Climate finance: Funding a low-carbon global economy

Sophie Yeo

07.16.15Sophie Yeo

16.07.2015 | 3:00pmOver the next decades, trillions of dollars will be required to tackle climate change.

Leveraging it is a question that concerns politicians and financial institutions alike. Largely, it has been a conversation that the two have held separately.

The political discussion centres around a promise made in 2009 at the UN’s climate conference in Copenhagen, when developed countries committed to provide $100bn a year from 2020 to help poor nations reduce their emissions and adapt to the impacts of climate change, with a significant portion of this flowing through a Green Climate Fund.

Nations reaffirmed that pledge at the Financing For Development conference in Addis Ababa this week, where the UN largely focused on the issue of how to finance its post-2015 sustainable development agenda – a set of guidelines, to be finalised this September, on reducing poverty, hunger and climate change, among other issues.

$100bn may sound like a lot of money. It is. But the investment required to deal with climate change will likely cost trillions, as infrastructure and energy across the world reshape into a greener, more resilient form, compatible with a world where temperatures rise no more than 2C. Enabling this will require a rethink of how the financial system itself works.

Part 1: The $100bn-a-year promise

Unlike the vague trillions required for a low-carbon overhaul of the global economy, the $100bn is a precise figure embedded in a political agreement.

The text of the Copenhagen agreement states that this could come from a variety of sources: public and private, bilateral and multilateral, and alternatives. It also established a Green Climate Fund (GCF). This has been designed to channel a significant proportion of these funds, but by no means all of them.

Despite this, the GCF is often seen as synonymous with the $100bn pledge.

Green Climate Fund

Many poor nations are in a situation where their capacity to reduce their emissions is limited by a lack of funding. The GCF was established to ensure that developing countries have access to additional and predictable finance that will allow them to scale up their own efforts to tackle global warming.

Under intense pressure from campaign groups and developing countries, rich nations have already started to trickle public funds into the GCF. So far this amounts to $10.2bn, with much of this pledged at a Berlin meeting in November 2014. Others, including Australia, added to that sum at the UN conference in Lima.

To date, 58.5% of these pledges have been signed off by the donor nations into actual contributions, surpassing the 50% threshold required for the GCF to start allocating resources through bodies that have been approved by the board.

As a new financial institution, the GCF remains a work in progress.

Since it was established, countries have been debating issues such as what kind of projects it can fund (a complication that is exacerbated by the lack of an official definition of “climate finance”), who gets to disburse the money, and how it intends to manage financial risk.

Some observers are concerned about the lack of an explicit ban on fossil fuel projects for the GCF, following the revelation that Japan had used its early climate finance contributions to fund a coal plant in Indonesia.

Another challenge is ensuring that developing countries are ready to receive the funds. Héla Cheikhrouhou, executive director of the Green Climate Fund, said in a speech last month at the UN that, although $6bn had been requested from the fund so far, only $500m of this was from funds that “look promising”.

Private versus public

The extent to which the GCF will be publicly funded has become one of the most contentious issues in climate finance.

It is widely accepted that a portion of the $100bn will be from private sources, and the GCF has set up a Private Sector Facility to enable this.

The theory is that public money can unlock private investment in developing countries, where there can be significant barriers blocking the flow of funds into clean energy and infrastructure projects, for example.

Following advice from its Private Sector Advisory Group, the GCF has said that it will allocate up to $500m for mobilising these resources in the initial phase of the fund, up to 2018. It has also said that it will provide another $200m to support micro, small and medium sized enterprises working on climate projects.

But so far, there has been no official decision regarding how much money should be from private sources, and how much from public.

The developed countries responsible for filling the coffers of the GCF are keen to draw on private finance, as it eases pressure on their own budgets, as well as arguing that it aligns with the nature of the financial transformation required. Ed Davey, the former UK climate and energy secretary, said in an interview with Carbon Brief in March:

“There are some people I listen to at the UN who think that if climate finance is private money it’s somehow not climate finance. Well, I don’t think we can accept that. Climate finance is going to have to be both. And, actually, the more you can mainstream this into normal business, into the normal works of a normal market, the quicker we will tackle climate change.”

Others have argued that the private sector may struggle to meet the needs of the world’s poorest people, and should be approached with caution by the GCF.

The rest of the $100bn

Not all of the $100bn is required to flow through the GCF.

To date, contributions to the GCF total $10.2bn, with South Korea making the first donation in September 2013. This is a figure that is dwarfed by the sums of money that were already flowing from the developed to the developing world.

