Q&A: Will the reformed EU Emissions Trading System raise carbon prices?

Simon Evans

12.06.17Simon Evans

06.12.2017 | 4:52pmIn July 2003, at a series of meetings in Brussels and Strasbourg, EU lawmakers adopted an Emissions Trading System (EU ETS) to help combat climate change.

The cap-and-trade scheme for industrial CO2 was part of the EU’s response to the Kyoto Protocol, which had set the then-15 member bloc a target to cut emissions 8% below 1990 levels by 2012.

Even before its adoption, the EU ETS was subject to years of fraught debate, lobbying and negotiation. After it started operating in 2005, it quickly ran into trouble, facing volatile carbon prices that crashed in the wake of the financial crisis, while industry pocketed windfall profits.

Prices have remained stubbornly low ever since, undermining the supposed role of the ETS as the cornerstone of EU climate policy.

However, last month, after two years of talks, “strengthening reforms” were finally agreed between the EU’s 28 member state governments, the European Commission and MEPs in the European Parliament.

In this Q&A, Carbon Brief runs through the details of the reforms and whether they will raise EU carbon prices. The Brexit question is also covered.

Why did the EU adopt a carbon market?

For the climate policy purists, “putting a price on carbon” represents the most economically efficient means to reduce emissions, at the lowest cost. In a cap-and-trade scheme, industries covered by the market buy and sell allowances to emit greenhouse gases, within a cap that shrinks over time.

This idea is reflected in the text of the 2003 directive, establishing the EU ETS so as to “promote reductions of greenhouse gas emissions in a cost-effective and economically efficient manner”. In more extreme versions of this view, no other policies should be needed, as the shrinking cap is all that is needed to meet carbon targets (more on this, below).

The directive had been adopted after failed attempts to introduce a carbon energy tax, first proposed in 1992. It also marked a change of heart. The EU had opposed use of carbon markets under the Kyoto Protocol because of concerns over “hot air” – the idea that emissions caps might credit reductions that had already happened. (See this detailed history for more.)

Announcing the adoption of the EU ETS on 23 July 2003, the environment commissioner Margot Wallström said in a statement: “Today’s proposal and the emissions trading system just adopted by the Council and the European Parliament are evidence of our strong commitment to cutting greenhouse gas emissions and to the Kyoto Protocol.”

In the “recital” (introduction) to the latest reforms, the ETS is described as the “cornerstone of the Union’s climate policy”. The ETS cap is now set to shrink to 43% below 2005 levels in 2030, as part of the overall EU 2030 target to cut emissions “at least 40%” below 1990 levels.

What does the EU ETS cover?

