Explainer: How can climate finance be increased from ‘billions to trillions’?

Josh Gabbatiss

11.04.22Josh Gabbatiss

04.11.2022 | 12:12pmFrom the moment in the early 1990s when nations began grappling with the threat posed by climate change, money has been at the heart of discussions.

Over a decade ago, rich countries promised to raise $100bn each year by 2020 to help developing countries pay for climate action.

But they failed to reach that target. Now, under terms set out in the Paris Agreement, nations negotiating at the UN have been tasked with setting a new one by 2025.

It is clear that existing climate finance is nowhere near what is required. To phase out fossil fuels and protect their citizens from worsening climate disasters, developing countries will need trillions rather than billions of dollars.

Rich countries are under pressure to pitch in more money, but the jump from billions to trillions will likely require more than they are willing to provide from their public coffers.

Nations such as the US want to lean more on the private sector to fund this global transition. Others want to see a complete overhaul of the global financial system so that funds can be more effectively channelled into climate action.

In this article, Carbon Brief explores some of the options on the table for raising levels of climate finance and more broadly ensuring that the flows of money around the world are consistent with global climate goals.

- What is climate finance?

- How much climate finance is needed?

- Boosting private investment

- Reforming international financial institutions

- Special drawing rights

- Just energy transition partnerships

- Expanding the pool of contributors

- Dealing with debt

What is climate finance?

“Climate finance” is a term typically used to refer to any money that is used to either cut emissions or help people adapt to climate change. (Some nations and campaigners hope to expand its definition to include money for “loss and damage” from climate change – see below.)

In the context of UN climate negotiations, the term “climate finance” refers to the money raised by a small group of developed countries to fund climate action in developing countries.

This notion has its roots in the early 1990s, when countries first met to design a climate change treaty. From the outset, developing nations said they needed money and the US, in particular, resisted their demands.

The resulting UN Framework Convention on Climate Change (UNFCCC), agreed in 1992, stipulates that “developed” countries:

“[S]hall provide new and additional financial resources to meet the agreed full costs incurred by developing country parties.”

The specific countries identified and listed in “Annex II” of the UN convention were western European nations, the US, Canada, Australia, New Zealand and Japan.

This was based on membership of the Organisation for Economic Co-operation and Development (OECD) at the time, meaning it does not include the likes of China.

They were tasked with providing financial support to other nations because they held more responsibility for causing climate change and had greater capacity to deal with it.

This finance is vital, not least because many developing countries’ climate pledges are conditional upon receiving it. The latest UN analysis suggests these conditional promises could be the difference between 2.4C and 2.2C of warming by the end of the century.

Despite its importance, there is no universally agreed way of accounting for climate finance. As such, countries can use their own definitions when they report this finance to the UN.

Commonly cited figures tend to be self-reported or provided by the Organisation for Economic Co-operation and Development (OECD), a club of rich nations. However, estimates by Oxfam and independent researchers suggest that the “true value” of climate finance may be just a fraction of the amounts claimed by developed countries.

Developing countries emphasise the “new and additional” requirement for climate finance. This concept was never defined due to lack of agreement, but is often viewed as meaning money that is provided on top of other development aid.

In practice, it is clear that climate finance is often considered a component of existing aid programmes. Only two nations – Norway and Sweden – provide climate finance that goes beyond the broadly agreed aid target of 0.7% of gross national income.

Developing countries also stress the need for grant-based finance rather than more loans for nations that are already burdened with debt. As it stands, only around one-quarter is provided as grants, with Japan and France providing nearly all their climate finance as loans.

How much climate finance is needed?

For years, organisations such as the World Bank have talked of a “billions to trillions” agenda, wherein billions of dollars in aid catalyses trillions in further investment. As the issue of climate finance grows in urgency, there is rising pressure to make this a reality.

In 2009, developed countries agreed to “mobilise” $100bn a year by 2020. (As with the term “climate finance”, the definition of “mobilise” is vague.)

