Factcheck: The steel crisis and UK electricity prices

Simon Evans

10.22.15Update 8/4/16 – BBC News is reporting on Tata Steel’s windfall profits under the EU’s carbon market, an issue highlighted by Carbon Brief in October. We have added a chart to the article, below.

Update 1/4/16 – Tata Steel is planning to sell its UK assets, including the Port Talbot steelworks in south Wales. The news has once again prompted finger-pointing at UK electricity prices and policy costs. Meanwhile, an additional tranche of policy cost-compensation has kicked in. We have updated the article, below.

Update 4/4/16 – For a long list of commentators once again blaming the steel crisis on climate policy, see our 4 April daily briefing. We have also added updates on EU ETS windfall profits and global variations in steel production costs.

The UK steel industry is in disarray after SSI closed its Redcar steelworks, Caparo Industries went into part administration and Tata Steel announced 1,200 job losses.

The growing crisis has grabbed wide media and political attention. Chinese premier Xi Jinping’s state visit in autumn 2015 threw the spotlight on alleged dumping of cheap Chinese steel on world markets. Yet some commentators have also pointed the finger at UK electricity prices.

Carbon Brief looks at the facts around the steel crisis and UK electricity prices.

Steel – going cheap

The crisis in the UK’s steel industry has been triggered, first and foremost, by plunging global steel prices. These have halved in the past year, the BBC says, taking prices below 40% of a 2011 peak, as the chart below shows.

The price of steel from March 2009 to October 2015. Source: Bloomberg/BBC.

Richard Warren, senior energy and climate policy adviser at manufacturers’ organisation EEF, tells Carbon Brief that falling prices have been the biggest factor in squeezing steelmakers’ margins.

Announcing its decision to axe 1,200 jobs, Tata Steel said it was:

“[A] response to a shift in market conditions caused by a flood of cheap imports, particularly from China, a strong pound and high electricity costs.”

By autumn 2015 sterling had risen 17% in two years, according to the Bank of England. This makes imported steel cheaper relative to UK production.

Notably, in Tata Steel’s 2014/15 annual report, UK energy costs are not mentioned. Instead, its focus is on high pension liabilities, the strong pound and weak domestic demand.

Expensive electricity

Nonetheless, high UK electricity costs have caught the imagination of several newspaper articles and commentators. The Times says UK industry is being “crippled” by electricity costs twice those in Germany. The Telegraph says UK energy policy is putting the steel industry at risk.

For industry, it makes sense to focus on energy costs, since the government has some (limited) control over them. Industry is much less likely to achieve change in world steel prices or the value of the pound. The current crisis also makes government more receptive to industry’s pleading.

Still, EEF’s Richard Warren tells Carbon Brief:

For Leo McKinstry in the Express and Dominic Lawson in the Mail, however, the real problem is the “green agenda” and our “idiotic leaders” who are “obsessed with being green”. For them, it is the UK’s climate change policies that are driving up energy prices and putting the steel industry at risk.

Several of the articles compare UK prices to those in France and Germany, which they say are half those in the UK. One of the articles even claims the UK has the world’s highest energy costs.

