Jeremy Bentham is vice president global business environment for Shell. He joined the company in 1980 and since 2006 he has been responsible for developing Shell’s energy scenarios to support the company’s strategic thinking and direction.

- Bentham on carbon capture and storage (CCS): “If you look at the depth of CCS investments that is required, that is quite a feasible amount of investment”.

- On recent CCS progress: “I would say it is disappointing, in terms of what we really need to achieve over the coming decades, if we’re going to address those particular challenges of emissions.”

- On whether 2C is politically and socially plausible: “[2C scenarios] have become less plausible…the kind of policy and regulatory developments that needed to take place, haven’t taken place”.

- On the twin challenges for the world’s use of energy: “What is really really critical…is a world that is prosperous for everyone… and with net-zero emissions. Now, in our outlooks that looks socially, politically and technically feasible over the course of this century.”

- On publishing Shell’s 2C scenarios: “Well, I’m not sure how helpful it would be. If we think it would be helpful into the public debate then we would bring that forward.”

- On the Paris talks: “Here’s [a chance to] highlight and get behind the spreading of the carbon pricing mechanisms in the world and, also, the kind of attention to investment and policy required to promote CCS”.

- On phasing out coal: “We mustn’t just take a narrow, rich-world view of the world and [so we need to] recognise that coal can be an important energy source for the developing nations, the economy in India, the economy in China”.

CB: I’d like to start with a question about solar. Recently, Shell CEO Ben van Beurden said he expected solar to become the world’s dominant energy source. When you developed the New Lens scenarios a few years ago, those see solar potentially taking that spot by maybe mid-century. But since then quite a lot’s changed – prices have come down a lot – so what’s Shell’s view on when solar will reach that position?

JB: Thank you for the question. And, indeed, if you look at the scenarios that we’ve produced, our understanding is that in the second half of the century, in both of our scenarios — both Mountains and Oceans — solar will become what we call the backbone, ie the single largest primary energy source. Although there will continue to be a very, very important mix, and we can talk about that later. It happens in the Oceans scenario somewhat before, maybe one to two decades before the Mountains scenario, but that’s the direction of travel. The development of solar has continued to be along the lines of our scenario understanding. If we go back to some earlier versions of the scenario expressions that we call “Blueprint” and “Scramble”, which really looked at the rate of regulatory development and technology deployment, Blueprint was the faster scenario. And whilst many developments in the regulatory space have tended to be along a [slower] Mountains or a Scramble type of pace, the pace of technology and costs has fallen [along] the [more rapid] Blueprints line.

CB: So you don’t really think that the developments in rapidly falling solar costs is significantly changing your outlook?

JB: We see that it is falling rapidly, but that is kind of what we anticipated over time. It’s already factored [into] the thinking that we have.

CB: Another feature of your scenarios is CCS. Ben van Beurden said that carbon capture and storage (CCS) is needed “without delay” to clean up fossil fuels. It’s something that Shell’s been active in developing. Under your Mountains scenario, CCS power capacity in 2050 looks like it would be larger than the world’s current fleet of coal, and I just wonder if you still think that’s plausible, given recent developments. For example, Drax’s decision on the White Rose project.

JB: Well, I think that, first of all, it’s very hard to compare apples and pears about the size of various things. If you look at the depth of CCS investments that is required, that is quite a feasible amount of investment that’s required to achieve that. If you compare that with the level of total investments in the energy system, or if you compare it with total investments required in urban development over the next decades. Those are much larger type of developments, so the scale of development is large, but that’s because the global energy system is very, very large, but it’s not beyond the bounds of feasibility. It’s really whether there are going to be the incentives in place to enable that development. It’s not really about technological aspects, although there are still important tests to be made that bring different well-known technologies together. It’s really whether you have in place mechanisms such as carbon pricing that really put a value on avoiding emissions, and, hence, can drive that investment into CCS.

CB: I suppose what I was getting at really was the question of, you know, you had this scenario that you set out, but that was a few years ago and since then progress has been slower than people hoped and expected for CCS.