This arbitrary figure, pushed by then-US state secretary Hilary Clinton at COP15 in Copenhagen, was first proposed by UK prime minister Gordon Brown during a speech at London Zoo earlier that year. It was not based on analysis of developing countries’ needs.

Nevertheless, this number was confirmed in the Cancun Agreements the following year, emphasising the need for “new and additional” finance with a balance between mitigation and adaptation. The Paris Agreement in 2015 also reinforced the $100bn goal and its decision text refers to meeting the target with support from a range of sources:

“Public and private, bilateral and multilateral sources, such as the Green Climate Fund, and alternative sources.”

It also said that, having continued to mobilise at least $100bn each year between 2020 and 2025, nations negotiating at the climate summits:

“[S]hall set a new collective quantified goal from a floor of $100bn per year, taking into account the needs and priorities of developing countries.”

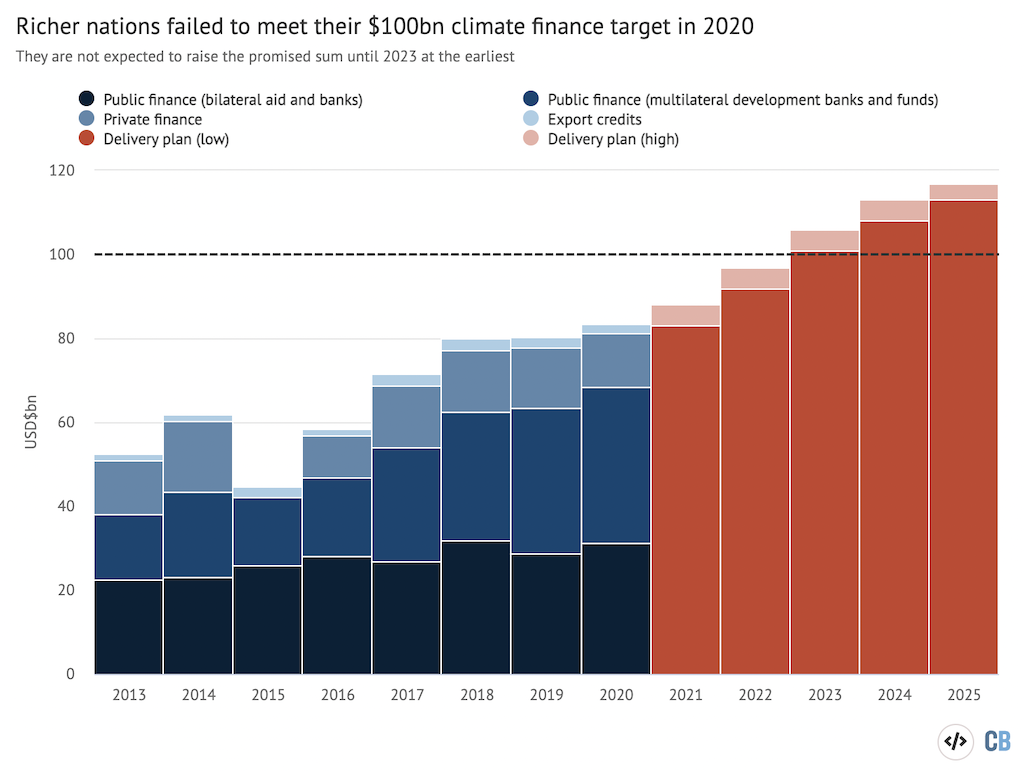

So far, developed countries have failed to reach the $100bn goal, as the chart below shows. According to the OECD, they mobilised just $83.3bn in 2020.

The developing countries’ “delivery plan” – indicated by the red bars below – suggests that they are unlikely to meet the target until 2023 at the earliest. This has been reiterated in an update to the plan ahead of COP27.

Climate negotiators at COP27 are now tasked with working out the terms of the “new collective quantified goal”, which will take effect from 2025.

Unlike the $100bn target, this goal is being negotiated within the UN over the next three years. This is a requirement of the Paris text, which says the new target must be higher than $100bn and must “tak[e] into account the needs and priorities of developing countries”.