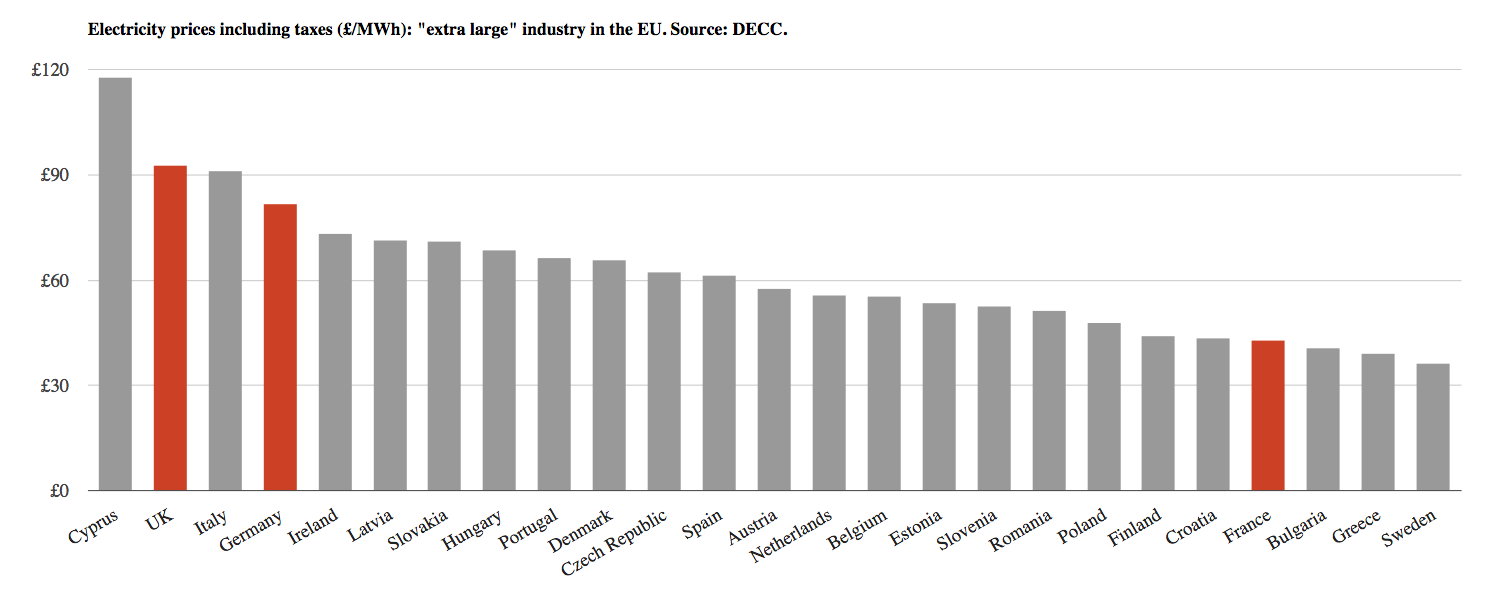

The Department for Energy and Climate Change (DECC) regularly publishes data on electricity costs faced by different industrial sectors. For “extra large” industry, which probably includes the steel sector, the UK does have relatively high electricity costs, though not the highest in the EU.

Electricity prices in £/MWh, including taxes, faced by “extra large” industry around the EU. Data covers the second half of 2014 but recent trends indicate the relative position of countries has remained relatively stable in recent years. The figures do not account for compensation received by heavy industry in countries including the UK and Germany, which reduce the price faced by steel firms, see below. Source: DECC. Chart by Carbon Brief.

The data is somewhat at odds with the claim that UK costs are “twice” those in Germany, though again, it’s hard to compare because the figures are pre-compensation. In terms of raw pre-compensation prices, however, UK costs do seem to be twice those in France. It’s possible that particular sectors or individual companies are able to secure more favourable contract terms with their electricity suppliers.

