Q&A: New UK onshore wind and solar is ‘50% cheaper’ than new gas

Molly Lempriere

02.11.26Molly Lempriere

11.02.2026 | 1:55pmThe UK government has secured a record 7.4 gigawatts (GW) of solar, onshore wind and tidal power in its latest auction for new renewable capacity.

It is the second and final part of the seventh auction round for “contracts for difference” (CfDs), known as AR7a.

In the first part, held in January 2026, the government agreed contracts for a record 8.4GW of new offshore wind capacity.

This makes AR7 the UK’s single-largest auction round overall, with its 14.7GW of new renewable capacity being 50% larger than the previous record set by AR6 in 2024.

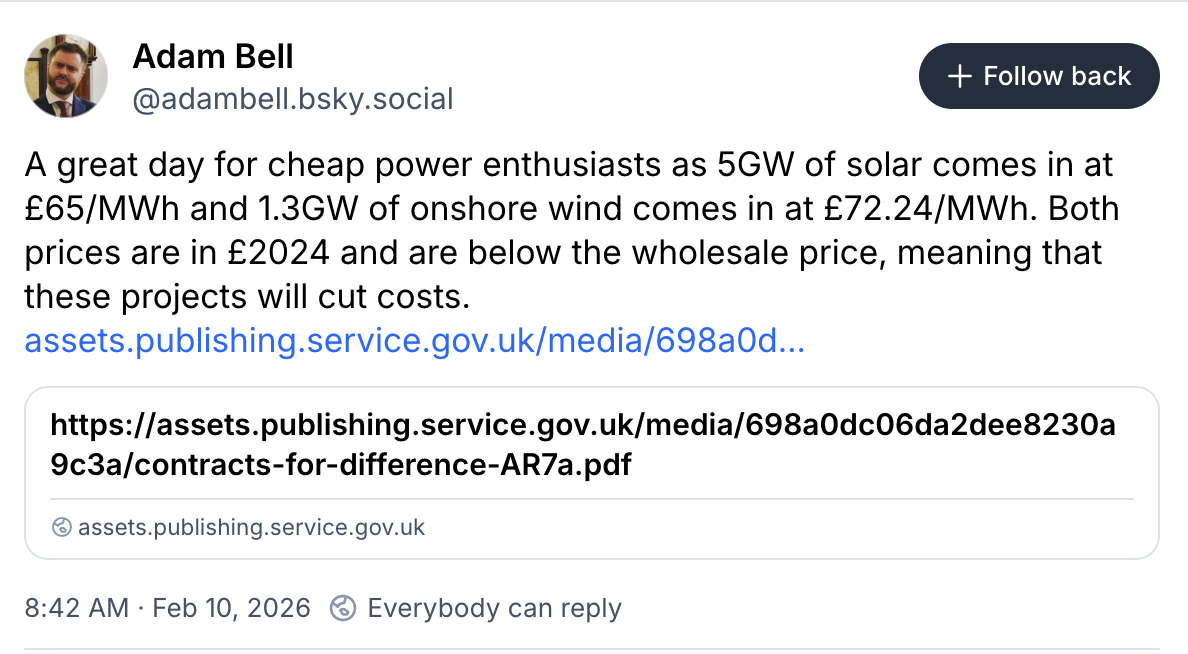

In AR7a, 157 solar projects secured contracts to supply electricity for £65 per megawatt hour (MWh) and 28 onshore wind projects were contracted at £72/MWh.

This means they will help cut consumer bills, according to multiple analysts.

Energy secretary Ed Miliband welcomed the outcome of the auction, saying in a statement that the new projects would be “50% cheaper” than new gas:

“These results show once again that clean British power is the right choice for our country, agreeing a price for new onshore wind and solar that is over 50% cheaper than the cost of building and operating new gas”.

In addition to cutting costs, the new projects will help reduce gas imports.

In total, AR7 will cut UK gas demand by around 95 terawatt hours (TWh) per year, enough to cut liquified natural gas (LNG) imports by three-quarters, according to Carbon Brief analysis.

Below, Carbon Brief looks at the seventh auction results for onshore wind, solar and tidal, what they mean energy for bills and the impact of the UK’s target of “clean power by 2030”.

- What happened in the latest UK renewable auction?

- What does the solar and onshore wind auction mean for bills?

- What does it mean for energy security, jobs and investment?