Developing countries want the new target to be based on – not just informed by – a rigorous analysis of their “needs and priorities”. This includes setting a clear definition of climate finance, the lack of which risks undermining trust between parties, they say.

The Glasgow Pact that emerged from COP26 “emphasises” taking into account “the needs of those countries particularly vulnerable to the adverse effects of climate change” and “significantly increasing support for developing country parties, beyond $100bn per year”.

There are also growing calls for the new target to include loss and damage finance for the first time, on top of finance for cutting emissions and adapting to climate change.

Paying for all of this low-carbon energy and climate-resilient infrastructure will require very large sums of money. Some of this will undoubtedly come from the developing countries themselves – and the private sector – but they are pushing for developed countries to bear a significant chunk of the costs via climate finance.

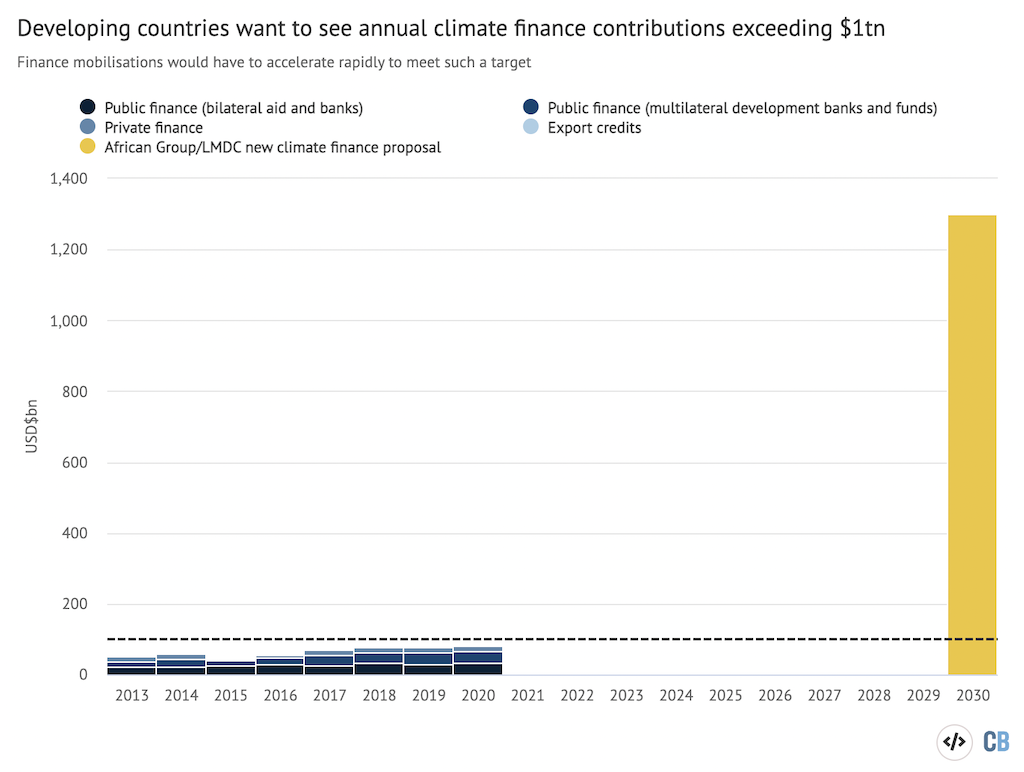

An early proposal put forward by the Like-Minded Developing Countries (LMDCs) and the African Group at COP26 included a figure of $1.3tn each year by 2030, with a “significant percentage on a grant basis”. As the yellow bar in the chart below shows, this would require a huge step up from the existing $100bn target.

Most estimates for finance needs do not distinguish between developing countries’ domestic spending and finance provided by foreign actors, but the sums required are easily in the trillions of dollars.

The Intergovernmental Panel on Climate Change’s (IPCC) most recent report concludes that climate-related investment in developing countries must increase by between four and eight times until 2030, in order to meet the Paris Agreement warming limits. This would bring annual climate investment in these nations to around $2-3tn annually.