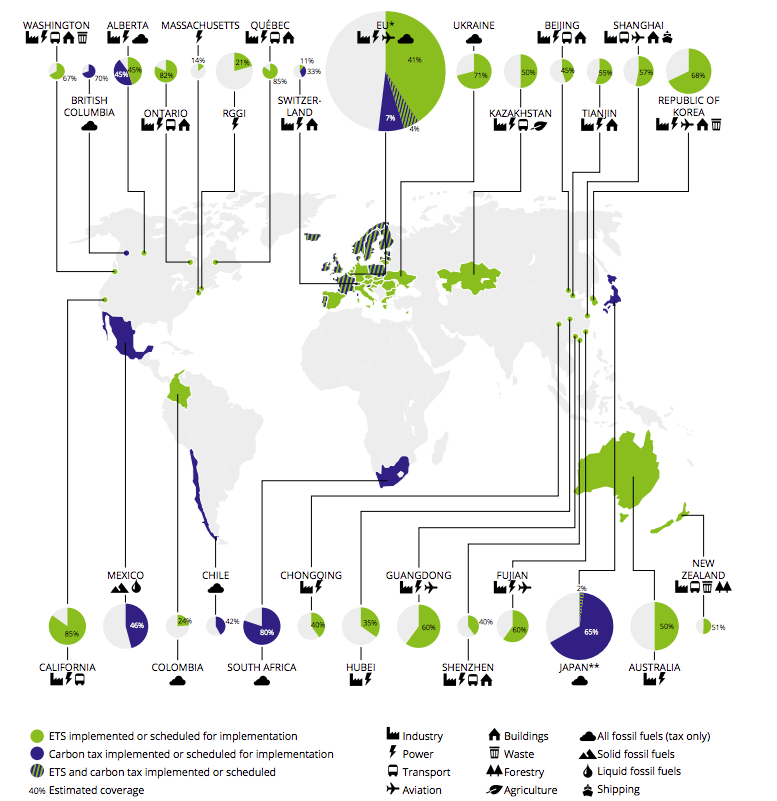

The EU ETS is the world’s largest carbon market (see graphic, below), at least until China launches its national market, due for launch this year, but subject to delays and uncertainty.

Carbon pricing schemes around the world, including their nature (ETS or carbon tax), sectoral coverage and share of national or regional emissions. Source: State and Trends of Carbon Pricing 2017, World Bank

The EU ETS covers airlines and more than 11,000 industrial sites, responsible for around 45% of EU greenhouse gas emissions – currently around 2bn tonnes of CO2 equivalent. This includes CO2 from industry, the power sector and aviation, plus nitrous oxide and perfluorocarbons from industry. (This handy European Commission primer has more background.)

![]()

Only flights between EU member states are covered, with flights outside the bloc still exempted, pending a review of the international aviation emissions trading scheme known as CORSIA.

Norway, Iceland and Liechtenstein also participate in the EU ETS. Meanwhile, the EU and Switzerland recently agreed to link their schemes – following seven years of talks – meaning emissions credits can be traded between the two.

Who pays for EU ETS allowances?

Also embedded in the initial 2003 ETS directive is the “polluter pays principle” and, as such, industry should pay for its carbon emissions. In the initial phases, however, most emissions credits were handed out for free, first to familiarise participants with the system and create a functioning market, then later to protect industry from overseas competition not facing a carbon price.

The recital (introduction) to the reform text explains:

“[The 2003 ETS directive] provides for a transition to full auctioning over time. Avoiding carbon leakage is a justification to temporarily postpone full auctioning, and targeted free allocation of allowances to industry is justified in order to address genuine risks of increases in greenhouse gas emissions in third countries where industry is not subject to comparable carbon constraints as long as comparable climate policy measures are not undertaken by other major economies.”

In the first phase, from 2005 to 2007, virtually 100% of carbon credits entering the market were given out for free, falling to an average of 96% during phase 2, from 2008 to 2012, according to an analysis of market data by carbon market NGO Sandbag, carried out for Carbon Brief, shown in the chart, below.

During phase 3, which runs until 2020, the free share fell dramatically because power stations stopped receiving allowances for free. Sandbag’s analysis suggests an average of 53% of the allowances entering the market during phase 3 will be free.

Share of emissions allowances entering the market each year that are allocated for free, under the first four phases of the EU ETS from 2005-2030 and excluding aviation. Source: Sandbag analysis for Carbon Brief, based on past market data and a model of the outcome of reforms. This assumes the market stability reserve (MSR) will prevent some allowances entering the market, shrinking the auction pot, while poorer member states will make full use of a derogation from auctioning, allowing them to give their power sectors free allowances. See below for more explanation of these details. Chart by Carbon Brief using Highcharts.Phase 4 runs from 2021 to 2030 and was the subject of the latest reforms, which will have an uncertain impact on the share of carbon credits handed out for free. Sandbag’s analysis suggests that 60% of allowances entering the market could be given for free, an increase on phase 3.

This assumes three elements of the reforms kick in. First, if too many free allowances are claimed, then up to 3% of the cap can be shifted from the auction share to the free allocation share, see below. Second, poorer member states can hand their power sectors some free allowances.

Third, some allowances are likely to be removed from the market because of the market stability reserve (MSR, see below). These removals come out of the auction share, which effectively raises the share of allowances entering the market that are given out for free, even as it tightens the market overall.

Note that this analysis excludes aviation emissions. Some 15% of CO2 emissions from flights between EU nations are supposed to be subject to auction during phase 3. This share is to be maintained through phase 4.

What is the EU carbon price?

