practices such as rotational burning on peatland and peat extraction” and “ending the sale of peat for horticultural use”. Rules could also oblige “water companies to restore peatland on land they own”, the report adds.

More costly measures require funding, the CCC says. It recommends auctioned contracts – similar to those offered for renewable electricity – or a carbon trading scheme for “afforestation and some agroforestry schemes”. Meanwhile, public funding should be used to “encourage the non-carbon benefits of afforestation” – such as recreation and reducing flood risk – and for peatland restoration.

The combination of full restoration of upland peat by 2045 and re-wetting and sustainable management of 60% of lowland peat by 2050 would deliver annual savings of nearly 6MtCO2e by 2035 and around 10MCO2e by 2050, the CCC says.

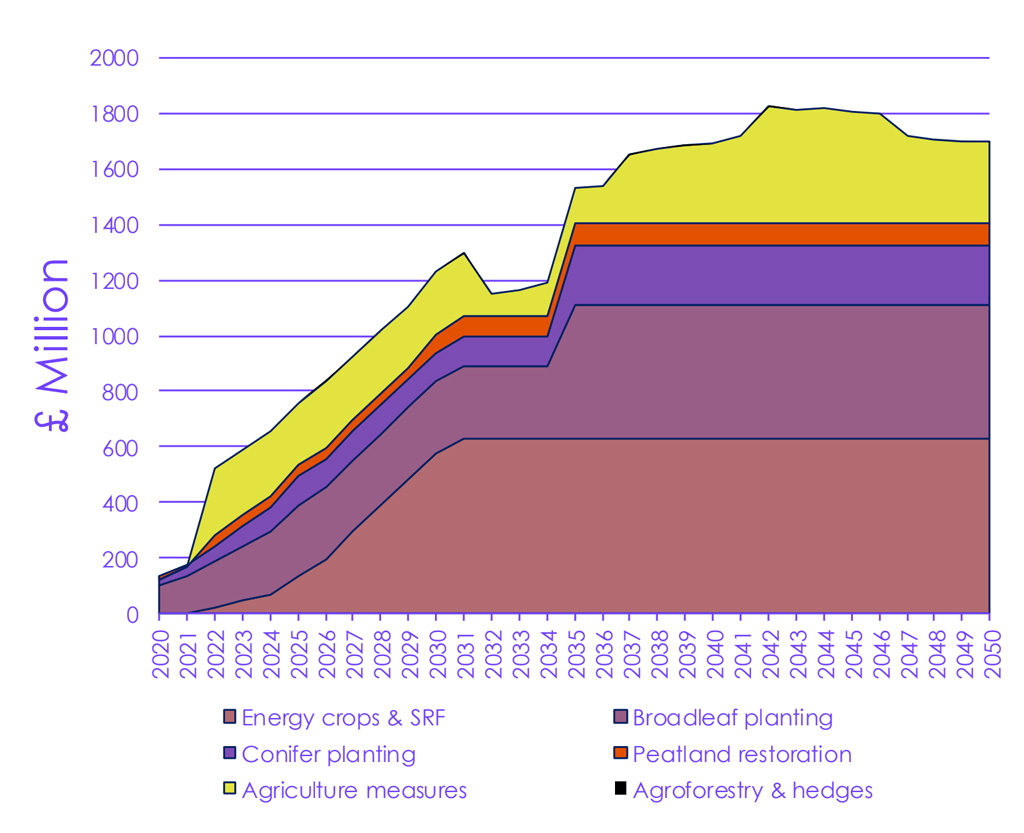

The BNZ pathway requires net investment of £1.5bn in 2035, the CCC says, with £1.4bn in the land sector and £0.1bn for agricultural measures. As the chart below shows, woodland creation and energy crops are the most significant source of costs.

Agricultural vehicles, buildings and machinery are also significant sources of emissions – 4.6MtCO2e per year – the report says. The CCC’s BNZ pathway “assumes biofuels and electrification options are taken-up from the mid-2020s and hydrogen from 2030, reducing emissions to 2MtCO2e in 2035”.

For non-financial barriers, the CCC recommends supporting schemes to “strengthen skills, training and market commercialisation of innovative low-carbon farming options”. It also suggests that reviewing the tax treatment of woodlands to ensure farmers are not penalised for creating forests on their land.