JB: I think that’s true and, so, the pace of development has again fallen within the boundaries of the scenario work. In the Oceans scenario it was envisaged that CCS would develop more slowly because of various factors, including the fact that those regulatory developments don’t come into place as rapidly. So it’s not unexpected within that broader framework. You know, I would say it is disappointing, in terms of what we really need to achieve over the coming decades, if we’re going to address those particular challenges of emissions.

CB: On the question of emissions, and reducing them over the coming decades in order to avoid dangerous climate change, do you think — given your work on scenarios — that a 2C target is politically and socially plausible?

JB: Well, I think that we laid out in our scenarios the real challenges to that. If we look back at the work that we were doing a decade ago, you could see pathways that were very plausible, towards that kind of outlook. Those have become less plausible because over time, the kind of policy and regulatory developments that needed to take place, haven’t taken place. We remember how disappointed people were with what happened in Copenhagen in 2009. So those developments mean that the timing is a concern, as you look forward. But both of our outlooks, if you’re able to look at them in detail, do put forward an understanding that what is really, really critical, can be achieved, which is a world with net-zero emissions. In fact, I’d take it further than that, or broader than that: a world that is prosperous for everyone, with a spreading of prosperity from the minority population of the world to the majority population of the world, and with net-zero emissions. Now, in our outlooks that looks socially, politically and technically feasible over the course of this century. Clearly, the more quickly that that is achieved, the closer to any particular temperature limit that you can approach.

CB: If I could just press you on that. Does what you said mean, given that progress has been slower than it needed to be, does that mean you don’t think 2C is still plausible?

JB: I think that it’s a challenge, and you have to have almost the “goldilocks” scenario, which is the best of all worlds. It’s a world in which you get deep collaboration between policymakers, businesses, industry, and civil society, academia, NGOs etc. So it takes all these things to line up to be able to bring that kind of pace of development. Now, different people will have different views on the likelihood of that lining up, but clearly, personally myself and as a company, we are committed to trying to foster that kind of cross-boundary collaboration.

CB: So, has Shell ever tried to produce a scenario that would be compatible with a 2C world?

JB: Well, yes, that’s called normative scenarios, and you can mathematically try and force things, and learn from that, see what would really have to happen. And so our scenario work encompasses doing that kind of outlook and, hence, we know about what I call the goldilocks outlook. But, also, our scenarios have to stretch our thinking about what are the likely features and the likely uncertainties in the future environment. And that’s what they have reflected in both the Mountains and Oceans outlooks.

CB: Neither the Oceans nor the Mountains scenarios that you published were compatible with a 2C future, but you say that you have looked at scenarios that would be. So is that something that Shell would ever publish?

JB: Well, I’m not sure how helpful it would be. If we think it would be helpful into the public debate then we would bring that forward. But, clearly, the requirements are well known, mathematically. You know that you’re essentially talking about net-zero emissions in the early part of the second half of the century. Mountains and Oceans show that net-zero emissions is feasible. The timescale tends to look towards the end of the century, but if those goldilocks elements can be brought together, then that can be accelerated. You know, and, in fact, those emissions profiles that we have, we have to combine that with thinking from others, around non-energy emissions, because clearly there are plenty of emissions that are non-energy related. We’re experts on the energy side, but we have a relationship with the climate modellers at MIT, for instance, who have taken those scenarios and added to them with the non-energy emissions, and, actually, show the kind of temperature rise, on average, that would be associated with those — and that’s less than 3C, it seems. That’s the challenge now, I think for us, broadly as society, is, how do you blend those two great moral imperatives of our time? One is spreading the quality of life, the modernity, the benefits of modernity from the minority population to the majority population. And how do you achieve net-zero emissions?

CB: I’d like to go on to energy demand, which is, obviously, a key part of your scenarios work. Your chief executive has said on occasions that energy demand is likely to double and that that will create a need for Shell’s products and other fossil fuels, despite things like the solar expansion that you see happening. Judging from the speech that Ben [van Beurden] gave yesterday, Shell effectively sees rising energy demand as a given. How do you see demand developing over the next few decades and are there any scenario you can imagine where demand wouldn’t rise at that rate?