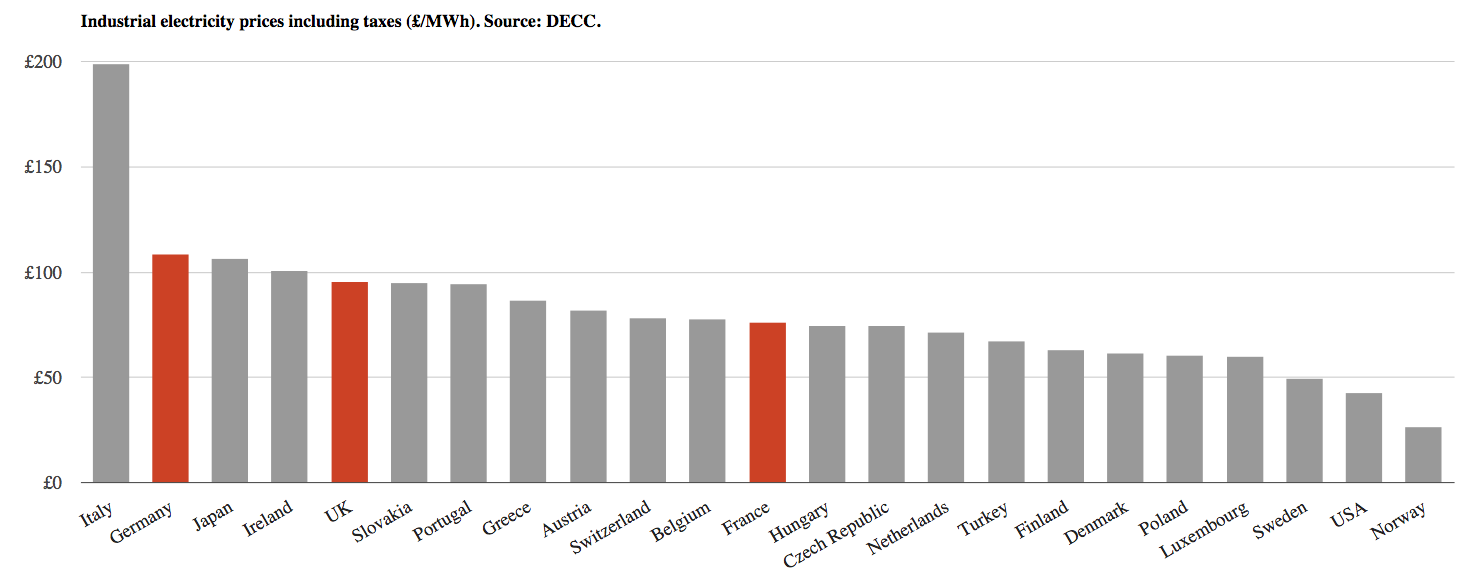

DECC also publishes data looking more broadly at electricity costs for industry as a whole, in a range of countries around the world. It’s worth noting that Italy, Germany and Japan all have larger steel industries than the UK.

Electricity prices including taxes for the whole industrial sector (£/MWh) in a range of industrialised countries. Data for 2014. Source: DECC. Chart by Carbon Brief.

Regardless of the relative prices in different countries, however, there’s a major problem with the argument that expensive electricity is at the heart of the UK steel industry’s problems. This is that electricity makes up a tiny share of steel production costs.

Raw material, freight and labour costs make up the majority of production costs. These can vary significantly between countries. UK labour costs of around $200 per tonne of steel, for example, are some 20-fold higher than the $10 per tonne in China. Raw material costs and freight costs appear to show relatively wide variation between countries, despite global trade.

The share of electricity in steel production costs is around 6%, according to one estimate for blast-furnace steel production, used at most major steelworks. The Committee on Climate Change (CCC) says energy makes up 5.2% of costs for “basic metals”, which includes steel. The CCC says it is around 6% for integrated steelworks like Port Talbot.

EEF’s Warren confirms this. He tells Carbon Brief that electricity accounts for around 6-8% of UK steel production costs. Of the UK electricity cost for heavy industry, he says that about a third — £31.50 per megawatt hour (MWh) — is due to policy costs during the 2016/17 financial year. Wholesale costs, transmission and distribution costs and power company profits make up the remaining two thirds.

Policy costs

So, perhaps 2-3% of UK steel production costs might be down to government policy. In fact, the steel industry does not have to pay the full costs of government policy. It receives compensation that offsets 60-70% of cost of CO2 pricing, says Warren.

Compensation for 85% of the cost of low-carbon energy subsidies started in February 2016 and will be backdated to December. This reduces the total policy costs faced by much of the steel industry to around £7/MWh, according to EEF. This amounts to much less than 1% of production costs.

After this compensation is taken into account, UK electricity costs for steel firms are around £70/MWh. This is still high relative to many other EU countries. Even if all green policy charges were scrapped, however, UK prices would remain higher than for most EU competitors.

German heavy industry — cited by several of the articles mentioned above — is exempted from the majority of policy costs. Instead, it is German households that bear the burden. German industry also benefits from very low wholesale electricity prices, which is partly the result of renewables generating at near-zero marginal cost.

Like in Germany, the UK’s homes and other businesses are now cross-subsidising policy-cost exemptions for heavy industry. This cross-subsidy adds about as much to consumer bills as will be saved by the government’s cuts to renewable energy support since it took office in May 2015.

The steel industry has also historically received generous free CO2 allowances to cover emissions governed by the EU’s Emission Trading System (EU ETS). As a result, the scheme has been a source of revenues as well as costs.

For instance, between 2008 and 2015 Tata Steel received 85m more free allowances than it needed to cover actual emissions, according to campaign group Sandbag. These surplus allowances netted the firm €600m, Sandbag says, equivalent to £520m.

Within this, the Port Talbot plant received around 5m excess free allowances, Sandbag says. These would have earned it a cumulative total of €92m (nearly £80m).

Large emitters such as Tata Steel may also have earned so-called windfall profits. These occur where firms raise their prices to customers to cover the costs of the EU ETS, even though they have received EU ETS allowances for free.

Tata Steel is likely to have netted around €1bn (£841m) from such profits between 2008 and 2014 says Emil Dimantchev, carbon market analysis at Thomson Reuters.

The true figure could be even higher, depending what percentage of the CO2 price was passed through to customers. Dimantchev’s analysis uses 55%, which he says is conservative. Tata’s Port Talbot site in Wales could have earned €299m (£254m) in windfall profits between 2008 and 2014 alone, he adds.