- What does the auction mean for clean power by 2030?

What happened in the latest UK renewable auction?

The latest UK government auction for new renewable capacity is the second and final part of the seventh auction round, known as AR7a.

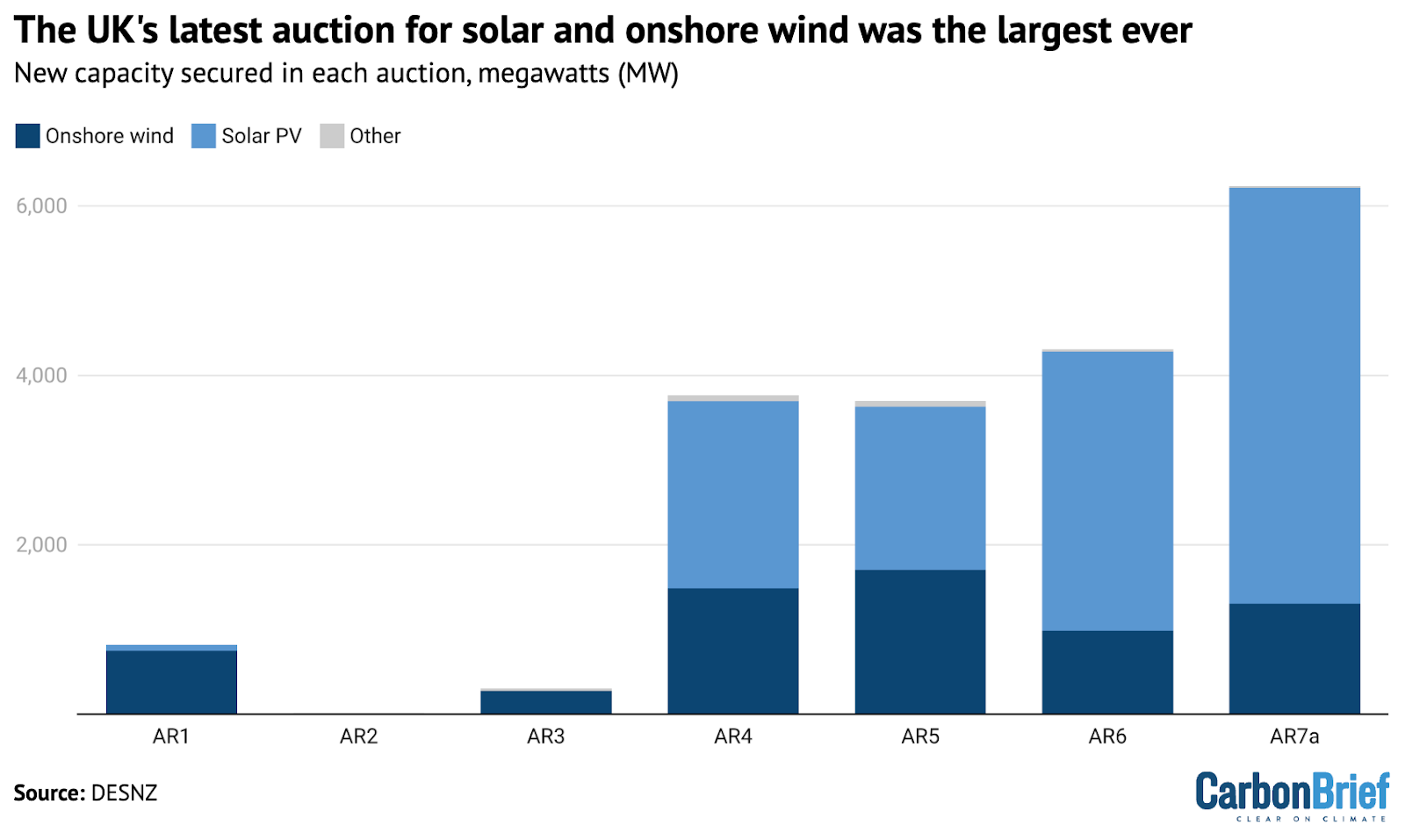

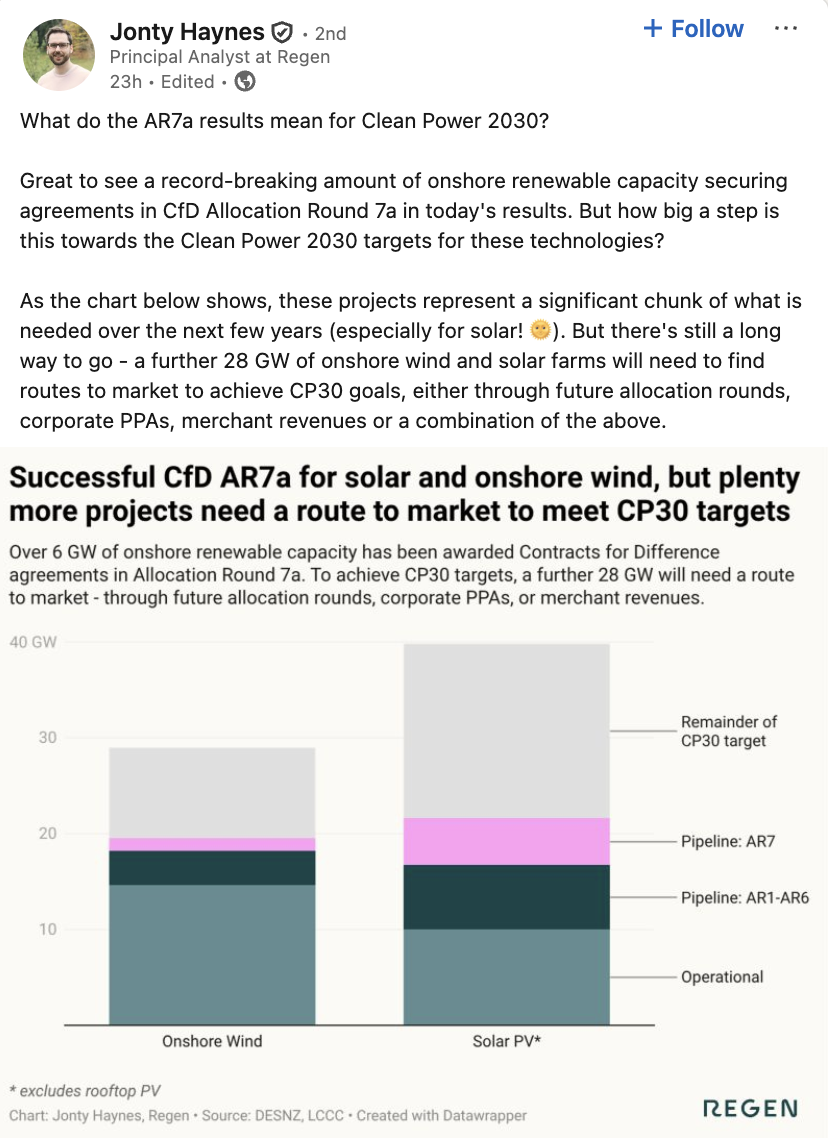

It secured a record 4.9GW of new solar capacity across 157 projects, as shown in the figure below, as well as 1.3GW of onshore wind across 28 projects.

In addition, four tidal energy projects totalling 21 megawatts (MW) secured contracts, included within “other” in the figure below.

Most of the solar that secured a contract has a capacity of less than 50MW. This is the cut-off point for projects to be approved by the local council. Larger schemes must instead go through the “nationally significant infrastructure project” (NSIP) process, subject to approval by the secretary of state for energy.

For the first time, one 480MW solar project – approved via this NSIP process – won a CfD in AR7a. The West Burton Solar NSIP is being developed in Lincolnshire and Nottinghamshire by Island Green Power. It is named after the grid connection it will use, freed up by the shuttering of the coal-powered West Burton plant.

However, Nick Civetta, project leader at Aurora Energy Research notes on LinkedIn that this site was only one of four eligible solar NSIPs to secure a contract.

Civetta adds that “wrangling these large projects into fruition is proving more painful than expected”.

Solar projects secured a “strike price” of £65/MWh in 2024 prices, some 7% cheaper than the £70/MWh agreed in the previous auction round.

In previous auction rounds CfD contracts were expressed in 2012 prices. For comparison, AR6 and AR7a solar contracts stand at £50/MWh and £47/MWh in 2012 prices, respectively.)

Alongside solar, 28 onshore wind projects secured contracts in the latest CfD auction, with a total capacity of 1.3GW.

This includes the Imerys windfarm in Cornwall, which at nearly 20MW is the largest onshore wind farm in England to secure a contract in a decade.