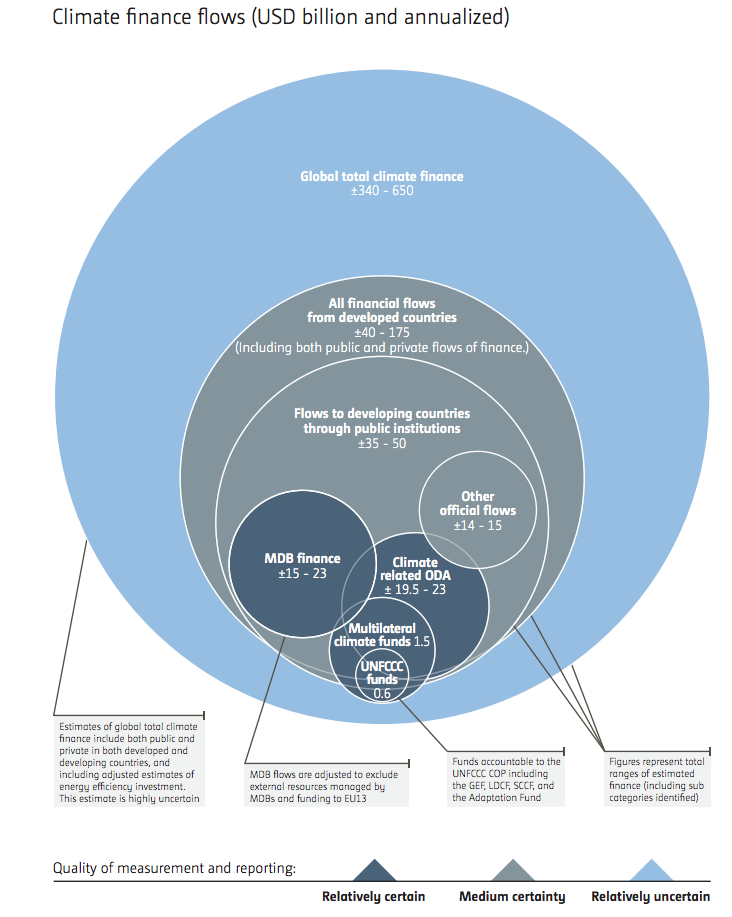

According to the 2014 biennial assessment by the UN’s Standing Committee on Finance, developed countries were already transferring between $40bn-175bn in climate finance a year between 2010 and 2012.

Between $35bn to $50bn of this was from public institutions, while between $5bn and $125bn was private finance.

Credit: UNFCCC, 2014 Biennial Assessment and Overview of Climate Finance Flows Report

Among this is money that governments have allocated to climate projects from their foreign aid budgets, in the form of bilateral projects, development banks and other multilateral bodies, such as the Adaptation Fund or the Global Environment Facility. For a case study, see Carbon Brief’s detailed assessment of how the UK spends its climate finance.

How these funds will operate in the future, should the GCF succeed in becoming the main vehicle for climate finance in the future, remains an unresolved issue.

Politics

The $100bn pledged through the UN may be small compared to the sums that will ultimately need to be mobilised, but this pot of money punches above its weight.

How the UN deal in Paris deals with finance remains an open question. When negotiators arrive in Paris this December, they will have to grapple with issues such as how financial contributions can be scaled up in coming years, and how such enormous flows of money can be measured and verified.

What is certain is that the ability of rich nations to deliver on their Copenhagen promise will determine the level of ambition and the level of trust shown by developing countries at the UN climate talks in Paris this December.

Under the 1992 UN Convention on Climate Change, which sets the rules for international climate action, rich countries have a duty to help poor nations cope with the financial burdens of climate change – a rule that the latter are keen to see honoured in the forthcoming agreement.

Without the appropriate signals from developed nations that they will scale up levels of finance significantly over the next five years, mistrust and bad feeling could make it harder to achieve such a deal.

Part 2: Beyond the United Nations

$100bn will not meet the scale of the climate change challenge. However, outside of this sum, the UN has no ability to raise funds. Generating the remaining trillions will be the task of the private sector: investors, asset managers, commercial banks and financial regulators, for example.

According to the Financial Stability Board, financial institutions held around $305tn in 2013. Not all of this is available for low-carbon investments, but even a small fraction of this could significantly boost progress towards tackling climate change.

The UN has estimated that the total amount of climate finance flowing each year between 2010 and 2012 was between around $340bn and $650bn, although it acknowledges that this estimate is highly uncertain.

It calculates that only $50bn of this at most was from public coffers, as the graphic above demonstrates. The rest of it came from private organisations. This money flowed without the prompting of the Green Climate Fund, which was still in its earliest phases at this stage.

Nonetheless, this will have to be scaled up dramatically over the coming years.