The Standing Committee on Finance, set up to aid understanding of climate finance within UN negotiations, has assessed 153 climate plans submitted to the UN by developing countries. It found that even though only around half had provided costed estimates of some of their needs, this subset alone would require $5.8-5.9tn in total by 2030.

The International Energy Agency’s (IEA) most recent World Energy Outlook (WEO) concludes that, for its 1.5C-compatible scenario, annual clean-energy investment needs to triple by 2030, reaching $4.2tn. Roughly $1.8tn of this would be in emerging and developing countries.

The UN estimates that climate adaptation in developing nations alone will cost between $160bn and $340bn each year by 2030.

While the figures appear daunting, activists often place them in the context of money that wealthy countries raise to fund their own domestic priorities.

The IEA estimates that predominantly “advanced” economies have committed “well over $500bn” to shield their citizens from the impacts of the energy crisis, for example. The EU alone committed €750bn ($848bn) to help member states recover from the Covid-19 pandemic, and other wealthy nations committed billions more in “green recovery” funds.

On top of the specific climate-finance targets, Article 2.1c of the Paris Agreement text takes much wider aim at all “finance flows”. It says strengthening the global response to climate change includes:

“Making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development.”

This goes far beyond developed countries providing financial assistance to developing countries. It acknowledges that the world also needs a total transformation of global finance, with all public and private money aligned with the goals of cutting emissions and strengthening climate resilience.

Beyond simply supporting climate-relevant projects, such as low-carbon energy, this suggests that nations should also be winding down their investment in fossil-fuel projects.

Some nations, both developed and developing, want to see this part of the Paris Agreement given more attention at COP27.

Boosting private investment

Climate finance can involve businesses in developed countries investing in climate-related projects – such as solar farms or wind turbines – in developing countries.

Wealthy nations and multilateral development banks (MDBs – see below) can encourage private entities to invest in these kinds of projects by providing grants, low-interest loans or loan guarantees to “derisk” investments and get projects off the ground.

Given the trillions that need to be raised, there is broad recognition that private money has a significant role to play in scaling up overall climate finance.

The IEA estimates that $3tn of the $4.2tn needed in global investment by 2030 to achieve the 1.5C target would come from the private sector, “mobilised by public policies that create incentives, set appropriate regulatory frameworks and send market signals”.

US climate envoy John Kerry has repeatedly emphasised the role of the private sector, stating “no government in the world has enough money to solve the climate crisis”.

However, private finance should not be seen as a replacement for public funds, explains Preety Bhandari, a senior adviser in climate and finance at the World Resources Institute. She tells Carbon Brief:

“There is also concern among developing countries that developed nations are deflecting some of their responsibility in the UNFCCC context by placing an overriding emphasis on the role of the private sector.”

A statement by the LMDC group ahead of COP27 described moves by wealthy nations to shift the focus onto businesses as efforts to “dilute their responsibilities under the UNFCCC and its Paris Agreement”.

What is more, the evidence suggests that private finance is simply not living up to expectations. In their delivery plan for the $100bn goal, developed countries stated that “mobilising private climate finance has proven to be challenging”.

The OECD’s analysis of progress towards the $100bn target includes private finance that has been “mobilised by official climate-finance interventions” from developed countries. Just $13.1bn of the reported finance came from the private sector in 2020, an amount that has stayed roughly the same over the past decade.

A separate analysis of “blended” finance – where development aid is used to leverage additional private or public funds – found that the amount of money being provided in this way for climate-related projects had sunk from $36.5bn between 2016-2018 to $14bn between 2019-2021.

One issue is that businesses generally opt for investments they perceive as safe, as Joe Thwaites, international climate finance advocate at the Natural Resources Defense Council (NRDC), tells Carbon Brief:

“We often hear two things – you hear the private sector is amazing, entrepreneurial, innovative…and then you also hear, oh boy, the private sector isn’t going to invest in developing countries because it’s too risky.”

Private climate finance tends to favour investment in wealthier nations that are viewed as more stable over some of the low-income nations that are most in need of help. The latter often come with higher risk premiums and costs associated with borrowing when investing in them.