JB: I think, I mean, obviously, we do a lot of modelling and econometrics and all those fancy things that you’d expect. But you can actually take it back and understand it in a more straightforward way. If you look at the advanced economies, the industrialised economies, then you can see the kinds of amounts of energy that are required to support a particular form of life. So, here in Europe, for example, which is relatively energy efficient, you need about — sorry about the technical term — about 150 gigajoules (GJ) per year per person, to support this quality of life. I’m going to put that in slightly more straightforward terms. If you actually look at the energy or the work that can be done by a physical labourer, that amounts to about a GJ per year, so what we’re actually talking about is everybody in Europe on average has 150 personal labourers, at low cost, but personal labourers working for them. If you go into a different kind of economy such as a North American economy, you’re talking about 300GJ per person. We estimate that over time, with attention to efficient end use and efficient infrastructures, like compact cities, perhaps around about 100GJ per year is sufficient to give people a decent quality of life. Now, if you take 100GJ per year and look towards the end of the century at 10 billion people in the world, then you multiply those numbers and you get, round about, a thousand exajoules (EJ) per year. So, again, with high efficiency, 1,000EJ per year, and that’s about double what you have today. So, if you’re going to have a world in which you have this spreading of comfort and prosperity to more people, then you’re talking about a doubling of the energy system required to provide the houses, the materials, the water systems, the sewage systems, the transport systems that are required for that.

CB: Earlier this year in one of its regular market reports, the International Energy Agency talked about the world entering a new normal for oil, where low prices were failing to ignite demand as expected because of things like increasing energy efficiency, as well as other structural changes in the global global economy. How’s that sort of thinking being reflected in Shell’s scenario work?

JB: Yes, well, the restructuring of economies and the impact of prices and price elasticities are all things that are part of our thinking, and our modelling of the energy system. It’s why I can look at that total energy demand over time and say that it doesn’t have to relate to a north American style of energy use — that 300GJ per person per year — but could translate over time into 100GJ per person per year. Those are all factors that we take into account. If we fail as a global society to invest in those efficient infrastructures and efficient end uses, then demand is going to, in fact, grow beyond what I said.

CB: I’d like to ask if Shell’s assumptions on rising energy demand are one reason why the scenarios aren’t compatible with 2C?

JB: Again, I think it’s that point of blending the likely developments in terms of spreading the benefits of modernity with the emissions challenge, so these things come together. They can’t be separated. We’re in a world in which we need more energy and fewer emissions, so one of the great opportunities and challenges for the energy system going forward is how you co-evolve, with both objectives, both the established parts of the energy system and the emerging parts of the energy system, to best address those opportunities and challenges.

CB: Shell is one of the driving forces behind the recently Energy Transitions Commission, which has been set up with McKinsey and other organisations to address some of the big challenges that you’ve talked about. Do you see its work as an extension of the scenario team’s work and what are you hoping it will achieve?

JB: First of all, I think it’s important to recognise that whilst we’re very supportive of the Energy Transitions Commission, it’s not a Shell commission. We understand that across the world there are important dialogues about both economic development and emissions, and that we see that these dialogues are often narrowly framed, or dysfunctional in some way and so we hope that the Energy Transitions Commission can be part of stimulating better forms of dialogue. So, we’re very supportive, but we’re one of several players who are supporting this. It’s set up as an independent commission. The academic work that it does, or the analytical work that it does, will be overseen by an independent academic observers and bring that forward. So, I think it will do its work and bring forward useful understanding and input that we will use in our scenarios as well. I suspect that as with one of its predecessors – the Global Commission on the Economy and Climate, the New Climate Economy work – we will probably be very comfortable with a certain percentage of what comes out of there and there’ll be other things that we’ll find challenging. But that’s the way of the world, that’s the way we drive things forward. So, it’s good to have another independent perspective and we’re happen to support that.

CB: The commission frames its goals of enhancing energy access and prosperity within the need to stay below 2C. We’ve talked already about Shell’s scenarios not being compatible with 2C. So, is this new commission in some ways an admission that Shell’s attempts to find an economically sustainable and environmentally sustainable path to 2C has been a bit of a failure?

