In-depth: Renewables are ‘key’ to lower UK industrial electricity prices

Simon Evans

02.05.18Simon Evans

05.02.2018 | 5:08pmOnshore wind is key to securing lower industrial electricity prices for the UK, a new report says.

Unlocking investment in the renewables, which offer the cheapest sources of electricity, is one of the recommendations of today’s University College London (UCL) report, prepared for the Aldersgate Group, an alliance of business, academic institutions and NGOs.

The report also finds that continental industrial power prices are often lower than those in the UK because of better links between neighbouring electricity grids, “activist” industrial policy and reliance on old generating capacity that is nearing the end of its life.

It confirms that climate policy costs are not the decisive factor. Prof Michael Grubb, professor of energy and climate change at University College London and one of the report’s two authors, tells Carbon Brief: “It’s kind of nonsense, the idea that it’s driven by carbon-related policies.”

Sweeping generalisations

Today’s report is the most comprehensive attempt so far to examine UK industrial electricity prices in an international context. As it notes: “Much of the UK debate on electricity prices has been at a level of either technical detail, or sweeping (and often questionable) generalisations.”

(Carbon Brief has explored many of these “questionable generalisations” in articles on the UK steel crisis and a House of Lords energy report, among others.)

The report comes in the wake of the government’s “Cost of Energy Review”, written by the University of Oxford’s Prof Dieter Helm. This was supposed to clear a path to the government’s manifesto pledge of having the “lowest energy costs in Europe, both for households and business”.

The manifesto, in turn, was co-authored by Nick Timothy. The former policy adviser to prime minister Theresa May had masterminded the Conservative election campaign, after which the party lost its majority. Since losing his job, Timothy has continued to attack climate change policy, arguing it is “impos[ing] higher energy costs and lower industrial output”.

In contrast, the government’s independent Committee on Climate Change (CCC) said that wholesale costs and network charges were to blame for higher industrial electricity prices, rather than climate policy. It said last year:

“Differences in low-carbon policies cannot explain the difference in electricity prices, which stem primarily from higher wholesale and network costs…It is not clear why these costs are higher in the UK than in many comparable countries.”

Today’s report confirms and expands on this. It then offers ways to minimise costs in future.

Industrial electricity prices

Since 2000, UK industrial electricity prices have more than doubled. Most of this was due to rising international fossil fuel prices before 2008, when the UK passed its Climate Change Act.

The UK is highly exposed to wholesale gas prices, the report notes, since the liberalised market of the 1990s led to the “dash for gas” and increased reliance on the fuel.

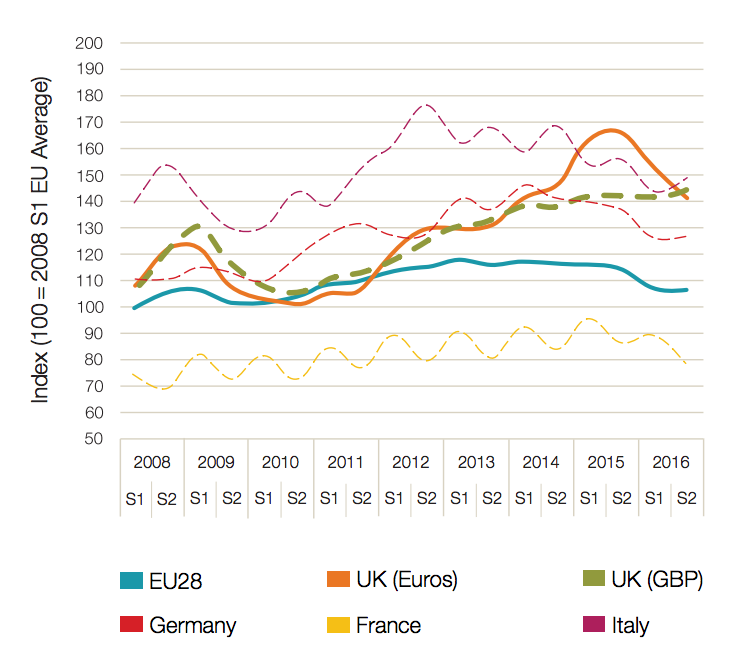

After 2008, prices continued to rise in the UK, but also elsewhere in the EU, as the chart below shows.