The EU ETS has also been plagued by persistently low carbon prices – for those that do have to pay for their pollution. Emissions allowances (EUAs) have cost less than €10 per tonne since late 2011, far below most estimates of the social cost of carbon and below the level thought to be necessary to drive deep decarbonisation.

Daily EU ETS carbon prices. Source: ICE EUA futures via Sandbag and Quandl. Chart by Sandbag using Highcharts.Prices fell after the financial crisis because free allocation continued at levels based on pre-crisis economic activity, whereas industrial output contracted. Meanwhile, the spread of more efficient appliances and renewable sources of electricity cut demand for permits. This left a flooded market.

Opinion is divided on whether the latest reforms will resolve these problems and raise prices (see below).

How is the EU ETS being reformed?

The reforms agreed in November were meant to codify the rules of market operation during phase 4 of the ETS from 2021 to 2030. They ended up also aiming to correct persistently low prices, while continuing to shield industry from overseas competitors facing no carbon price and keeping eastern European states on board.

Specifically, the reforms bring the EU ETS into alignment with the EU’s overall 2030 climate target, of at least a 40% cut below 1990 levels. They update the rules on free allocation of allowances. They attempt to squeeze the market surplus, raising prices. And they extend and expand the support for energy system upgrades in eastern European countries, which has been the quid pro quo for their support of the ETS.

This uneasy balancing act saw a series of stand-offs – most prominently over support for coal power – inevitably settled by compromise. This, along with the uncertain effects of economic growth, technological change and other national and EU climate policy, means that carbon price increases – and the ETS’s role at the heart of EU climate policy – are far from assured. More on this later.

The EU’s topline 40%-by-2030 goal means the overall ETS cap must shrink more quickly, by 48MtCO2e each year, up from 38Mt/yr during phase 3. (This fixed annual reduction is confusingly described as a percentage “linear reduction factor” of 1.74% in phase 3 and 2.2% in phase 4. The percent refers to a proportion of the average annual cap during 2008-2012.)

What is the market stability reserve?

The other key element of the reforms is the market stability reserve (MSR), which will hold excess allowances outside the market starting from 2019. This is effectively a central bank for the carbon market, designed to stabilise supply and demand for credits, which will kick in from January 2019.

Hæge Fjellheim, head of carbon analysis for information providers Thomson Reuters Point Carbon, tells Carbon Brief:

“This reform has been going for two years. If you take it from that point in time, you would have been surprised that it was quite a strong outcome in terms of strengthening the EU ETS and the market balance, because the aim of the reform was not to tighten the balance…It’s tightening the screw on the oversupply issue, which has been the main problem of the ETS.”

The MSR was agreed in 2015, but has been strengthened in two ways. Lawmakers agreed to significantly tighten its parameters, so that it takes more credits out of circulation each year, while it will also now cancel credits if the surplus becomes large enough.

First, 24% of the market surplus will be removed each year between 2019 and 2023 and placed into the reserve, if the surplus exceeds 833m credits – enough to cover the annual emissions of the whole German economy. The reforms doubled this rate, compared to the 12% agreed in 2015, though the removal rate will revert to 12% from 2024. If the surplus falls below 400Mt, 100m credits will be released from the reserve into the market.

Second, if the number of credits in the reserve exceeds the volume auctioned in the previous year, then the excess will be automatically and permanently removed from the market. (Technically, they will be “invalidated” rather than “cancelled”; it is not clear what this distinction means, says Marcus Ferdinand, lead analyst for EU power and carbon markets at information provider ICIS Carbon Analytics.)

The automatic cancellation will remove an estimated 2.4GtCO2e of allowances from the market during phase 4, according to Thomson Reuters Point Carbon.

Can countries cancel carbon credits?

Another element of the reforms allows ETS member states to voluntarily cancel allowances from their auction share, in response to the closure of electricity generating capacity that will no longer bid into the market. Cancellations are limited to the emissions of the closing capacity.

Worker with steel forge. Credit: Cultura Creative (RF) / Alamy Stock Photo.

This could apply to UK coal-fired power stations, for example, which are closing as a result of the government’s phaseout pledge. (At the start of phase 3, the UK’s coal fleet was responsible for nearly 7% of EU ETS emissions, meaning their closure strongly affects the overall market.)