The IEA’s WEO report states that the higher “cost of capital” in developing and emerging economies is a reflection of “real and perceived risks” in these nations.

Concerns about returns on investment also skew funding towards mitigation rather than adaptation. While clean-energy infrastructure can be highly profitable, adaptation measures often do not provide obvious financial gains, unless they protect a company’s assets.

According to the Climate Policy Initiative, 98% of adaptation finance in 2019 and 2020 came from the public sector.

Reforming international financial institutions

Public climate finance can either be provided by one country to another, or it can be channelled through large international financial institutions.

There have been growing calls for reform of these entities to help bring the money they distribute more in line with climate ambitions, particularly in developing countries.

Over the past few years, roughly 40% of the climate finance provided by developed countries has flowed through multilateral institutions.

A fraction of this comes from specialised climate funds, such as the UN’s Green Climate Fund, but the majority is provided by multilateral development banks (MDBs), such as the European Investment Bank or the Asian Development Bank.

Some countries, notably the US, give the majority of their climate finance through MDBs.

MDBs were first established towards the end of the second world war by the US and its allies, as part of an effort to rebuild countries. Together with the International Monetary Fund (IMF), the World Bank and the International Bank for Reconstruction and Development were termed Bretton Woods institutions after the meeting where they originated.

They are large organisations with a wealth of expertise and resources, which are funded by their developed country members. As public institutions, they can support early-stage technologies and projects that the private sector is likely to avoid.

Nevertheless, these institutions have come under fire for failing to live up to the scale of challenges facing the world, including the Covid-19 pandemic and climate change. Some have called for a “new Bretton Woods”, with new rules and systems that steer spending towards societal benefits, such as tackling environmental threats.

One particularly vocal critic has been the prime minister of Barbados Mia Mottley. Her government has been seeking support for its Bridgetown Agenda for the Reform of the Global Financial Architecture, which proposes significant changes to how MDBs operate. It also calls on MDBs to distribute reconstruction grants following climate disasters and proposes measures to deal with the “debt crisis” (see below).

In a lecture on the sidelines of the World Bank and IMF meetings in October, Mottley said:

“The global financial architecture was never designed for us. It was designed when we were still colonies…we were not seen, we were not heard, we were not felt.”

A key criticism of MDBs is that they are simply being too conservative and that they could distribute more money without developed countries having to pay more into them.

Some observers have argued that the MDBs are currently holding back on lending in a bid to maintain their AAA credit ratings – the highest possible score, meaning the lowest possible risk of defaulting. One analysis suggests that opting for a lower credit rating could allow some banks to triple their lending.

An influential report for the G20 concluded that the MDBs could increase their lending by “several hundreds of billions of dollars over the medium term”, if they followed a handful of recommendations. As Dr Rishikesh Ram Bhandary, a climate-finance expert at Boston University Global Development Policy Center, tells Carbon Brief:

“This report found that the MDBs could be lending a lot more without having to go through a capital increase…these MDBs have the ability to be providing a lot more climate finance now.”

Mottley’s Bridgetown Agenda calls for MDBs to follow the recommendations from the G20 report and expand their lending to developing countries by $1tn in total.

Proposals for reform are not only coming from leaders in the global south. US Treasury secretary Janet Yellen has said the World Bank and other MDBs need to “evolve” to address climate change, a sentiment echoed by other nations including the UK and Germany.

Yellen emphasised that these institutions should do more to encourage private investment. She also said they should consider more grants and “concessional” loans – meaning loans offered on generous terms below the market rate – to help middle-income countries transition away from coal. In a speech at the Center for Global Development, she stated:

“If the global community benefits from investments in climate, then the global community should help bear the cost.”

(Her comments came amid a scandal involving World Bank president David Malpass, who was accused of being a climate sceptic.)

Experts have argued that aligning the MDBs with the Paris Agreement also requires these institutions to phase out their investments in fossil fuel infrastructure. Ultimately, shareholder governments from both developed and developing countries have the power to push for these changes.

Special drawing rights

The use of special drawing rights (SDRs) to provide climate finance is a novel proposal that has risen to prominence over the last year.