Average electricity prices for industrial users in the UK (orange and green lines) compared to the EU average (blue) and other member states. Source: UK industrial electricity prices: competitiveness in a low carbon world.

After 2012, UK industrial electricity prices started to diverge from the EU average. A particularly large spike in euro-denominated UK power prices, around 2015, was due to the strength of the pound, whereas sterling-denominated prices held steady.

This exchange-rate effect harmed the competitiveness of UK industry by raising its cost base relative to overseas firms – and not just in terms of energy. It also made UK exports relatively more expensive. The pound has since fallen back to levels seen in 2010 or 2011.

Other factors driving the divergence with other EU countries include the UK’s exposure to gas, noted above, with prices peaking in 2013, well after a peak in coal prices. Like the UK, Italy is also reliant on and exposed to gas.

In contrast, France gets most of its electricity from nuclear plants built in the 1970s and 80s, while German electricity prices tend to be set by coal. You can see these differences in the map, below.

Shares of EU member states’ electricity consumption in 2017 met by coal (black shading, top left), gas (blue), nuclear (pink). Darker colours show heavier reliance on that source. Source: The European Power Sector in 2017, Sandbag and Agora Energiewende. Maps by Carbon Brief using Highcharts.UK prices after 2012 were also driven by rising investment in the electricity sector, after a lack of investment during the 2000s, and the carbon price floor, the UK’s unilateral top-up carbon tax. Note that while this contributed to a growing gap between UK and EU average prices after 2012, it cannot explain this difference (see below) and some industrial firms are compensated for the cost.

UK prices

It is this divergence in relative industrial electricity prices after 2012 that has caught the attention of UK commentators and policymakers. Indeed, the fact that UK prices are higher than in France or Germany is well-established, even if the reasons behind this have not been understood.

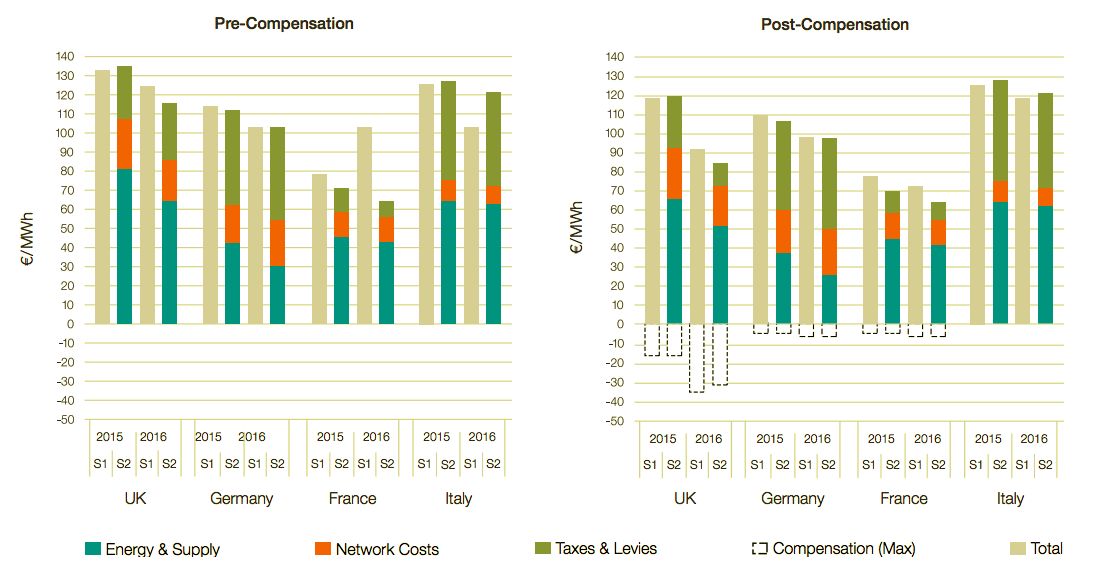

For the average industrial user in the UK, prices in 2016 were 35% above the level in 2008 and a similar amount above the EU average, which was relatively static over that period, the report says. This difference is illustrated in the chart on the left, below.

