IEA: Mineral supplies for electric cars ‘must increase 30-fold’ to meet climate goals

Josh Gabbatiss

05.05.21Josh Gabbatiss

05.05.2021 | 6:00amAt least 30 times as much lithium, nickel and other key minerals may be required by the electric car industry by 2040 to meet global climate targets, according to the International Energy Agency (IEA).

These metals are among a handful that are considered vital in the manufacture of solar panels, wind turbines and other clean energy technologies.

Overall, the Paris-based organisation says the production of these key minerals may need to quadruple over the next two decades to achieve the Paris Agreement target of limiting warming to “well below” 2C, or expand by as much as six times to reach net-zero globally by 2050.

Its new report examining the status of these minerals concludes that today’s supply and investment plans “fall short” of what will be necessary for a widespread clean energy transition.

The IEA report examines the barriers – some of which have previously been covered by Carbon Brief – that could prevent the mineral industry from scaling up to meet this future demand.

However, in an introduction to the report, IEA executive director Dr Fatih Birol writes:

“These hazards are real, but they are surmountable. The response from policymakers and companies will determine whether critical minerals remain a vital enabler for clean energy transitions or become a bottleneck in the process.”

Higher demand

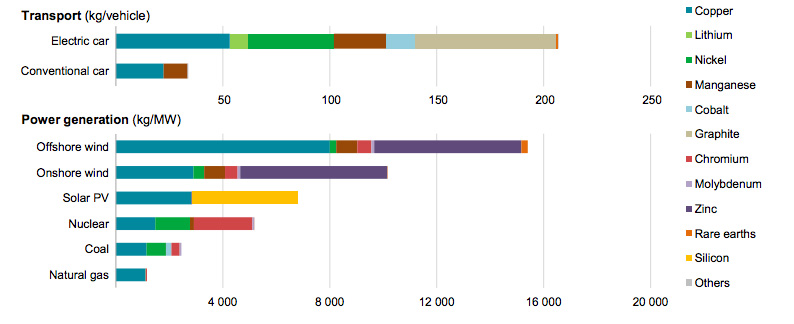

Broadly speaking, the mineral demands of clean energy technologies are greater than their fossil-fuelled counterparts, the IEA says.

This can be seen in the chart below, which shows how an offshore wind plant today requires around 12 times more mineral resources than an equivalent gas plant.

According to the IEA, the rise of renewable power in recent years means that since 2010 the average amount of these minerals required for a new unit of power generation capacity has increased by 50%.

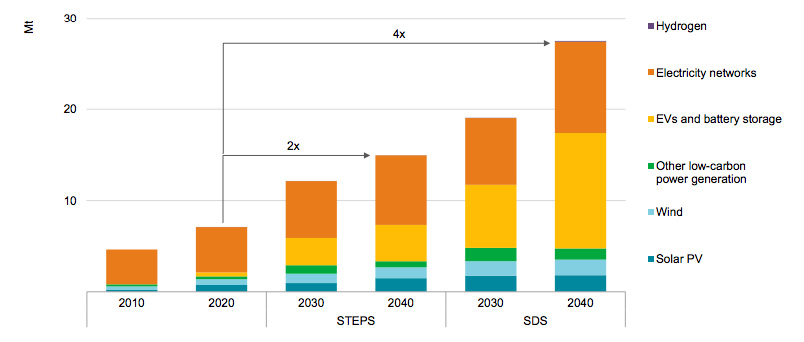

In its new report, the agency assesses future demand for these metals in different energy applications under two different scenarios, which see overall demand either doubling or quadrupling, as the chart below shows.

First is the IEA’s “sustainable development scenario” (SDS), which it says is aligned with the Paris Agreement target of holding warming at “well-below 2C”.

While the IEA’s SDS and its alignment with the Paris Agreement has been disputed, the report also mentions a “dramatic extra push” needed to achieve global net-zero by 2050. The agency is expected to release a “comprehensive roadmap to net-zero emissions by 2050” in the coming weeks.

The new report also uses the “stated policies scenario (STEPS)”, which “provides an indication of where today’s policy measures and plans might lead the energy sector”.

It combined clean energy trends primarily from the World Energy Outlook 2020 with new analysis of changes in mineral usage based on “extensive literature review, and expert and industry consultations”.