(Shortly after taking office in 2024, the current Labour government lifted a decade-long de facto ban on onshore wind in England.)

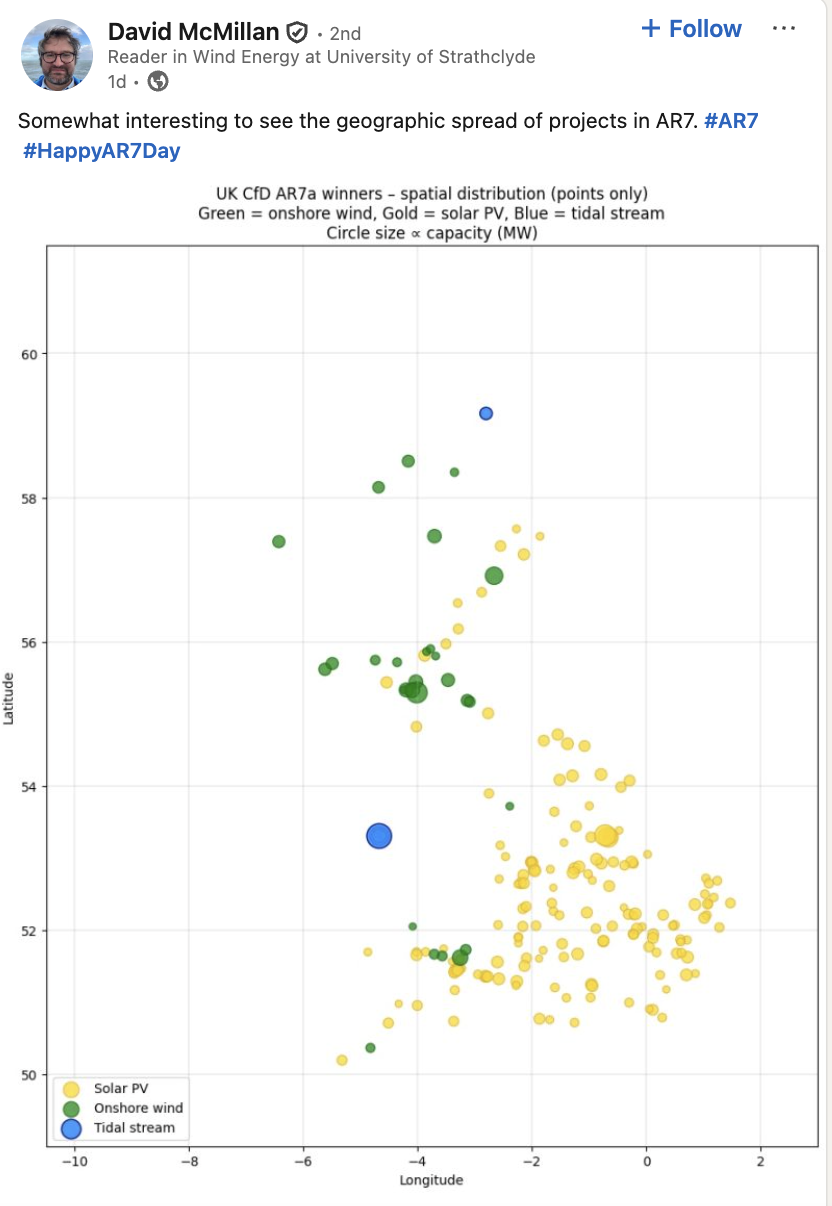

Overall, Scotland still dominated the auction for onshore wind, with 1,093MW of projects in the country in comparison to 38MW in England and 185MW in Wales.

This includes the Sanquhar II windfarm in Dumfries and Galloway in Scotland, which will become the fourth-largest onshore wind farm in the UK at 269MW.

In total, Wales secured contracts for 20 renewables projects in AR7a, with a capacity of more than 530MW. This is the largest ever number of Welsh projects to get backing in a CfD auction, according to a statement from the Welsh government.

Onshore wind secured a strike price of £72/MWh, up slightly from £71/MWh in the previous auction in 2024.

The prices for solar and onshore wind were 13% and 21% below the price cap set by Department of Energy Security and Net Zero (DESNZ) for the auction, respectively.

In its press release announcing the results, the government noted that the results for solar and onshore wind were less than half of the £147/MWh cost of building and operating new gas power stations.