(The report’s focus is on four EU countries: the UK, France, Germany and Italy. These countries span nearly the full range of EU industrial electricity prices and all have large industrial sectors. The chart shows euro-denominated prices, so part of the fall from 2015 to 2016 in the UK is due to the falling pound.)

Left: Industrial electricity prices in the UK, Germany, France and Italy (grey bars), and the breakdown of costs (coloured bars). Right: Costs after the maximum compensation for policy costs, which is available to some users. Source: UK industrial electricity prices: competitiveness in a low carbon world.

The chart on the right, above, shows that with maximum compensation, UK users in 2016 faced lower prices than in Germany or Italy, while they remained slightly above those in France.

(Note that other countries make greater use of exemptions, instead of compensation. This makes the UK look worse than it actually is, in the pre-compensation figures published by Eurostat, which can, therefore, be “quite misleading”, Grubb says. The UK is now moving towards exemptions.)

Grubb tells Carbon Brief: “It’s quite a messy picture, but for the big companies with full compensation, they’re pretty much at average EU prices. For those industries that don’t have [compensation], they are clearly in the high end of the EU.”

If prices for the largest industrial firms are around the EU average, this potentially undermines the whole premise of recent concern over “disadvantaged” UK industry. On the other hand, it’s fair to say that not all firms receive compensation.

Cost compensation

Eligibility for compensation is complex and varies between different schemes and countries, but the broad outlines are determined by EU-wide state aid rules. In principle, firms that face competition from overseas and with high electricity costs as a share of their outgoings can get compensation. This means those without it should be able to pass on their higher costs to their customers.

Report co-author Paul Drummond, a senior research associate at UCL, tells Carbon Brief:

“Those electricity-intensive processes, businesses and sectors deemed at risk of international competition – and, thus, offshoring – are those that are eligible for compensation for EU ETS [EU emissions trading system] costs in the UK, Germany and France, as well as the CPS [carbon price floor] and renewable support costs in the UK only.”

Eligible firms got 85% compensation for carbon price costs during 2013-15, falling to 80% in 2016-18 and 75% in 2019-20. This includes indirect costs passed through by electricity suppliers. In the UK, some firms also get 85% compensation for the costs of renewable subsidies, while some German firms also get a discount at similar levels.