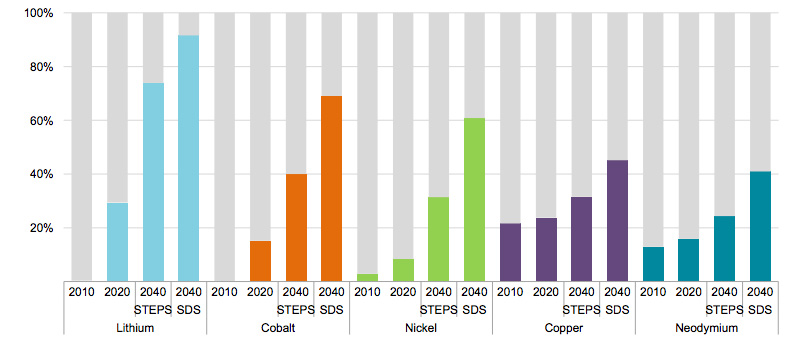

Under the SDS in particular, clean energy technologies’ share of total mineral demand is set to rise significantly, becoming the primary market for nickel, cobalt and lithium. This can be seen in the graph below.

Material needs

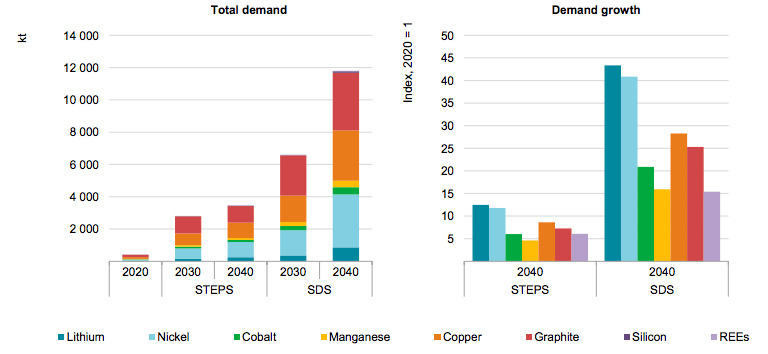

Electric vehicle batteries and battery storage are expected to be by far the biggest contributor to the future surge in demand, with lithium, nickel, cobalt, manganese and graphite all crucial for ensuring performance, longevity and energy density.

In the SDS, mineral demand from the battery sector grows around 30-fold by 2040. Lithium and nickel demand for electric vehicle batteries alone grows by 43 and 41 times, respectively.

This projected growth can be seen in the charts below.

Low-carbon power generation also accounts for a considerable chunk of the future growth in mineral demand, with rare earth elements currently needed for permanent magnets in wind turbines and EV motors, for example.

As societies become increasingly electrified, the expansion of electricity networks will also require large quantities of copper and aluminium.