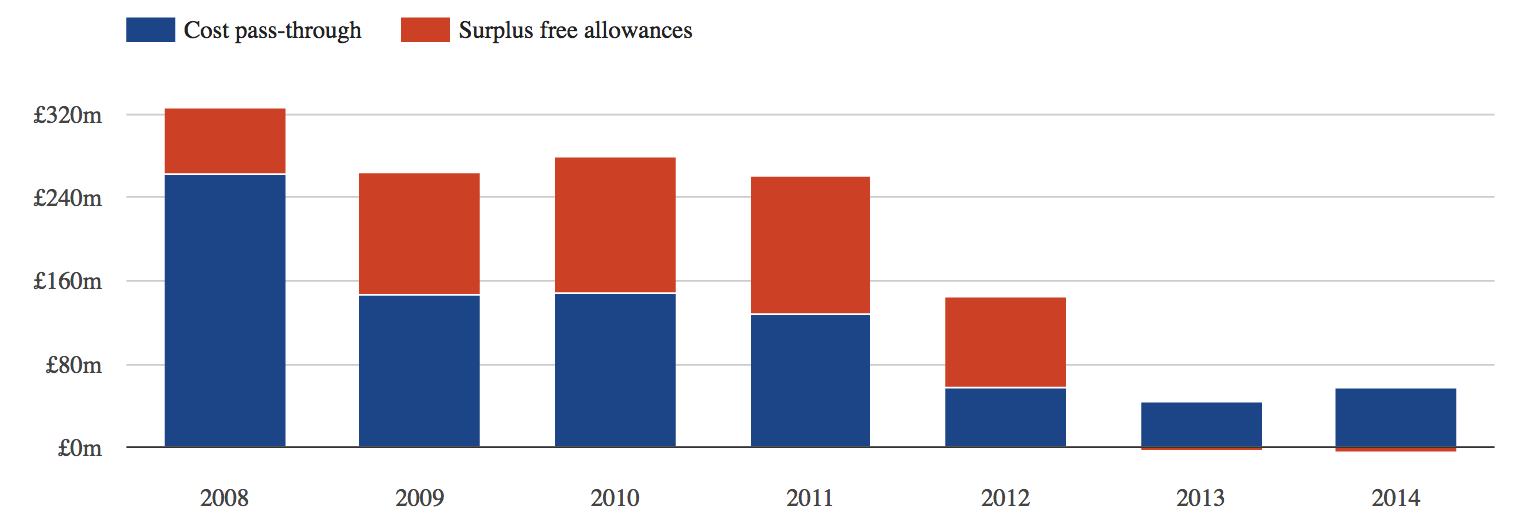

Carbon Brief has combined Dimantchev’s estimates of cost pass-through windfall profits and Sandbag’s estimates of surplus free allowance profits in the chart, below.

A separate study, prepared by consultancy CE Delft for NGO Carbon Market Watch, says Tata Steel’s UK operations have earned around £700m in total from the EU ETS since 2008. This includes the sale of surplus allowances and estimated windfall profits from cost pass-through.

Estimated Tata Steel Europe profits and costs under the EU ETS

Tata Steel Europe’s estimated profits and costs under the EU ETS between 2008 and 2014. Blue: Windfall profit from passing an estimated 55% of the cost of CO2 allowances through to customers, even though most allowances were received for free. Red: Profit or cost of CO2 trading, after setting Tata’s actual emissions against free EU ETS allowances. The figure accounts for Tata’s use of cheaper international CO2 credits to some cover emissions. Sources: Thomson Reuters and Sandbag. Chart by Carbon Brief.

Responding to reports about its windfall profits under the EU ETS, a Tata Steel spokesperson said in a statement sent to Carbon Brief:

Tata Steel Europe had a small shortfall of free permits across its EU sites in 2013 and 2014, as you can see in the red bars on the chart above. The cost of this shortfall was an estimated £5m for the group as a whole in 2014. Port Talbot had estimated costs of £7.4m that year, suggesting other parts of the group still had excess free allowances.

Tata Steel also disputes the idea that it earned large windfall profits from cost pass-through. It points to comments from Eurofer, the European steel industry association, which calls the 55% figure and the study it was based on “absurd and misleading”.

However, a review prepared for the European Commission cites three other pieces of research which each reach similar conclusions on the likely existence and level of cost past-through. The review says:

Conclusion

Can policy costs, making up much less than 1% of steel production costs, really be responsible for the current crisis in the industry? In a blog written in early 2015, EEF’s Warren says that even tiny percentages like this can make the difference between profit and loss, given “razor thin margins”.

Yet, as we’ve seen, Warren agrees that the industry’s biggest problem is falling steel prices.

23/10/15 – We added a note from Jeremy Nicholson regarding electricity prices for “extra large” industry around the EU.

5/4/16 – Emil Dimantchev corrected an error in the figures he presented for EU ETS windfall profits. We have amended the article. We also updated the figures on income from excess EU ETS allowances, following an update from Sandbag.