Finally, four tidal energy projects secured contracts with a total capacity of 21MW at a strike price of £265/MWh, up from £240/MWh in 2024.

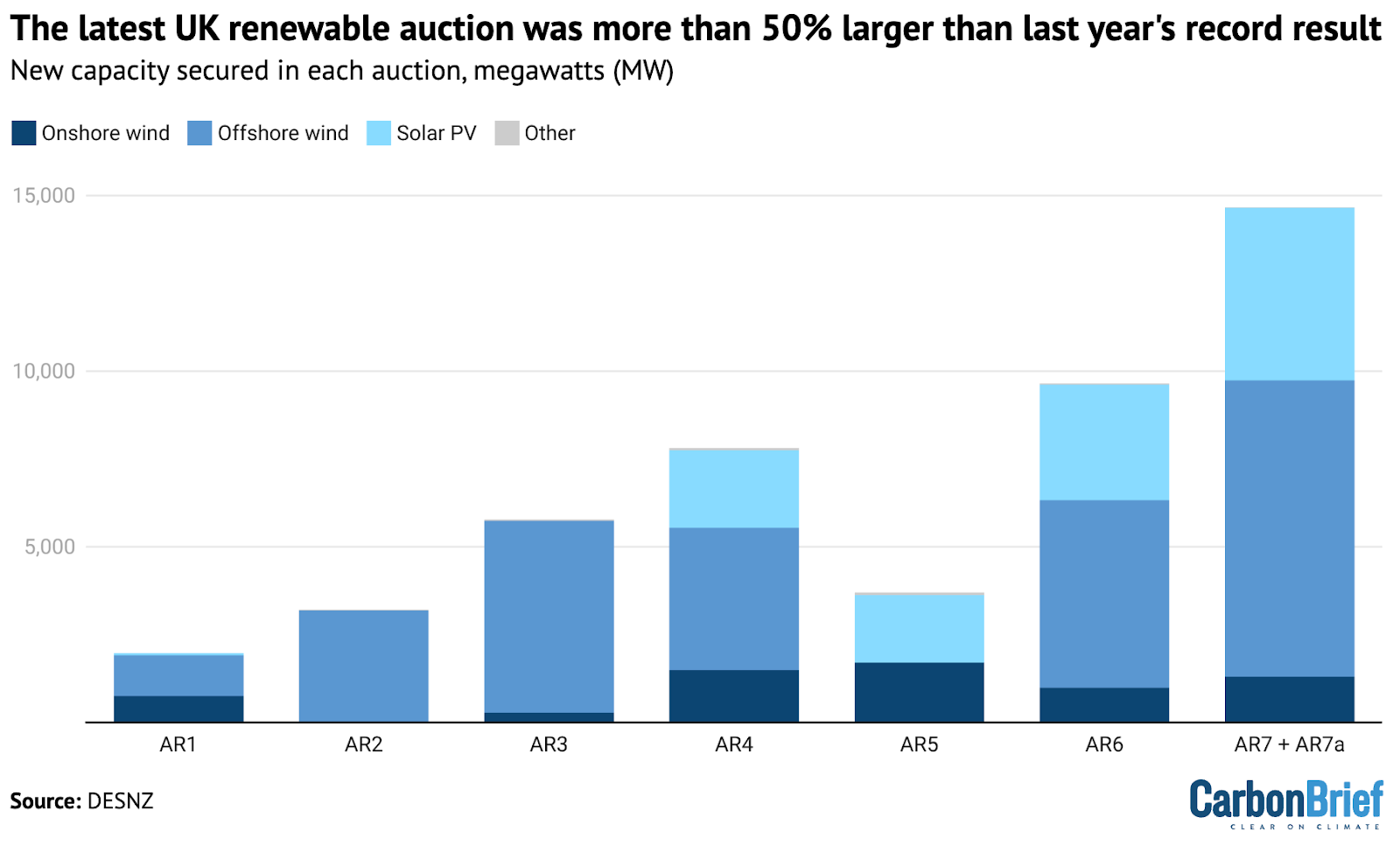

In total, taken together with the 8.4GW of offshore wind secured in the first part of the auction, AR7 secured a total of 14.7GW of new clean power, as shown in the chart below.

This is enough to power the equivalent of 16 million homes, according to the government. It also makes AR7 the single-largest auction round by far, at more than 50% larger than the previous record set by AR6 in 2024.