Take infrastructure, for instance – one of the principle arenas that has the potential to become cleaner and more resilient if it receives the appropriate investment. The recent findings of the Canfin-Grandjean Commission set up by President François Hollande ahead of the Paris summit in December show that, of the $5tn invested in infrastructure in 2013, only 7-13% of this could be considered “climate change compatible”.

“This portion of total investment is clearly insufficient,” says the report.

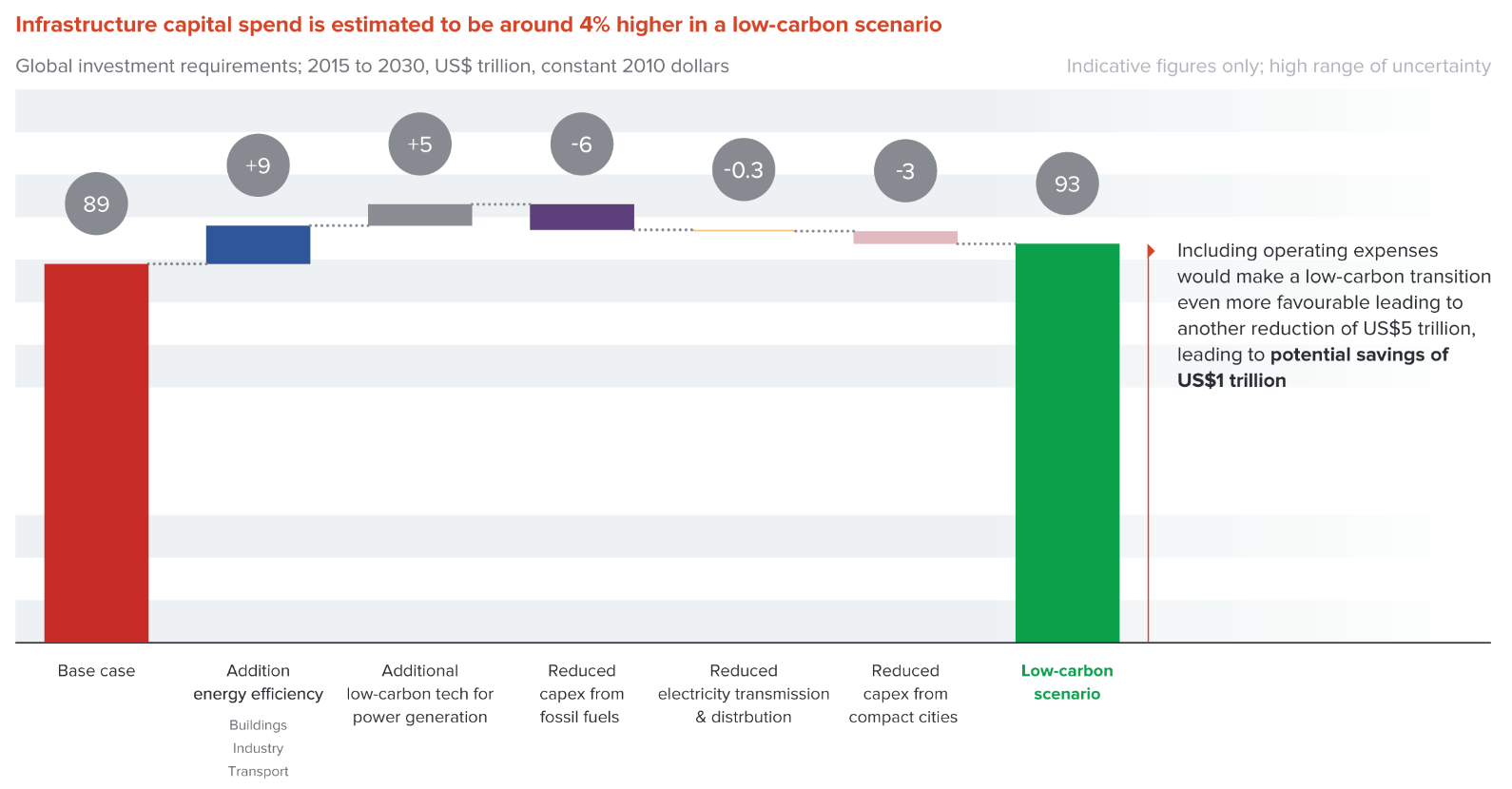

A separate report from the New Climate Economy released in 2014 found that a total of $89tn of infrastructure investment would be required up to 2030, with capital spend estimated to be around 4% higher in a low-carbon scenario, due to a combination of additional investments in areas such as energy efficiency and savings in costs such as fuel, as the graph below illustrates.