Policy costs

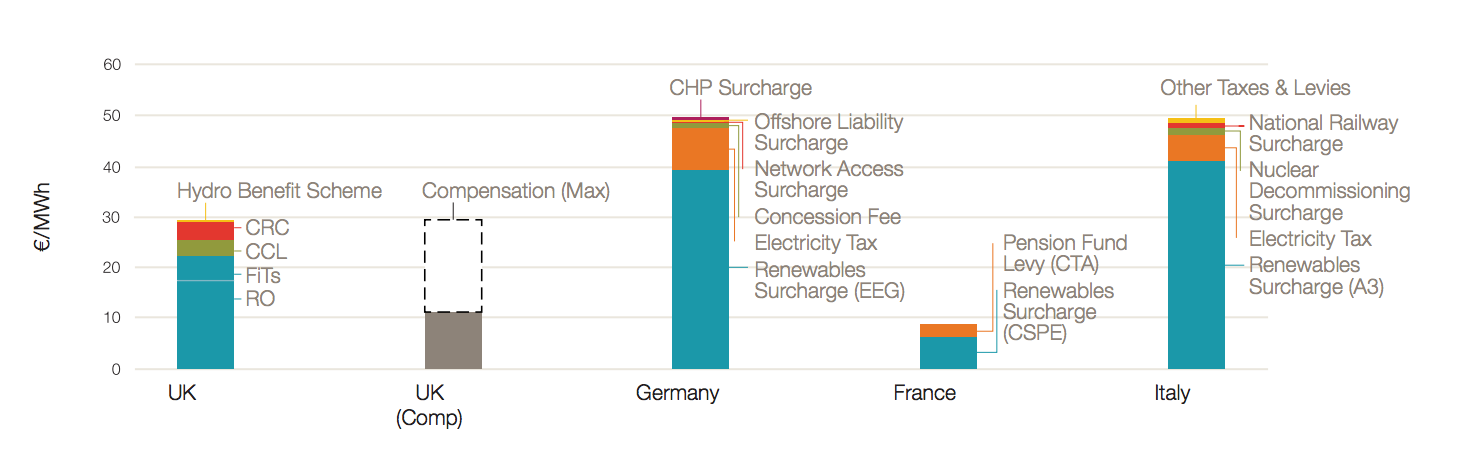

Today’s report divides policy costs into two sections. First, it shows that taxes and levies – including support for renewables – cannot explain higher prices in the UK. In fact, UK industrial electricity faces lower taxes and levies than in Germany or Italy, as the chart below shows.

Taxes and levies on average industrial electricity prices in the UK, Germany, France and Italy in euros per megawatt hour. For the UK, the total is also shown after maximum compensation, available to some users. Source: UK industrial electricity prices: competitiveness in a low carbon world.

Grubb tells Carbon Brief:

“UK industry, even without compensation, is paying less in taxes and levies than Italy or Germany. It’s significantly less. [So] it’s kind of nonsense, the idea that it’s driven by carbon-related policies.”

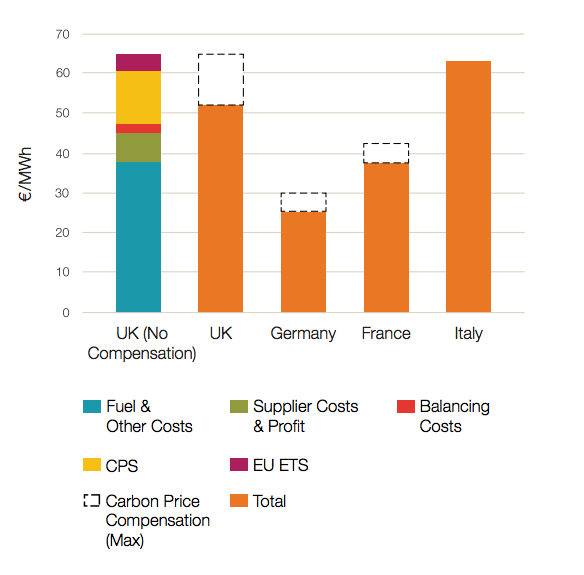

Carbon pricing – the second part of policy – is listed under “energy and supply” in the report. Here, policy is once again unable to explain lower costs on the continent. Even if the UK’s carbon price floor were set to zero, costs would be higher than in France or Germany, as the chart below shows.

Energy and supply costs of average industrial electricity in the UK, Germany, France and Italy in the second half of 2016. For the UK, the cost is broken down into its components. Source: UK industrial electricity prices: competitiveness in a low carbon world.

Other explanations

If policy costs cannot explain the higher industrial electricity prices for uncompensated UK firms, then what other explanations can there be? As noted at the beginning of this article, while the CCC pointed to UK wholesale electricity prices and network costs, it did not explore why these differed.

However, the UCL report shows that network costs are actually almost equal across the four countries it looked at. Instead, it is the way these costs are shared between consumers that differs. In the UK, costs are shared relatively equally between domestic, business and industrial users whereas in Germany, France and Italy industry is cross-subsidised by smaller consumers.

This is one example of what the report calls a more “activist” approach to industrial policy on the continent. Another example is the French “Exeltium” consortium, a large group of industrial firms that negotiated a cheaper fixed-price, long-term electricity supply contract with French utility EDF. This sort of arrangement would be “incompatible” with the UK’s historic approach to promoting competition between industries, the report notes.

Besides these factors, it is in wholesale electricity prices where the largest and most obvious differences lie. These can be explained by the makeup of countries’ electricity mix and the past policy and investment decisions they stem from.