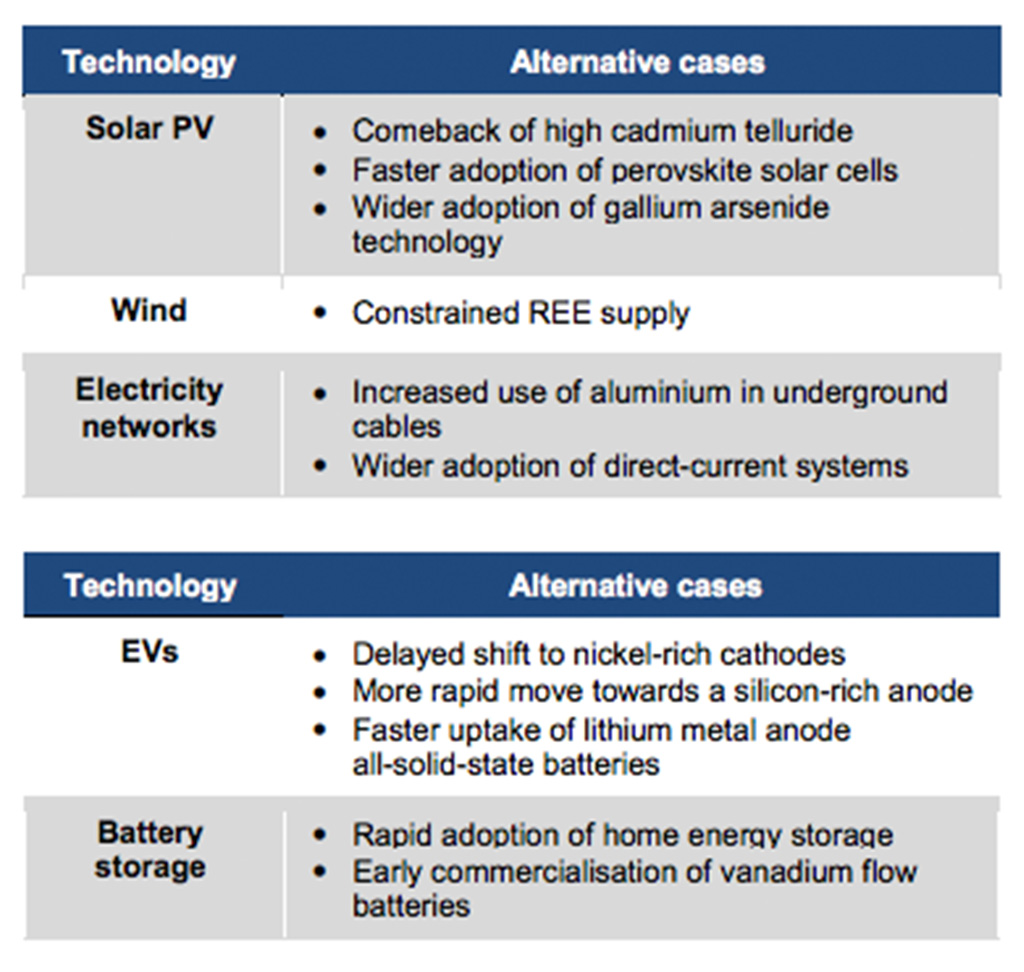

The IEA notes that future mineral demand is “subject to considerable uncertainty” due to both the extent of climate policies and the direction that different technologies take. For example, mineral requirements can shift in response to market prices or the commercial success of one technology over another.

To address this, the agency assessed 11 alternative cases that account for some of the potential variability in different sectors. These can be seen in the table below.

As an example, cobalt demand could be between six and 30 times higher than current levels, depending on future developments in both battery chemistry and climate policies. (Tesla and General Motors are among the firms exploring low- or no-cobalt car batteries.)

The report concludes that the largest uncertainty for future mineral demand relates to the ambition of global climate policies:

“The big question for suppliers is whether the world is really heading for a scenario consistent with the Paris Agreement. Policymakers have a crucial role in narrowing this uncertainty by making clear their ambitions and turning targets into actions. This will be vital to reduce investment risks and ensure adequate flow of capital to new projects.”

‘Looming mismatch’

In a statement released to accompany the report, Birol says:

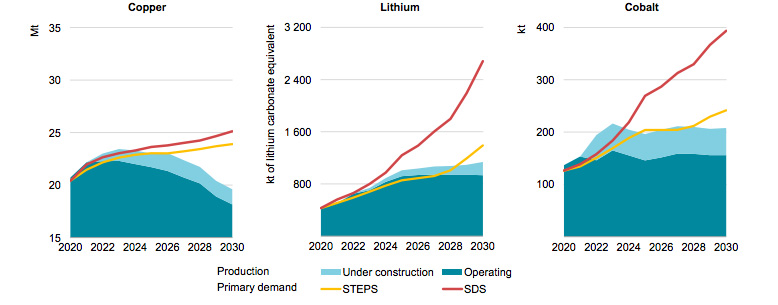

“The data shows a looming mismatch between the world’s strengthened climate ambitions and the availability of critical minerals that are essential to realising those ambitions.”

This can be seen in the charts below, which show projected demand in the SDS (red line) and even the STEPS (yellow line) outstripping the mineral resources that are currently due to be extracted (blue area) in the coming decades.

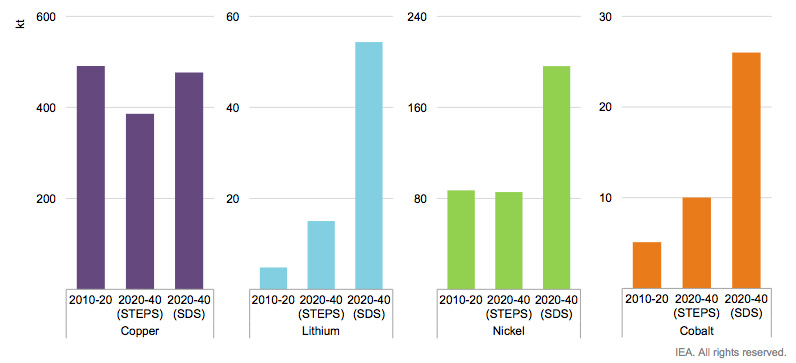

For the SDS in particular, the scale of demand growth for most of these minerals is far above the levels that have been seen in recent years, as the chart below shows.