Source: New Climate Economy, 2014

But the additional sums of private finance will not flow by themselves. Financing a world that is low-carbon and climate resilient will require a different approach from the current carbon intensive model.

For instance, most climate-related investments have higher upfront costs and longer payback periods, and, therefore, a lower immediate return. New technologies can also carry greater risks in developing country markets, which can be another disincentive for investors.

There may also be a lack of expertise when it comes to delivering the project, including among the relevant financing, regulatory and governance institutions, or the capital markets, and financial instruments used to correctly price risk may be unavailable.

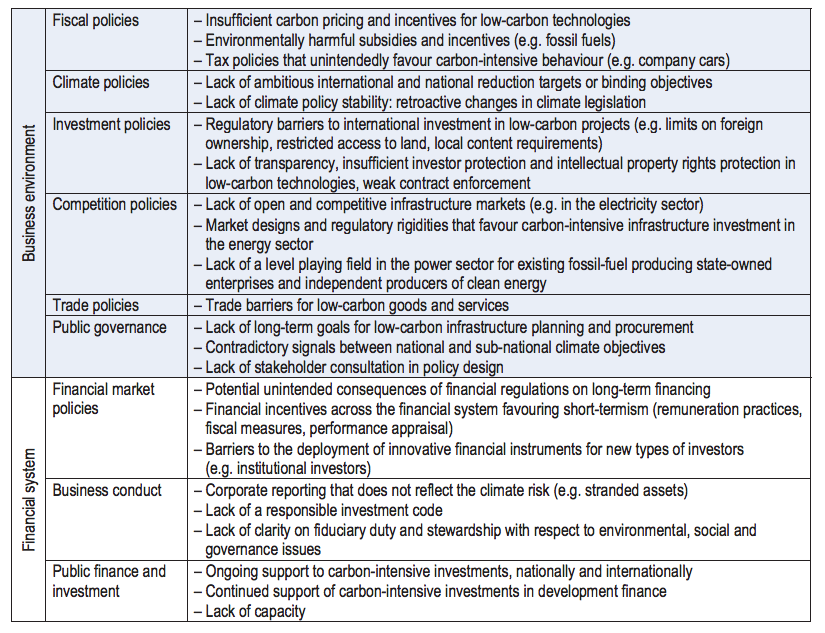

Sometimes, the reason for the lack of investment is that current policies are ill-equipped to encourage low-carbon investment. The following table sets some of these out in detail.

Source: OECD, 2015

A better policy environment and an innovative financial toolbox could enable investors to navigate this high risk environment. This is a topic that has already garnered interest and analysis at the highest levels.

For instance, the Organisation for Economic Co-operation and Development (OECD) recently published an in-depth report on how economies can restructure themselves away from fossil fuels and towards a 2C-compatible future.

“There is no one-size-fits-all strategy when it comes to policy reform,” says the report, but suggests a number of possibilities. These include a demonstrable commitment to low-carbon reform from governments, stable carbon pricing policies and facilitating access to financing instruments appropriate to green investments, such as credit enhancement, leasing, guarantees, grants and bonds.

Meanwhile, a report on the topic is expected from the Financial Stability Board in September or October this year, after G20 finance ministers mandated it in April to “review how the financial sector can take account of climate-related issues”.

In fact, a recent report into climate risk led by the UK Foreign Office states that “the proliferation of initiatives can be confusing to investors”.

The Pascal-Grandjean Commission proposed in its report a “low-carbon financial roadmap” that would prompt the shift towards a greener economy.

This would be largely shaped by existing bodies outside the UN, such as the G20, Basel Committee and the FSB, with the IMF and the World Bank charged with supervising and implementing it, suggests Pascal Canfin, a former French development minister who led the Commission.

Carbon Brief asked Canfin how such a roadmap might be built practically over the coming months and years. He said:

“How it will be shaped formally, it’s too early to say. If it happens, it will be shaped in October in the G20, in the next FSB meeting, and in Paris with the head of states’ declaration. That’s exactly the kind of paragraph you can have in a head of states and government declaration in Paris. It’s outside the [UN Paris] agreement. It’s political.”

Conclusion

Tackling climate change requires a lot of money. Mobilising these funds is a task for both politicians and the financial sector.

But, as the New Climate Economy points out, it will also save a lot of money – potentially trillions – as fossil fuels are phased out and the share of renewable energy increases.

But the benefits aren’t purely financial. Limiting global warming and preparing citizens to deal with the impacts of climate change will also better protect the world’s poorest and most vulnerable communities.

Main image: Wall Street sign, New York.

-

Over the next decades, trillions of dollars will be required to tackle climate change. Leveraging it is a question that concerns politicians & financial institutions alike.