Countries could use voluntary cancellation to demonstrate greater climate ambition, says Rachel Solomon Williams, managing director of carbon market NGO Sandbag. Sweden is already voluntarily buying and cancelling ETS allowances, though only around 7MtCO2e per year.

If governments decide to voluntarily cancel carbon credits, however, they would have to forego the revenue from auctioning those allowances.

“I’m very sceptical this measure will be used on a largescale,” Ferdinand tells Carbon Brief. He adds: “I think there will always be a quarrel between the environment and finance ministries.”

Auction revenues amount to billions of euros each year across the EU, of which 80% is earmarked for climate and energy spending, research for the European Commission suggests. For example, the UK government earns around £0.5bn a year from ETS auctions – and the Office for Budget Responsibility assumes this will continue at least until the end of its forecast period in 2022/23.

(If the UK leaves the EU ETS on the March 2019 Brexit date, or after a transitional phase, then this revenue would cease. The UK’s future role in the ETS is undecided, see below.)

Nevertheless, combined with the strengthened MSR, this reform overturns the “waterbed effect”. This is the idea that climate action outside the ETS not only undermines the market, by weakening demand, but also achieves no extra emissions savings because the annual market cap is fixed. (Pushing down on one part of the “waterbed” of emissions only serves to raise them elsewhere.)

This charge has been levelled at the UK’s top-up carbon tax, the carbon price floor, for example.

Yet disagreement remains over the appropriate balance between relying on the ETS and implementing additional EU or national climate policies. (See below for more details.)

How are free allowances handed out?

During phase 4 of the EU ETS from 2021 to 2030, industries will continue to get “transitional” support in the form of free emissions permits, if they are deemed at risk of competition from overseas firms that do not pay an equivalent carbon price.

![]()

Industry sectors at risk of this carbon leakage will – in principle – continue to get 100% of their allowances for free. Even sectors not at risk of carbon leakage will still get 30% free allowances until 2026, falling to 0% by 2030. Their free allocation had been due to stop in 2026.

A new consultation on revising the list of sectors deemed at risk runs until 2 February 2018. Phase 4 will continue using a binary at-risk/not-at-risk approach, with those at risk getting 100% free allowances, rather than a graduated approach advocated by NGO Sandbag.

In order to reduce windfall profits from excess free allowances when production falls – as happened in the wake of the financial crisis – free allocations will be adjusted up or down if an installation’s output over two years changes by more than a 10% threshold.

The power sector is not given free allowances, though phase 4 extends a partial exception to this for the 10 poorest EU member states in eastern Europe, including the likes of Poland, Romania and Hungary (see below). For the rest of industry, according to Thomson Reuters Point Carbon, the “lion’s share will continue to be considered at high risk of carbon leakage and receive 100% of their benchmark [emissions] as free allocation”.

During phase 4, the “benchmark” rate at which each industry can claim free allowances will shrink by between 0.2% and 1.6% per year, to reflect progress in improving efficiency. This benchmark rate is based on the most carbon-efficient 10% of sites within each sector.

Claims for benchmarked free allowances are added up across industries and countries, then checked against that year’s overall cap and the volume set aside for auctions, which is supposed to average 57% across phase 4. If too many free allowances are claimed, then allocations are reduced uniformly, across the board, using a “cross sectoral correction factor” (CSCF).

During phase 3, this has meant all industries, including those most at risk of carbon leakage, receiving less than 100% of their allowances for free, undermining efforts to shield them from the impact of climate policy.

Under the phase 4 reforms, up to 3 percentage points of the auction volume can be transferred into extra free allowances, in order to avoid triggering the CSCF.

This would raise the share of free allowances handed out from 43% to 46%, meaning around half a billion fewer credits available for auction, according to NGO Sandbag. This would translate into more than €3.5bn in lost auction revenues for member states, even at current low ETS prices.

How does the EU ETS support eastern Europe and innovation?

Several EU ETS support schemes will continue through phase 4. These schemes, designed to support innovation across Europe and energy sector modernisation in poorer states, come with rules attached – though the strictness of the rules is unclear. These funds were also used to leverage political support, both for ETS reforms and the wider EU 2030 climate and energy targets.