To support these changes, policies are also needed to help shift diets and reduce food waste, the report says. These include implementing “low-cost, low-regret actions to encourage a shift away from meat and dairy”, target setting for food waste reduction and “interim policies” to avoid a delay in action while waiting to implement the new framework.

For example, the BNZ pathway “involves a 20% shift away from meat and dairy products by 2030, with a further 15% reduction of meat products by 2050”. It also assumes that “food waste is halved across the supply chain by 2030”.

Aviation and shipping

The UK has played a key role at ensuring progress at both the International Civil Aviation Organisation (ICAO) and International Maritime Organisation (IMO), the CCC says.

However, these sectors are global in nature and the report warns that a unilateral UK approach to reducing emissions could be detrimental. It also notes that progress in decarbonising these sectors has been slow and changes in emissions have mainly been driven by changes in demand.

On aviation, the report finds that the government should commit UK international aviation to reaching net-zero by 2050 at the latest, with UK domestic and military aviation potentially reaching this target earlier.

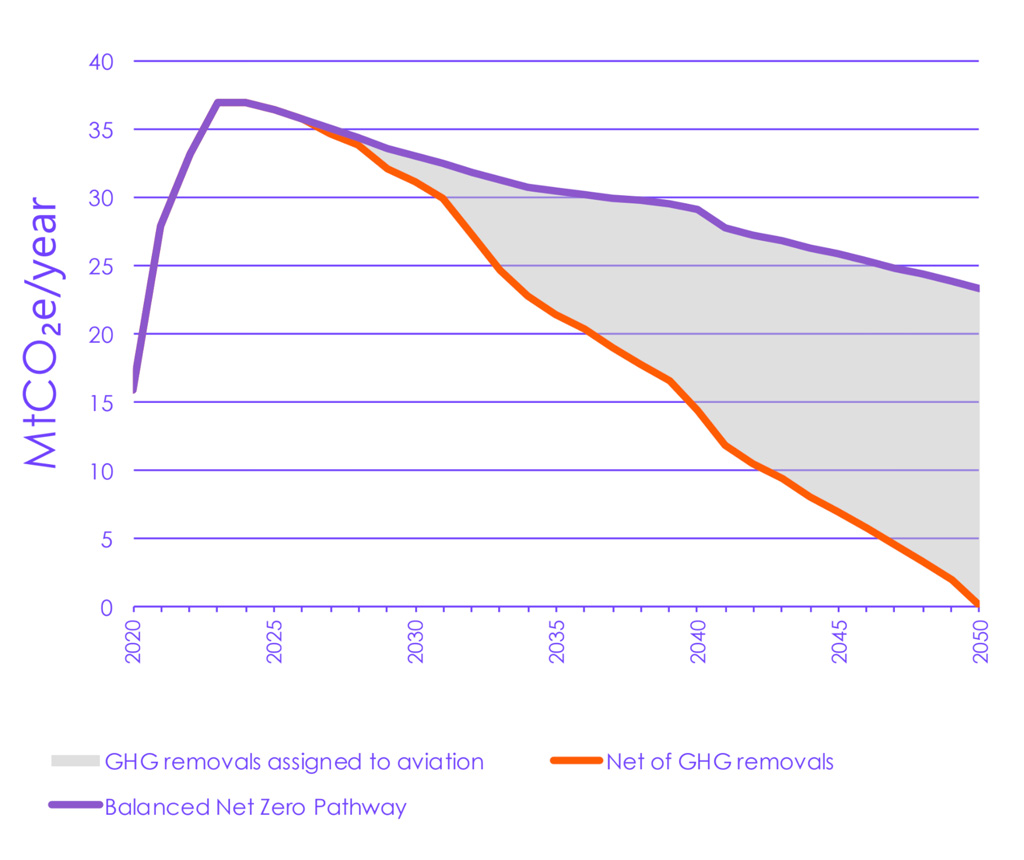

Following the BNZ pathway, the aviation industry should reduce its emissions to 23MtCO2e/year in 2050 and use greenhouse gas removal technology to make up for these emissions, the CCC says. This approach would mean that 40% of UK engineered greenhouse gas removals at that time is assigned to making the aviation sector net-zero.

The pathway to 23MtCO2e/year in 2050 is shown in the chart below.

The report recommends work on sustainable aviation fuel (SAF), finding that a SAF mandate is likely to be more effective than methods such as emissions trading schemes or carbon taxation.