JB: No, I don’t think that I would express it that way. I think that we’ve tried to lay out our best understanding, so that people can engage in that debate and that dialogue about what’s needed. So, I think we’ve been very clear that deeper collaboration across sectors – government, business, academia and other parts of civil society – is going to be essential to blending and achieving those kinds of goals that I laid out about a prosperous world for everyone, with net-zero emissions. So, I think it’s completely compatible with that, that we’re supportive of this independent commission, and we hope that that helps improve energy dialogue and move us more progressively and constructively along over the coming decades.

CB: I’d like to ask about the COP21 meeting in Paris in December. In the past, Shell’s response to questions about stranded assets has effectively been that governments aren’t or won’t take the action required for a 2C world. What would have to happen at Paris, or what one detail of the Paris agreement, would make you change your mind?

JB: I think that, here’s another opportunity to, for example, highlight and get behind the spreading of the carbon pricing mechanisms in the world and, also, the kind of attention to investment and policy required to promote CCS. So those would be two very, very important things. But also, this recognition that there’s a dog and a tail in the world, and sometimes people get them mixed up. The nature of the energy system is shaped by the consumption of energy, the needs of consumption, the different sectors whether those are residential sectors, or they’re service sectors, or they’re industrial sectors. The energy system, if you like, the energy companies, are the tail part of that. Recognising the importance of encouraging the restructuring of the broader economy over time is as significant as a very narrow focus on energy production companies. So, we hope that that deeper recognition of how this is something that requires a broad framing, would also come out of the [Paris] talks. One of the things, as someone that’s been involved in scenarios, that I’m appreciative of is the way that the developments over the last few years have been more along the lines of our previous Blueprints scenario, which recognised the difficulty of herding whatever number of national cats, 190-odd national cats, into a single agreement, and the more likely evolution of policy around nationally contributions, which come together and add to each other and can learn from each other and evolve over time. So, that structure that’s emerged feels to us more likely to be a successful structure than what has been attempted previously.

CB: That’s interesting, it really leads into the next question I was going to ask. There’s an expectation that Paris will agree some sort of five-yearly cycle of pledge and review, which is, perhaps, a little bit like the UK’s five-yearly carbon budgets process. Given what you’ve said and your experience on scenarios, would you say that’s a good model to adopt?

JB: Yes, I do. We put a lot of thought into this. When I say we, we don’t work in isolation, we work with a vast network of external subject matter experts and sometimes with very different perspectives and try to learn from those as well. And, clearly, we felt that the kind of mechanism that’s evolving is more likely to accelerate developments over time, which is why we included it in that more accelerated scenario, which was the Blueprints scenario.

CB: I’d just like to come back to what you said about the tail and the dog in terms of energy demand versus energy companies. Do you think, perhaps, that underplays Shell’s role, I mean Shell’s such a big part of the global energy system? Do you not think there’s, perhaps, a space for Shell to act in some kind of leadership position? Historically, it worked on solar, for instance. It has worked in CCS, biofuels. Is there a bigger role that Shell could take in not only trying to satisfy the demand – the dog – but, actually, also to wag the dog and try and push things in the right direction?

JB: Well, I think so, and I think we attempt to do that. First of all, you’ve got to understand that much as we are a company with a high profile, I think we’re still only about 2% of the global energy system. So, if there’s a tail, then there’s a few hairs on the tail and we’re one of the bigger hairs on the tail, but we’re still a small part of that. So we can’t wag the tail or wag the dog completely at all. But we have expertise, we understand technology, we act globally and so we can see across the world of developments and we try and bring our voice and our expertise into these conversations. You’ve been asking me particularly about scenarios and one of the reasons why when we do multi-decade broadscope scenarios that we publish them is to bring that voice into public dialogue.

CB: You mentioned in relation to Paris, Shell’s calls for carbon pricing, which it would like governments around the world to embrace. What would that actually look like in practice, and what’s Shell actually planning for?