As the maps above show, Germany is more reliant on coal, for which prices fell sooner after 2012 than for gas. Part of its fleet uses lignite, a low-quality high-emissions coal that is cheap.

In contrast, the UK and Italy are reliant on international gas markets. Even if the UK were to develop a domestic shale gas industry – and even if it could extract gas as cheaply as in the US – this would be unlikely to cut UK gas prices, which are part of a larger, integrated European market.

Order of merit

Germany has also benefited from the merit-order effect, whereby renewables cut wholesale prices by pushing the most expensive generators out of the system.

If you ever wanted to understand the merit order effect, this animation (and article) is for you:https://t.co/beU2eBEduD pic.twitter.com/d0GgW4IYwm

— Simon Evans (@DrSimEvans) May 12, 2017

This cut German wholesale prices by €14-16 per megawatt hour (MWh) in 2016, the report says, with a similar saving in Italy, against a lower €7/MWh effect in the UK. These savings offset part of the policy costs discussed above.

For France, the wholesale price is low because it relies on nuclear plants built decades ago. The country also benefits, as does Germany, from being closely connected to the grids of neighbouring countries, whereas the UK and Italy are less integrated.

This explains one of the report’s recommendations, which is that the UK should continue to expand its interconnection capacity as planned, despite planning to leave the EU. This should help prices converge between the UK and the continent, as long as the UK maintains access to the EU’s internal energy market. (This remains a big if).

Unlocking wind

The other key recommendation of the report is for the UK to unlock investment in renewables, since this is now the cheapest way to generate electricity. New onshore windfarms, for example, could deliver electricity below current UK wholesale prices, if industry were to embrace them.

This directly contradicts the arguments of Timothy and others, who have argued on grounds of cost that the UK should slow climate policy, in general, and limit expansion of renewables, in particular.

The government should hold an auction for long-term “subsidy-free” contracts for such technologies, the report says, while looking at restrictive planning rules as part of a wider “full-scale” review of onshore renewables.

This could be combined with a renewed carbon price escalator, the report argues, along with continued cost exemption or compensation for heavy industry.

The government should also consider a more ambitious reform, whereby standardised power purchase agreements for renewables are bought and sold by industrial users in a “green power pool” that shares the system costs of backing up variable wind output.

Firms buying into this pool could get reduced rates by offering flexible demand to match variable supply. They would also avoid paying the rising carbon price, which would only be applied to trades on the wholesale electricity market.

Finally, the government could facilitate industry directly buying cheaper continental electricity via interconnectors, similar to systems already in place in Italy and California.

Looking ahead

Overall, these proposed reforms, along with other changes already underway, offer a chance to bring UK industrial electricity prices in line with those on the continent, say the report’s authors.

Grubb says:

“We present quite strong reasons why the UK is likely to converge to a large degree with continental prices. Our recommendations are really to accelerate and deepen that.”

Moreover, the conditions that make wholesale electricity in Germany and France cheaper than in the UK could soon evaporate.

Most of Germany’s coal fleet is old and will ultimately need to be replaced, though the debate on how or when to phase out coal is less advanced than in other countries. The country is also planning to close its remaining nuclear plants, which still supply a significant share of its mix. This will squeeze market supply and raise prices.

In addition, EU ETS carbon price rises in the wake of recent reforms would hit Germany particularly hard, given its reliance on coal-fired power.

For France, the country faces the costs of the life extensions needed to keep its ageing nuclear flee open for longer. This is an estimated €55bn, the report notes. Then there is the cost of decommissioning, estimated by utility EDF at €300m per gigawatt but widely expected to be higher.

In total, the UK could improve its relative position, but is unlikely to meet the government’s aim of having the lowest costs in Europe. Grubb tells Carbon Brief:

“My sense is that in the mid-term it’s reasonable for the UK to aim for mid-range – maybe even better than much of western Europe. But it is rather fantastic to imagine our prices could compete, for example, with Norway, or even some of central and east European countries, with both cheaper labour and [abundant] hydro.”