Furthermore, the CCC says, there must be no net expansion of UK airport capacity unless the sector is on track to sufficiently outperform its net emissions trajectory and can accommodate the additional demand. The growth in demand for aviation will also need to be “constrained to 25% growth by 2050 from 2018 levels”, it adds.

On shipping, the IMO has agreed to reduce global international shipping emissions by at least 50% by 2050 compared to 2008 levels, the CCC notes, with an intermediary checkpoint of 40% improvement in carbon intensity compared to 2008 levels by 2030.

However, the report states that more “stretching” targets should be introduced for new ship and fleet efficiencies, as fleet carbon intensities have already improved by 30% from 2008 to 2018.

The government should also commit to the delivery of “a phased roll-out of clean maritime clusters”, the report states. The UK’s first clean maritime cluster at commercial scale should supply more than 2TWh/year of zero-carbon fuels and be operating by 2030 at the latest. The report recommends a “roll-out during the early 2030s to achieve a 33% share of zero-carbon fuels being used in UK shipping by 2035”.

Waste

Emissions from waste originate mostly from decomposition of organic matter in landfills, wastewater treatment processes and combustion of residual waste in energy-from-waste (EfW) plants, the CCC says.

The report notes that “good progress has been made in decarbonising waste in the past three decades”, which has mainly come from using taxes to reduce the waste that is sent to landfill. However, “recent years have seen sector emissions stalling”, the report says, “with increases in energy-from-waste plant emissions”.

The CCC says further progress requires a “step towards a circular economy” at local, regional and national levels. As changing waste management practices can be a relatively slow process, the CCC warns that “the waste sector requires new policy urgently”.

The CCC’s BNZ pathway would see “waste sector emissions fall 75% from today’s levels to reach 7.8MtCO2e/year by 2050”.

The report also notes that the sector faces a number of challenges, including “diffuse sources and incomplete data, locational and quality variations, a growing population, time lags, long-term contracts and the current lack of carbon capture and storage (CCS) infrastructure in the UK”.

In addition, waste policy “is mainly devolved”, the report notes, which means each nation within the UK has its own starting point, targets and regulations.

This means, for example, that the CCC’s recommended 2030 targets for recycling rates – for all wastes – differ across the UK. The report sets 68% and 70% targets for England and Northern Ireland, respectively, and notes that Wales and Scotland already have 70% targets for 2025. These should be formalised in legislation, the CCC says, and then exceeded for 2030.

The CCC also recommends that “biodegradable waste should be banned from landfill by 2025”, which would include “at least paper and cardboard, food, textiles, wood and garden wastes”.

As mentioned in the agriculture and land use section above, the CCC also highlights the importance of reducing food waste. It notes that “mandatory business food waste reporting will help achieve reductions in food waste”.

The CCC says the UK “should work towards banning the export of waste” by 2030, but warns that “full landfill waste bans should not be rushed”. While landfill bans could provide “modest reductions” in methane emissions, the CCC warns that the growth in EfW plants could see the sector’s emissions rise if they continue to be built without the option of CCS available.

Policies are also needed to “provide incentives for landfill operators to invest in increasing methane capture rates over time”, the report says.

Finally, on emissions from wastewater treatment, the CCC says that Ofwat – the UK water industry regulator – “should include sector decarbonisation as one of its core principles”.

In its BNZ pathway, the CCC estimates total additional investment costs above the baseline of around £175m/year in 2035 and £2.1bn/year in 2050.

F-gases

The CCC report dedicates a whole chapter to “F-gases”, which is a catch-all term for synthetic fluorinated gases – such as hydrofluorocarbons (HFCs) and sulfur hexafluoride (SF6). They are mainly used in fridges and air conditioners, but also in fire extinguishers and as solvents.

HFCs were designed as a replacement for ozone layer-damaging chlorofluorocarbons (CFCs), but they are potent greenhouse gases – as much as several thousand times better at absorbing heat than CO2. They “can stay in the atmosphere for centuries”, the report notes.

The UK has “signed up to a strong international legal framework for reducing F-gas emissions in the Kigali Amendment to the UN Montreal Protocol”, the report notes. However, the UK should go beyond these requirements, the CCC says, though the government is “yet to publish a plan to restrict the use of F-gases to the very limited uses where there is no viable alternative”.

The CCC recommends that the government “should bring forward such a plan as part of its net-zero strategy”. In particular, the plan should “ensure that any increase in ambition in EU F-gases regulation is matched or exceeded by the UK”, the report says.