JB: First of all, I think amongst people who are listening to this, I think will understand that in order to incentivise investment or choices on demands, then you need to value them, you need to have some kind of mechanism that prices them. Hence, we see that in that co-evolution of the established and emerging forms of energy supply, carbon pricing has an important role to play. The way that it’s happening, of course, is that it is tending to develop various national or regional systems, and there’s a need for those to grow, but clearly also to link in some way. We’re a supporter of the International Emissions Trading Association and their developments in thinking about how to link these systems over time.

CB: I’d like to ask about the Arctic and I wondered whether the scenario team, in your broader work within Shell, was an influence on the decision to pull out of Alaska, or whether, perhaps, you see Arctic oil exploration as part of the future.

JB: There’s a dilemma there. Clearly, for many people, either people in the economy, in communities in Alaska, as well as people in our company who have been working on this are disappointed on the technical outcome of that work. And I think that our scenario work highlights the dilemmas that we all face in looking at a world which is going to need, for the comfort of the majority, the energy being developed from multiple sources, and, also, at managing emissions over time. Clearly, the Arctic is a very special environment, it’s a pristine environment, but we and others have been able to operate there responsibly over time. So, I think the scenarios help lay out the issues, and as global society and as an actor in global society, we will see that playing out and evolving over the years ahead.

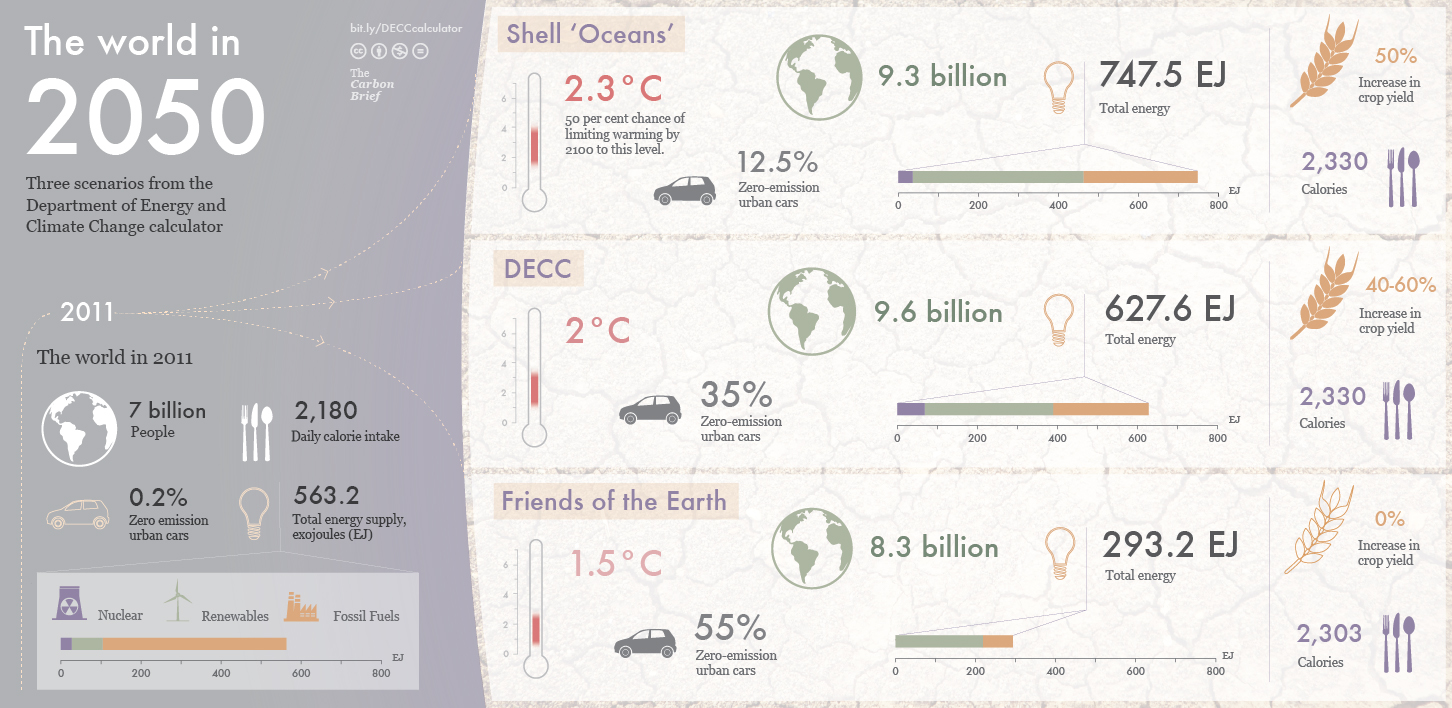

Infographic: Three scenarios from the DECC calculator. Credit: Rosamund Pearce for Carbon Brief.