Fiat Panda and Fiat 500 production line in factory, Tychy, Poland. Credit: Bart Pro/Alamy Stock Photo.

The innovation fund, managed at EU level and funded via 400m allowances, will continue to be used to finance research and development of: “CCS or CCU [carbon capture and storage or usage] facilities, new renewable energy technologies and industrial innovation”.

For eastern Europe, two ETS schemes are supposed to assist energy system upgrades, under articles 10c and 10d of the directive.

When the power sector stopped receiving free allowances in 2013, poorer EU countries were allowed to continue handing out credits, covering up to 70% of emissions in 2013, declining to zero in 2020. This “article 10c” derogation was conditional on the 10 countries – Bulgaria, Cyprus, Czech Republic, Estonia, Hungary, Lithuania, Poland and Romania – investing the equivalent amount in “the modernisation of electricity generation”.

These countries must submit national plans explaining what the money was going towards. Specifically, the plans should address: “Investments in retrofitting and upgrading of the infrastructure and clean technologies. The national plan shall also provide for the diversification of their energy mix and sources of supply.”

The European Commission approved allocation of up to 680m free allowances under 10c by 2019, with a market value estimated at €12bn, according to NGO Carbon Market Watch. It says that in practice, 90% of the money was invested in existing fossil fuel infrastructure, mostly coal.

Can EU ETS funds still be used to support coal?

The article 10c derogation was extended and expanded under the phase 4 reforms, allowing those 10 eastern European countries to allocate up to 60% of power sector emissions allowances for free, with their value matched by investment as before.

This 60% figure is an increase from the 40% agreed by member state governments in 2014. While the revised legal text includes a series of new conditions, these leave considerable wiggle room. (The European Parliament had called for a 450gCO2 per kilowatt hour threshold for support, effectively an outright ban on support for coal power.)

The text says: “The investments supported shall be consistent with the transition to a safe and sustainable low-carbon economy, the objectives of the Union’s 2030 climate and energy policy framework, and reaching the long term objectives as expressed in the Paris Agreement. This derogation shall end on 31 December 2030.”

Investments financed through article 10c – and worth more than €12.5m – must be subject to competitive bidding. Additionally, they must: “contribute to the diversification of their energy mix and sources of supply, the necessary restructuring, environmental upgrading and retrofitting of the infrastructure, or modernisation of the energy production.”

Further loosely worded conditions say projects must “not contribute to or improve the financial viability of highly emission-intensive electricity generation nor increase dependency on emission-intensive fossil fuels”.

Funding must also “realise a predetermined significant level of CO2 reductions”. Where new power capacity is added, this must be matched by the closure of “a corresponding amount of more emission-intensive…capacity”.

The second EU ETS scheme for eastern Europe is the article 10d “modernisation fund”, offered in 2014 in return for Polish support of the EU 2030 climate goals. This is administered at EU level and financed with 2% of total allowances for the period 2021-2030 (310Mt), with an optional extra 0.5%.

The revised text says: “No support from this fund shall be provided to energy generation facilities using solid fossil fuels,” ruling out EU money for coal. The text adds that 70% shall go towards renewables, energy efficiency, grid infrastructure or support for “just transition” in mining regions.

The net impact of the reforms to these two support schemes for eastern Europe is uncertain. This will be a balance between the raising of the 10c derogation to 60% free allocation, its new but loosely-worded funding criteria and the ban on support for coal under the 10d modernisation fund.

Fjellheim tells Carbon Brief:

“We want to look into this a bit more, because what does it really mean? It looks like a big win for those that didn’t want to fund coal, but with the raised ceiling to 60%, it is not really clear…It looks strict but it might not be that strict in the end.”

Will the latest reforms raise carbon prices?

Most analysts expect the reforms to tighten the market surplus and raise carbon prices in the short term, from today’s roughly €7/tCO2e to around €10 through 2018, reports newswire Carbon Pulse.

In terms of future carbon prices, the strengthened MSR is the most important aspect of the reforms, says Ferdinand. He tells Carbon Brief: “Honestly, I’m quite bullish. The main driver is the MSR doubling [of the annual intake rate, from 12 to 24% of the market surplus].”