The report notes that “a host” of options are “already available on the market” – including F-gases with a lower warming impact and F-gas alternatives. “Innovation will likely bring more forward,” it adds.

In addition, the UK should “minimise non-compliance”, the CCC says, including ensuring that the Environment Agency is “sufficiently resourced” to carry out “adequate inspections”. The government should also “bring forward proposals to ensure that all those who handle refrigerants have up-to-date training”.

Finally, the CCC recommends encouraging the use of more sustainable inhalers in the NHS. This includes educating practitioners and patients “about the global warming effects of medical inhalers and the importance of proper disposal”.

Greenhouse gas removals

Greenhouse gas removals (GGRs) – also known as negative emissions techniques – “encompass a broad range of technologies”, the CCC says.

It mentions “nature-based removals such as tree-planting and peatland restoration” and “engineered removals such as wood in construction, bioenergy with carbon capture and storage (BECCS) and direct air capture of CO2 and storage (DACCS)”. It also notes that “though other forms of GGRs exist, they are not included in our scenarios”.

The chapter on agriculture and land use (above) focuses on how nature-based removals can be scaled up over time, so this section covers engineered removals and overarching policy.

The CCC also notes that they have a separate document on pathways, method and policy advice for GGRs, called “The Sixth Carbon Budget – Greenhouse Gas Removals”.

GGRs are “essential to meeting the UK’s 2050 net-zero target”, the CCC says, as they can help offset “residual emissions in our scenarios”. However, they “are currently not available at scale in the UK, outside of the land sector”, it notes, and their costs are “potentially large”.

For example, the BNZ pathway estimates that “scaling up engineered GHG removals is likely to lead to added costs of £2.3bn/year in 2035 and £5.7bn/year by 2050. DACCS does not contribute in 2035, but will make up around 15% of removal costs in 2050”.

The average cost of removals in the CCC scenarios is “around £100/tCO2 during the 2030s and 2040s, although there is a wide variation in costs between sectors”, the report notes.

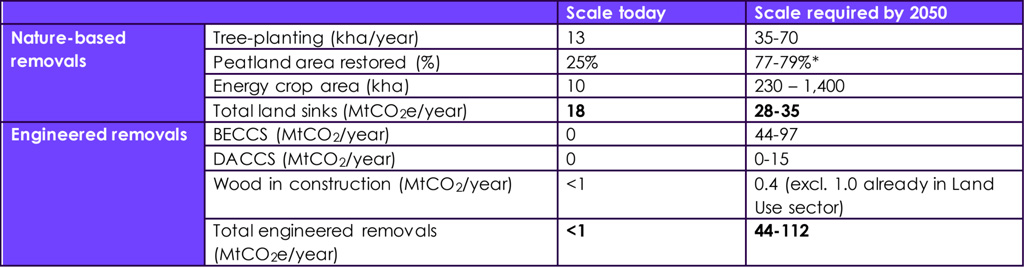

The table below shows the scale of GGRs at present in the UK and what the CCC says is required by 2050 to achieve net-zero.

Overall, the BNZ pathway estimates that “engineered emissions removals of 58MtCO2/year are required in 2050, in addition to nature-based sinks of 39MtCO2/year from UK land”.

As such, the sixth carbon budget pathway “requires that both land-based and engineered GGRs are available at scale by 2030”, the CCC says. This means that policy “will need to be developed in the first half of the 2020s” and it may “require initial support from the exchequer”. However, the CCC adds, “a longer-term vision for the sector could see emissions removals paid for by higher emitting sectors, such as aviation”.

The CCC sets out its policy recommendations in three sections: innovation support and enabling actions; scaling up GGRs in the UK; and the UK’s role in developing GGRs globally.