CB: So, I just wonder when, over the last few years, while Shell’s been going through that internal discussion, and externally with, you know, NGOs and so on, whether you’ve been having conversations with the leadership team talking about your scenarios for future prices, for instance? And particularly coming back to carbon pricing, obviously, Shell has for a long time had a shadow carbon price. And with the expanse of oil exploration in challenging environments like the Arctic has that not been part of the conversation?

JB: Oh, it’s certainly been part of the conversation. So, I’m part of the Corporate Strategy Leadership Team, and our understanding of the business environment, which is often encapsulated in scenarios, is part of that ongoing dialogue, and ongoing process. So, you’ve referred to the Mountains and Oceans outlooks and those date actually from already a few years ago. And the dialogue just continues as the understanding of those is absorbed and reflected in the kinds of decisions that are made over time, and our new work which we will share over time as that becomes more crystallised.

CB: You mention new work and I was hoping to ask whether Shell will in future publish a new set of scenarios and whether it’s conceivable that one of those might, perhaps, be a 2C compatible one?

JB: Well, I think that we have more recently last year published a supplement around one of the topics that is really, really important to grapple with, which is urbanisation. So a New Lens on future cities, capturing our understanding of that, because urbanisation is one of the great phenomena of our time. I think people will look back in the future at the period from 1950 to 2050 as the century of the city, when most of the world urbanised. And, clearly, when that takes place it has a huge footprint on efficiency, on resource demand: water, energy, land-use. And we put a lot of attention into that, and I think that probably some of the next type of material that we’ll share our understanding on is around the outlook of a prosperous world with net-zero emissions, and what’s actually required to achieve that, and then we can help be part of the dialogue at a nitty-gritty granular level about that.

CB: I mean when would you expect that? Is there some kind of set time-table for those sorts of new understandings, new scenarios to be published?

JB: There’s no set timetable. A lot depends on when the insights become firmer, but also simply on where the dialogue is and when will it be helpful. But I think this is something that in the course of next year we will be delighted to share our thinking about. And we already do share our thinking about that – in a sense some of the factors are already included in those New Lens scenarios, Mountains and Oceans. But it’s when you look at these things as a whole together and draw lessons from it as a whole, that you can then begin to speak about particular issues like that.

CB: You’ve talked quite a bit about net-zero emissions. Many of the 2C scenarios that have been developed by other organisations and academics and so on rely on negative emissions to get to a net-zero position. Given what you’ve said about CCS, and given your work on scenarios, what’s your view on negative emissions?

JB: Well, I think that, indeed, that is part of the story and is clearly why you need also to have CCS combined with sustainable biomass activities. So that you have things like…power generation from biomass combined with CCS, and the reason why the negative emissions are an important part of the totality is that there are going to be certain sectors of the economy, such as iron and steel manufacturer, cement manufacturer, which are almost impossible to decarbonise, at least in any kind of foreseeable time-frame. So, you’re going to need CCS not only to mop up remaining emissions, but also to create the opportunity for negative emissions. So, given the importance of that technology in any future outlook, then you also need the incentivisation, the investment within that, which is why you come again back to the importance of carbon pricing mechanisms.

CB: OK. So is this something you can see Shell throwing its technical and engineering expertise behind? I mean is it something that Shell scientists might start looking at?

JB: Well, I mean we have already invested not only attention, but also funds into important CCS activities. And before long we’ll be opening up the big plant in Canada, the QUEST project as well. So, indeed, these are areas where we not only put our attention and our scientific outlook, but also our investment dollars, but as part of this broader understanding of what’s required to take not only a few pilot plants, what is required to make a development like this be deployed at scale.