Ferdinand thinks the MSR will cut the volume of allowances available for auction roughly in half from 2019, a cut of around 400MtCO2e. He also expects rising prices to change participants’ strategic approach to hedging, encouraging them to hold on to unused credits and squeezing the surplus available to the market.

He says: “If you are an industrial sitting on surplus allowances when the price is rising, we don’t believe all of those will come to market.”

All this means prices could rise to €9-10/tCO2e in 2018 and €36 in 2024, Ferdinand says, before easing off towards €23 in 2030, as the MSR intake rate drops back to 12% per year and after higher prices have driven faster-than-expected cuts in emissions.

At the lower end of the forecast spectrum is Thomson Reuters Point Carbon, which sees prices rising to €10 in 2020 and €23 in 2023. Fjellheim explains: “We think the MSR will tighten the market considerably, but we assume market participants to be forward looking…so that means they price in future shortages already today.” This means prices will only rise gradually.

Fjellheim tells Carbon Brief:

“We have lower prices than many other analysts…There is more risk to the down side than the upside, if you look at related policies like coal phaseout.”

This highlights a central problem for the EU ETS. The phase 4 reforms tackle only one side of the supply-demand balance, by attempting to reduce the number of surplus allowances on the market. Yet the other half of this equation – demand for emissions credits – is also affected by related climate policy, as well as unrelated market forces.

Reflecting this uncertainty, analysts set out a wide range of ETS price predictions at a September 2017 conference organised by specialist newswire Carbon Pulse. It reported that analysts MKonline forecast a €14 peak, due to weak demand as emissions cuts are made for other reasons.

Meanwhile, consultancy Energy Aspects sees a gradual rise to €38 by 2030, interrupted in the mid-2020s by tighter air pollution limits under the EU Industrial Emissions Directive, which force the closure of coal plants burning dirtier lignite fuel.

Emissions – and, therefore, market demand under the EU ETS – have been falling rapidly, according to analysis from Sandbag. It says emissions fell by 2.9% on average between 2005 and 2010, then by 2.6% on average through 2016.

If emissions reductions continue at a similar rate through the 2020s, Sandbag analysis suggests, then the size of the ETS market surplus – currently around 1.7bn allowances – would remain the same until 2030, despite the impact of the phase 4 reforms and the tightened MSR.

Sandbag’s Soloman Williams tells Carbon Brief:

“We can’t see [the reforms] having a massive impact on the carbon price. We still think there will be a relatively low price by 2030, simply because there will be no scarcity [of allowances]. Scarcity drives prices.”

It’s worth adding that analysts’ forecasts have tended to overestimate prices on carbon markets.

What is the best way to strengthen carbon markets?

Views diverge on the appropriate response to the interaction between the EU ETS and other climate policies, sometimes referred to as “overlapping” action.

One solution is simply to avoid raising the ambition of other policies, such as national coal phaseouts or moves to raise the EU’s 2030 targets for renewables and energy efficiency. Yet these other actions are, by their very nature, decided by a wide range of actors and so hard to control.

Fjellheim tells Carbon Brief:

“Countries that want higher carbon prices are also more eager to put in place national policies that would work in the other way, going above and beyond their EU targets. I definitely see a risk that countries will continue to move forward on overlapping policies – at least a risk to the carbon price and the ETS as the main instrument of climate policy…There will always be national aims, policies and electorates so it’s naive to think of the ETS as the only instrument of climate policy.”

Does the EU ETS need a floor price?

Another solution is to underpin the ETS with a minimum “floor price” for carbon emissions, a move pushed by French president Emmanuel Macron in September.

French presidential candidate Emmanuel Macron visits a Deutsche Bahn training programme for young refugees in Berlin, Germany, 10/01/2017. Photo: Soeren Stache/dpa/Alamy Stock Photo.

The Netherlands has pledged to join the UK in setting its own carbon price floor from next year. It will also join Sweden in buying and cancelling allowances. Meanwhile Belgium is also looking at setting a minimum carbon price.

Support for the idea comes in a November 2017 paper published by the Mercator Research Institute on Global Commons and Climate Change (MCC), which says: “The EU ETS is in crisis.” Its authors include prominent climate economist Prof Ottmar Edenhofer.