The idea has been championed by Barbados’s Mottley in her proposals for global financial reform. However, this use of SDRs would come with certain limitations and the extent of their future use remains to be seen.

SDRs are a “global reserve asset” maintained by the IMF. They are not money, but they can be swapped for money at a willing central bank in a country that has plenty of spare foreign currency – such as dollars.

The country that provided the money will then hold onto the SDRs, with the understanding that it could undertake a similar swap in the future if it were ever low on dollars.

Countries can use the money obtained with SDRs however they want, giving them the freedom to channel their SDRs into climate projects.

In 2021, the IMF issued an unprecedented $650bn in SDRs, describing the move as “a shot in the arm for the global economy at a time of unprecedented crisis”, referencing the economic shock caused by the Covid-19 pandemic.

However, these assets are distributed according to an IMF quota system that is highly skewed towards wealthy nations. The US alone received SDRs worth $113bn, while all low-income nations together received just $21bn.

Yet the US and other major economies already have plenty of foreign currency reserves, meaning their SDR allocations are going largely unused. In contrast, newly issued SDRs have proved useful in many lower income nations.

This has led to a push for these SDRs to be reallocated to low-income nations, as Nadia Daar, head of the Washington DC office of Oxfam International, tells Carbon Brief:

“This is no skin off anyone’s back. Rich countries channelling the SDRs they are not using anyway comes with little to no cost. And we are not only talking a few billion, but many multiple billions could be achieved potentially for any number of under-invested areas, including climate.”

The re-channelling of $100bn in unused SDRs is a key component of Mottley’s Bridgetown Agenda, as well as a new issuance of 500bn SDRs – worth $650bn – or “other low-interest, long-term instruments”. The IMF has created a $45bn Resilience and Sustainability Trust for rich nations to re-channel their SDR funds to developing countries.

Mobilising money from SDRs can prove complicated and expensive, however, as countries have to pay interest on SDRs that leave their accounts and often need to seek approval from parliaments before channelling these assets.

Given these issues, Daar emphasises that any redistribution of SDRs should be in addition to meeting the climate finance goals that rich countries are currently missing.

She notes that re-channelled SDRs passed from one country to another would “most likely” come in the form of loans, meaning new issuances of the kind proposed by Mottley “are more valuable for countries rather than recycled SDRs.”

Just energy-transition partnerships

At COP26, a new model for climate finance was revealed in the form of an agreement between the governments of South Africa, France, Germany, the UK and the US, as well as the EU.

Dubbed a “just energy-transition partnership” (JETP), the $8.5bn scheme involves developed nations financially supporting South Africa’s shift away from coal.

South Africa is a major emitter due largely to its reliance on coal, which still provides nearly 90% of its electricity. Ending this reliance therefore has global implications for addressing climate change.

At the same time, the coal industry employs tens of thousands in a nation where around one-third of people are unemployed. This is why the focus on a “just transition” that does not leave coal-dependent communities behind is a crucial aspect of the JETP concept.

The G7 has since announced that similar partnerships are in the works with other coal-dependent nations including Indonesia, Vietnam and India, as well as Senegal, which relies on heavy fuel oil for much of its power generation. Other nations reportedly under consideration are Egypt, Côte d’Ivoire, Kenya and Morocco.

The IEA has noted the “immense value” of such initiatives, noting the need for climate finance to “tackle the various economy-wide or project-specific risks that deter investors”.

If such interventions could cut the cost of financing clean energy projects in developing countries by 200 basis points (2 percentage points), the IEA said, it would cut the overall cost of reaching net-zero by $15tn through to 2050.

Money being provided for JETPs would likely count towards the broader climate finance obligations of the nations involved.

Partner countries have emphasised the importance of working cooperatively, promoting national ownership from the beneficiary nations and wider benefits such as boosting energy access and job creation. However, as details of the South African partnership slowly emerge, it is clear that there are issues with the model.

One concern is the risk of simply replicating the same problems that are seen in other forms of climate finance.