CB: OK. I’d like to ask about coal. It’s been particularly topical in the UK at the moment: a newspaper report yesterday suggesting that the government may look to phase out coal-fired power station within, perhaps, a decade or so. On a global level, would you say that phasing out coal is the most important step we can take to tackle emissions?

JB: Well, I think we have to again have a blended, mature view on this. I mean clearly if you’re looking at coal as a thermal fuel, or as a thermal fuel for power generation, then you can take alternatives, such as natural gas, and deploy natural gas, and you can essentially halve the emissions, and that’s available and possible. And so that kind of development can be important, but also, again we mustn’t just take a narrow, rich-world view of the world and [so we need to] recognise that coal can be an important energy source for the developing nations, the economy in India, the economy in China, and will continue to be an important source, although again, the other elements and other technologies can play an important role. You’ll note the announcements from China, from the Chinese government about how they see their emissions developing, and you’ll probably see peak coal in China in the next few years. So, again, this is an evolution and we need to take a broad view on it, and not just a rich-country view on it.

CB: You mentioned natural gas as a potential replacement for coal. Given the length of time the energy infrastructure lasts, how long do you see that window because you’ve talked about the need to get to net-zero emissions, but, obviously, gas isn’t zero-emissions. So if you replace a lot of coal with gas, there’s a limited window before we get to zero, so can you just talk about that a bit?

JB: Yes, well, first of all the understanding needs to be that when we’re talking about climate stability, or ocean acidification – all the different impacts of emissions – these are cumulative effects. So, being fast is very important, and one of the fastest things you can do is to replace the use of coal by the use of natural gas, and so that’s one of the reasons why I highlighted that. And, indeed, gas is low-emissions, half the carbon emissions, but also low-emissions in terms of other particulates and so on and so it has advantages within that, and so you can see how over time gas, and then gas with CCS can play an important role in the future energy developments, you know alongside things that are going to be increasingly important, such as solar and wind. There are no silver bullets and how these evolve together is going to be important.

CB: OK, I mean would you, given the strategic decisions that Shell’s been taking investing in CCS, taking over British gas exploration, investing in energy… would you say that Shell’s vision of the future of itself as a company is based around natural gas and carbon capture and storage?

JB: No, I think that…it’s interesting sometimes to take a historical perspective on these things and we’re in a time of transition. And we’ve been through transitions before, so in the 19th century effectively coal was coming on top of wood and peat and dung historically as places like the United Kingdom, United States industrialised. In the 20th century you’ve got that spreading of industrialisation also mobility, you began to see oil and gas come on top of coal use, as we had more of the benefits of modernity deeper and spreading. We’re in a century now where you’re going to see more factors, such as solar, wind, etc, coming on top of the other energy sources as well. So, these are all times of transition. Shell as a company has been at the frontier of energy transitions over the last transition so we have a deep expertise in oil and gas and related technologies, that we can bring into the 21st century activities. I think that we will seek to be a successful company in the 21st century.

CB: What does that actually mean for Shell? You’ve talked about the world moving to zero emissions – perhaps in the 2060s or, perhaps, not until the end of the 21st century – but, ultimately, that means a world where a lot less oil and gas is burned, perhaps, very little unless it’s got carbon capture and storage. Where is the role for Shell in that world?

JB: I think if you look in that world, we’re an energy systems developer and we will continue to be an energy systems developer. Oil and gas have got a significant role to play for many many decades ahead, as part of that and, that will be part of the portfolio. But already we have broader portfolios, whether that’s in biofuels that you mentioned, and we will continue to look for attractive opportunities to be part of that broader development.

CB: Thanks very much.

JB: You’re welcome.

Main image: Shell’s Jeremy Bentham. Credit: Friends of Europe/Flickr

This interview was conducted by Simon Evans on 7 October 2015 at the Shell Centre, Shell's London HQ.

-

The Carbon Brief Interview: Jeremy Bentham

-

Shell's Jeremy Bentham on CCS, Paris talks, 2C and phasing out coal.