This means that the two auction rounds held since the Labour government took office in July 2024 – AR6 and AR7 – have secured a total of 24GW of new renewable capacity. This is more than the 22GW from all previous auction rounds put together.

However, several analysts noted that the AR7a results did not include any old onshore windfarms looking to replace their ageing turbines with new equipment – so-called “repowering projects” – despite the auction being open to them for the first time.

What does the solar and onshore wind auction mean for bills?

Onshore wind and solar are widely recognised as the cheapest sources of new electricity generation in almost every part of the world.

The latest auction shows that the UK is no exception, despite its northerly location.

The prices for onshore wind and solar in the latest auction, at £72/MWh and £65/MWh respectively, are comfortably below recent wholesale power prices, which averaged £81/MWh in 2025 and £92/MWh in January 2026.

This means that the new projects will cut costs for UK electricity consumers, according to multiple analysts commenting on the auction outcome.

The government lauded the results of AR7a for securing “homegrown energy at good value for billpayers – once again proving that clean power is the right choice for energy security and to meet rising electricity demand”.

In a statement, Miliband added:

“By backing solar and onshore wind at scale, we’re driving bills down for good and protecting families, businesses, and our country from the fossil fuel rollercoaster controlled by petrostates and dictators. This is how we take back control of our energy and deliver a new era of energy abundance and independence.”

As noted in Carbon Brief’s coverage of the offshore wind results under AR7 in January, electricity demand is starting to rise as the economy electrifies and many of the UK’s existing power plants are nearing the end of their lives.

Therefore, new sources of electricity generation will be needed, whether from renewables, gas-fired power stations or from other sources.

In his statement, quoted above, Miliband said that the prices for onshore wind and solar were less than half the £147/MWh cost of electricity from new gas-fired power stations.

(This is based on recently published government estimates and assumes that gas plants would only be operating during 30% of hours each year, in line with the current UK fleet.)

Trade association RenewableUK also pointed to the cost of new gas, as well as the £124/MWh cost of the Hinkley C new nuclear plant, in its response to the auction results.

In a statement, Dr Doug Parr, policy director for Greenpeace UK, said:

“These new onshore wind and solar projects will supply energy at less than half the cost of new gas plants. Together with the new offshore wind contracts agreed last month, these cheaper renewables will lower energy bills as they come online.”

Strike prices for solar dropped by 6% compared to last year and while onshore wind prices rose, this was by less than 2% despite a “difficult environment for wind generation”, according to Bertalan Gyenes, consultant at LCP Delta.

In a post on LinkedIn, he noted that “extending the contract length [for onshore wind projects] by five years seems to have helped keep this increase low”.

The January offshore wind round secured 8.4 GW at £91/MWh, as such, the onshore and solar projects are 25% cheaper per unit of generation.

(The offshore wind projects secured in January are nevertheless expected to cut consumer bills relative to the alternative, or at worst to be cost neutral.)

Parr added that while the AR7a auction results “show we’re getting up to speed” ahead of the clean power 2030 target (see below), “an even faster way for the government to make a really big dent in bills would be to change the system that allows gas to set the overall energy price in this country”. He adds:

“That would allow us to unshackle our bills from unreliable petrostates and get off the rollercoaster of volatile gas markets once and for all.”

What does it mean for energy security, jobs and investment?

The onshore wind and solar projects secured in the latest auction round will generate an estimated 9 terawatt hours (TWh) of electricity, according to Carbon Brief analysis.

This is equivalent to roughly 3% of current UK electricity demand.

Combined with the estimated 37TWh from offshore wind secured during the first part of the auction, AR7 projects will be able to generate 46TWh of electricity, 14% of current demand.

If this electricity were to be generated by gas-fired power plants, then it would require around 95TWh of fuel, because much of the energy in the gas is lost during combustion.

This is several times more than the 25TWh of extra gas that could be produced in 2030 if new drilling licenses are issued, according to thinktank the Energy and Climate Intelligence Unit (ECIU). As such, AR7 will significantly cut UK gas imports, ECIU says, reducing exposure to volatile international gas markets.

Furthermore, ECIU says that the impact of renewables in driving down gas demand – and subsequently electricity prices – is already being seen in the UK.

Five years ago, gas was setting the wholesale price of power in the UK 98% of the time due to the way the electricity market operates.