According to a leaked draft of the South African JETP package seen by Climate Home News, around 97% of the $8.5bn will be delivered as loans and investment guarantees. This is despite South African president Cyril Ramaphosa stating that he would only accept the deal if it was on good terms, with most of the money coming as grants.

US climate envoy John Kerry has also expressed an interest in funding JETPs by selling carbon offsets to private companies. This could prove controversial given scepticism about companies relying on offsets to meet their climate goals.

Another issue is that the JETP model of financing can be viewed as rewarding a historical reliance on fossil fuels, potentially overlooking some of the nations that need finance most. Faten Aggad, a senior adviser in climate diplomacy at the African Climate Foundation, explains this concern to Carbon Brief:

“If I take the case of Africa, the distinction is not only between middle- and low-income countries, but also between high polluters and low polluters – with a tendency in the short-term to ignore the latter, which is problematic.”

South Africa and Senegal, for example, both have relatively high rates of electricity access compared to some of their neighbours, which have not constructed as much fossil-fuel infrastructure.

Expanding the pool of contributors

One option to increase the amount of international climate finance is to simply expand the list of contributors.

As it stands, only the nations of western Europe, the US, Canada, Australia, New Zealand and Japan, plus the EU, are obliged to provide climate finance under the UN system.

This list of “Annex II” countries was originally intended to capture the “developed” countries regarded as responsible for causing climate change. It was based on membership of the OECD when the UNFCCC was signed three decades ago.

Therefore, it omits large emerging economies, notably China and Russia, wealthy non-western nations, such as South Korea and Chile, and major oil producers including Saudi Arabia and other Gulf states.

Many of these nations do, in fact, provide climate-related finance to developing countries. However, it is not considered official climate finance and does not, for example, count towards the $100bn target.

With negotiations over the post-2025 finance target now getting underway, some developed countries have argued for expanding the pool of contributors.

There is a reasonable argument for this on the basis of historical responsibility. As of the most recent data, Annex II nations are only responsible for 40% of historical carbon dioxide (CO2) emissions, whereas China alone is responsible for 11%.

However, the proposal has seen firm opposition from developing countries. In particular, the LMDCs – a group that includes many large emerging economies and oil producers – have consistently argued against any changes to the original divisions between countries set out in the UNFCCC.

Tracy Carty, a climate-finance lead at Oxfam, tells Carbon Brief that, while the question of adding more contributors is “reasonable”, it is hard to justify in the context of developed countries missing the $100bn target:

“They haven’t met their own goal and now they’re saying other people need to come on board.”

Aggad tells Carbon Brief that African nations have shown little appetite for expanding the donor list. She notes that countries recognise that constructive discussions about financing from non-Annex II nations can take place outside of the UN system. China, for example, is not an official climate-finance contributor, but is a major financier of African energy projects.

Dealing with debt

Many of the nations that are most in need of finance also face a heavy debt burden, which makes funding climate-related projects difficult.

According to the World Bank, 58% of the world’s poorest countries are in debt distress or at high risk of it.

Meanwhile, analyses have shown that low-income countries spend five times more on debt than climate adaptation, while small-island developing states spend 18 times more paying back debts than they get from climate finance.

Calls for debts to be wiped out have been amplified by the floods that struck Pakistan this year. The UN Development Programme argued for relief on Pakistan’s billions of foreign debt so it could focus resources on dealing with the climate-related disaster.

Most climate finance is in the form of loans and so contributes to the problem of debt. More grant-based finance could help to remedy this. With this in mind, one proposal is that the post-2025 climate finance goal should have a sub-target specifically for grants.

So-called “debt-for-climate” swaps have also been suggested as a way to address the debt crisis and boost climate spending. These swaps involve a partial forgiveness of debt by the creditor nation, with the money being used domestically to fund climate-related projects.

This idea has been around for decades and has so far only seen limited use – including a frequently cited example of a “debt-for-nature” swap in the Seychelles.

There has been renewed interest in recent months, with hopes that such initiatives could help scale up climate finance more broadly.

-

Explainer: How can climate finance be increased from 'billions to trillions'?