The paper argues:

“Introducing a carbon price floor can re-affirm the role of the EU ETS as the central pillar in the European effort towards decarbonisation. Such a price floor should start at an economically significant level and rise over time…Many observers argue that it is misguided to focus on the EU ETS allowance (EUA) price, since the emissions cap determines environmental effectiveness and the allowance market works well in technical terms.”

The paper lists a range of arguments against this view, including that the market operates inefficiently due to “private sector short-sightedness and regulatory uncertainty” and that national climate measures dampen the EU carbon price.

It concludes:

“The recent EU ETS reform effort offers an entry point to tackle these concerns, but does not sufficiently address the underlying problems. The magnitude and direction of its impact on the EUA price is highly uncertain. More fundamental change will be required to reaffirm the role of the EU ETS as the central pillar of European decarbonisation efforts.”

[Consultancy Futureproof has an incredibly detailed discussion of the technical and interpretational issues that create ambiguity around the EU ETS and the EU’s overall climate goals.]

Can the EU ETS be changed again?

Arguments over the strength of the EU ETS will continue to play out over the years ahead, with the phase 4 reforms making explicit provision for the rules to be regularly reviewed.

The text says: “The provisions of this directive should be kept under review in the light of international developments and efforts undertaken to achieve the long-term objectives of the Paris Agreement.”

“If there’s political will, [politicians] could still tighten the screw,” says Fjellheim.

The reviews are aligned to the five-yearly timetable of global stocktakes under the Paris deal. This will include an early review of the ETS reforms in the context of the 2018 “Talanoa Dialogue”, which will take stock of progress via three questions (“Where are we? Where do we want to go? How do we get there?”), in order to inform the next round of international Paris climate pledges.

This 2018 review is probably too early to make changes to the ETS, says ICIS’s Ferdinand, given reforms have only just been agreed. Further changes are more likely around the 2023 Paris Agreement stocktake, he suggests.

These regular reviews “may consider whether it is appropriate to complement [the ETS]…with carbon border adjustments”, the introductory reform text says. The parameters of the MSR will also be subject to review, in 2021.

Separately, a 2020 review of the planned international aviation emissions trading scheme, known as CORSIA, will inform a decision on continued exemption of extra-EU flights from the ETS.

The ETS reform text also says: “Action from the International Maritime Organization or the EU should start from 2023.” It requests annual reports from the commission to track progress.

What about Brexit?

One final complication for the EU ETS is the UK’s planned EU exit on 29 March 2019, which falls before the April 2019 ETS compliance deadline for emissions in 2018. In response to this looming deadline, the European Commission proposed a “safeguarding” rule to invalidate UK carbon allowances issued from 1 January 2018, worth around €1bn to government and industry.

The thinking was that if the UK left the ETS in 2019, without a transitional or final deal on the future relationship, then holders of UK industry would no longer need its allowances and could flood the market, sending carbon prices plunging.

After several rounds of furious diplomacy, EU nations recently agreed to a revised safeguarding rule that aims to avoid the writing off of those €1bn in allowances while shielding the EU ETS from market disruption. This agreement is contingent on a rule-change that will bring forward the compliance deadline for UK firms. In a consultation on making this change, the UK government says:

“To ensure a smooth transition and avoid a cliff edge on withdrawal, the UK has proposed to the EU an implementation period of about two years where we would continue to have access to each other’s markets on current terms. We are calling for this to be agreed as early as possible to provide clarity.”

Ferdinand tells Carbon Brief: “A transition period would postpone the cliff edge, but the difficulty would still be there. But you could be much better prepared.”

As to what happens to the UK’s participation in the EU ETS after Brexit and any transition period, the UK government has been making holding statements that keep all options open. On 20 November, for example, climate minister Claire Perry told parliament:

“The government is considering all options for the UK’s future participation, or otherwise, in the EU Emissions Trading System after our exit from the EU. The effect on the cost of EU allowances will depend on the nature of the UK’s future relationship with the system and will be taken into account as part of this consideration.”

-

Q&A: Will the reformed EU Emissions Trading System raise carbon prices?

-

"Putting a price on carbon": Will EU trading reforms raise carbon prices?