This price-setting dominance is being eroded by renewables, with recent analysis from the UK Energy Research Centre showing that gas set power prices 90% of the time in 2025.

A further effect of new renewables is that they push the most expensive gas-fired power plants out of the system, reducing prices. This is known as the “merit-order effect”.

Recent analysis from ECIU found that large windfarms cut wholesale electricity prices by a third in 2025.

Lucy Dolton, renewable generation lead at Cornwall Insight, said in a statement that the AR7a results will provide a “surge in momentum as [the UK] pushes toward secure, homegrown energy”, adding:

“These investments ultimately strengthen the UK’s position against volatile gas markets. If the past few years have shown us anything, it’s that remaining tied to international energy markets comes with consequences.”

The projects that secured CfDs will help the UK avoid burning significant quantities of gas, “the bulk of which would have been imported at a cost which the UK cannot control”, said RenewableUK in its statement.

Together with previous CfD auction rounds, the latest new renewable projects are expected to generate some 153TWh of electricity once they are all operating, according to Carbon Brief analysis. This is around half of current UK demand.

Generating the same electricity from gas would require some 311TWh of fuel, which is similar to the 339TWh of gas produced by the UK’s North Sea operations in the most recent 12-month period for which data is available. This figure can also be compared with the 130TWh of gas that was imported by ship as liquified natural gas (LNG) in the same period.

The government added that the AR7a projects will support up to 10,000 jobs and bring £5bn in private investment to the UK.

(In total, the new projects secured via AR7 are expected to bring investments worth around £20-23bn to the UK, according to Aurora.)

Additionally, the onshore wind projects are expected to generate over £6.5m in “community benefit” funds for people living near them, according to RenewableUK.

The AR7a results were released alongside the publication of the Local Power Plan by the government and Great British Energy.

This is designed to provide £1bn in funding for communities to own and control their own clean energy projects across the UK.

What does the auction mean for clean power by 2030?

The AR7a results put the UK “on track for its 2030 clean power target”, according to the government.

Over AR6 and AR7, several changes have been made to the CfD process to help facilitate more projects to secure contracts.

A total of 24GW has been secured over the last two auction rounds – which have taken place under the current Labour government – compared to 22GW across the five auction rounds previously.

As part of its goal for clean power to meet 100% of electricity demand by 2030 and to account for at least 95% of electricity generation, the UK government is aiming for 27-29GW of onshore wind and 45-47GW of solar by the end of the decade.

As of September 2025, the UK had 16.3GW of installed onshore wind capacity and more than 21GW of solar capacity. Taken together, the onshore technologies therefore need to double in operational capacity over the next four years to reach the 2030 targets.

Analysis by RenewableUK suggests that the government will need to procure between 3.85GW to 4.85GW of onshore wind in the next two auctions for the 2030 goal to remain possible.

Writing on LinkedIn, Aurora’s Civetta said that the onshore clean power 2030 targets “remain a long way off”.

He continued that the gap for solar to reach its 45-47GW target is still a “whopping 18GW”, but added that there may be other ways for new capacity to be secured, beyond the CfD auctions.

He said these included a growing market for corporate “power purchase agreements” (PPAs), economic incentives for homes and businesses to install solar and the government’s recently released “warm homes plan”, all of which “should drive further procurement”.

Dolton from Cornwall Insight adds that “the challenge now is delivery”, continuing:

“2.5GW of the winners have a delivery year of 2027/28, and over half – 3.7GW – have a delivery year of 2028/29, which brings them very close to the government’s 2030 clean power target.

“Historically, renewable projects in the UK have faced delays, often due to grid connection backlogs and planning holdups. With AR7 and some of AR8 representing the only realistic pipeline for pre-2030 capacity, keeping to schedule will be essential.”

When built, the projects announced today will help to bring the total capacity of CfD-supported wind and solar to 50.6GW, according to Ember.

While solar and onshore wind are expected to play an important role in decarbonising the electricity system, offshore wind is set to be the “backbone”.

The government is targeting 43-50GW of offshore wind by 2030, up from around 17GW of installed capacity today.

This leaves a gap of 27-34GW to the government’s target range.

Prior to the AR7 auction, a further 10GW had already secured CfD contracts, excluding the cancelled Hornsea 4 project.

The 8.4GW secured in January brings the gap to reach the minimum of 43GW over the four years to just 7GW.