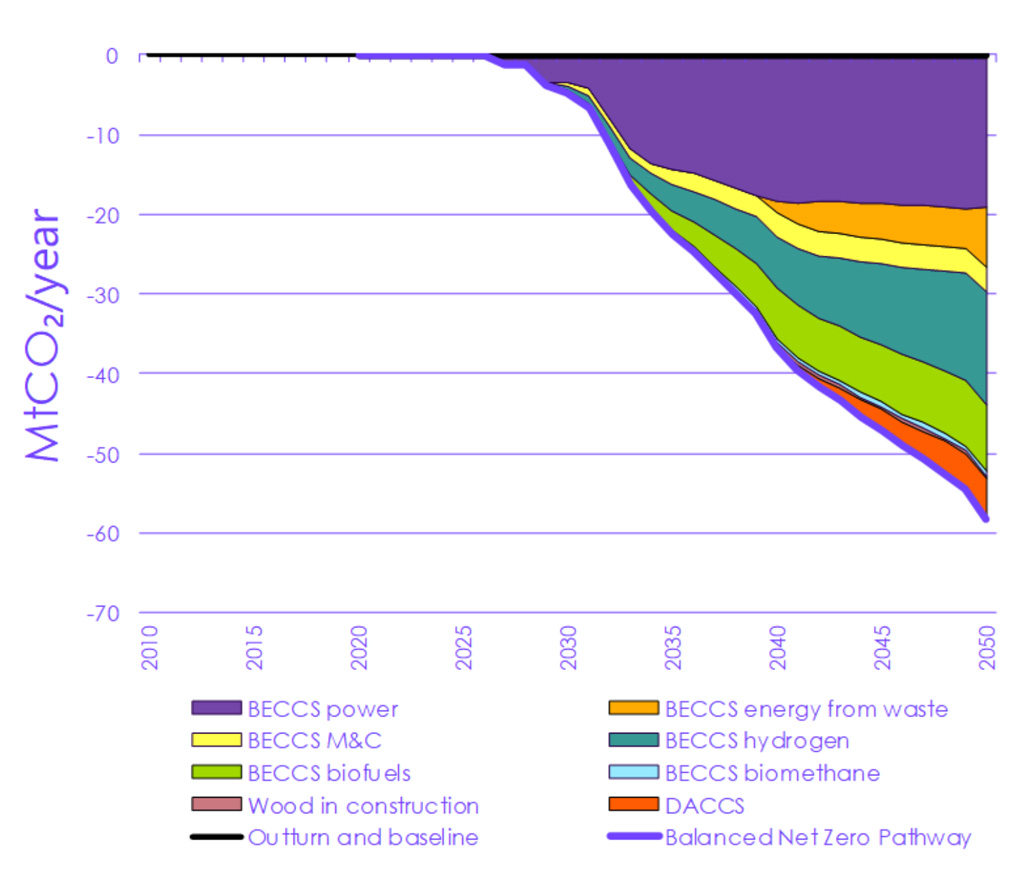

On innovation, the CCC says that for engineering GGRs to play a role, carbon capture and storage (CCS) deployment should start “as soon as possible”. This requires a “stable long-term policy environment”, it notes.

For BECCS, “near-term actions are required to ensure that the supply of sustainable low-carbon biomass can be scaled up to provide the necessary resource by 2050”, the CCC says. This involves “meeting and exceeding current tree-planting targets and overcoming the incentive barriers to the planting of sustainable perennial bioenergy crops on lower-grade agricultural land”.

The government also needs to bring forward “gasification” plants to turn biomass into energy carriers, such as hydrogen or biojet, the report says – and to re-examine its “gasification incentive scheme”, putting more emphasis on the transport sector.

On other GGSs – such as DACCS, enhanced weathering and biochar – the CCC recommends innovation and investment support. For example, field trials and experiments “can initially be delivered through the UK Greenhouse Gas Removal Demonstrators Programme”.

Successfully scaling-up GGRs to meet the net-zero target will “require funding, public support, rules and governance to ensure sustainability, placement within a wider net-zero strategy, a transition of biomass uses towards BECCS and a stable policy framework”, the CCC says.

The UK’s GGR strategy “can play a leading role in global policy development for greenhouse gas removals”, the report notes. For example, without safeguards, “large-scale harvesting of biomass can both be high-carbon and have substantial impacts on the provision of food, biodiversity and other sustainability concerns”. Strengthened governance is needed to manage these risks, the CCC says.

The UK can also “lead the development of international effort sharing frameworks for biomass-based GGRs”, the report says. It explains: “Many world regions will have either large potential biomass supplies or large CCS capacities, but not many countries will have both.”

Article 6 of the Paris Agreement “supports collaboration between countries to support higher mitigation ambition around the world”, the CCC says. The UK could, therefore, help “provide incentives to ensure that the world’s sustainable low-carbon biomass resource is used as efficiently as possible”.

-

CCC: UK must cut emissions ‘78% by 2035’ to be on course for net-zero goal

-

CCC: ‘Almost all’ investment must be zero carbon by 2030 to achieve sixth carbon budget