For example, between now and 2040 annual average demand growth for lithium is around nine times higher than the levels seen over the past decade. Meanwhile, demand for copper must continue to be met at the same, relatively high, level.

The IEA identifies several “risk factors” which it says may “increase the possibility of market tightness and new price cycles, slowing energy transitions”.

These include the long time spans typically involved in starting up new mining projects, a trend towards declining resource quality at many mines and growing scrutiny of environmental and social issues at these sites.

The report also notes that many mines are located in areas of high climate risk. Around half of global lithium and copper production is located in areas of high water stress, for example.

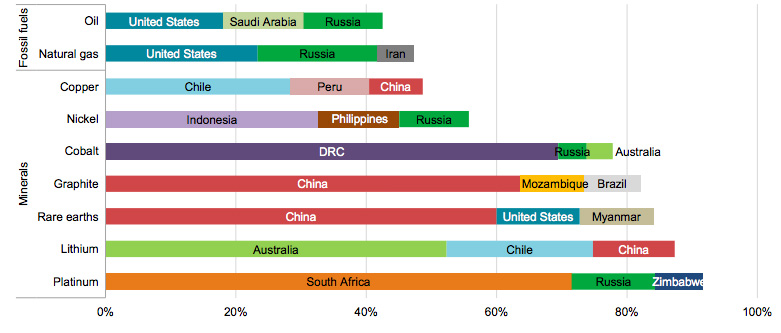

The IEA states that another issue is the geographical concentration of many of these minerals, as shown in the chart below.

Frequently, a single country is responsible for roughly half of worldwide production, leaving the global market vulnerable to trade measures or events in those nations ranging from natural disasters to military coups.

IEA recommendations

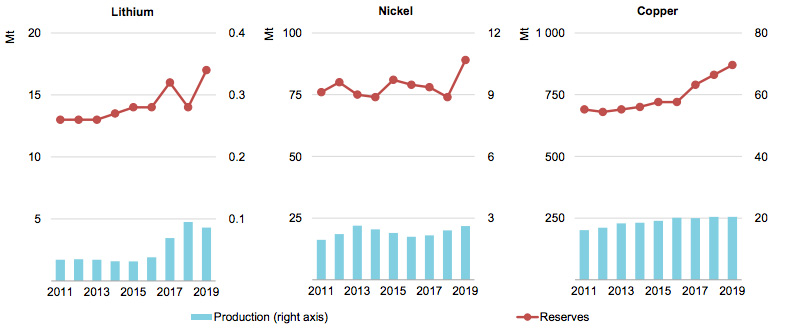

Despite these issues, the IEA emphasises that there “is no shortage of resources” – the quantity of key minerals held in deposits underground.

It adds that the size of economically viable reserves have been growing, despite rising production, as shown in the chart below.

The agency also provides “six key recommendations for a new, comprehensive approach to mineral security”.

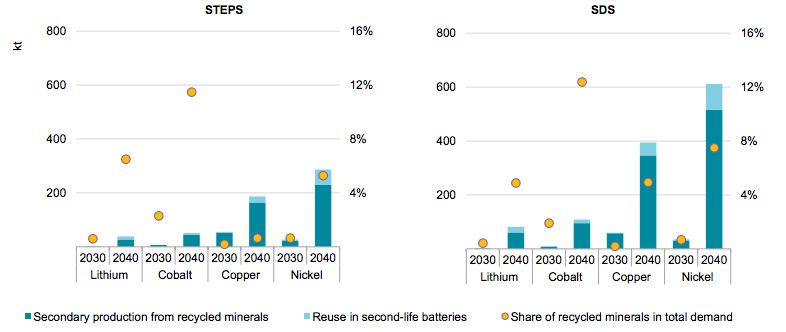

One of these recommendations is scaling up recycling to relieve pressure on new supplies, although as the chart below shows, recycled metals are still only expected to be a fraction of the total used by 2040.

Besides world governments being clear about their climate policies, the agency also notes the importance of promoting R&D, maintaining high environmental and social standards and strengthening international collaboration between producers and consumers.

Finally, the IEA emphasises that while mining activities produce greenhouse gases, “emissions along the mineral supply chain do not negate the clear climate advantages of clean energy technologies”.

-

IEA: Mineral supplies for electric cars ‘must increase 30-fold’ to meet climate goals

-

IEA: ‘Looming mismatch’ between climate targets and supply of important minerals