Q&A: Can the UK meet its climate goals without the Wylfa nuclear plant?

Simon Evans

01.21.19Simon Evans

21.01.2019 | 4:37pmThe Japanese firm Hitachi has shelved a planned new nuclear plant at the Wylfa site on Anglesey in Wales, leaving a large hole in the UK government’s climate and energy strategy.

The news comes just months after the planned Moorside plant in Cumbria was scrapped by Toshiba, another Japanese conglomerate. Hitachi’s UK subsidiary, Horizon, has also suspended work on a third new nuclear scheme at Oldbury in Gloucestershire.

New nuclear plants were due to replace old reactors as they retire through the 2020s, helping to plug the gap left by coal-fired power stations being phased by 2025. They form a key part of the government’s plans to “keep the lights on” while meeting the UK’s legally binding climate goals.

However, recent analysis from the government’s official advisers the Committee on Climate Change (CCC) shows the UK could meet its power demand and climate goals to 2030 at low cost, without any new nuclear beyond the Hinkley C scheme already being built in Somerset.

This new analysis reflects the dramatic cost reductions seen for renewables in recent years. Greg Clark, the UK’s secretary of state for business, energy and industrial strategy (BEIS), made a similar point last week as he spoke in parliament about the failed Wylfa deal. He told MPs:

“The economics of the energy market have changed significantly in recent years. The cost of renewable technologies such as offshore wind has fallen dramatically…The challenge of financing new nuclear is one of falling costs and greater abundance of alternative technologies, which means that nuclear is being outcompeted.”

The outlook to 2050 is much less certain and, for Clark, nuclear will continue to have an “important role” in the future UK energy mix.

Modelling from the Energy Technologies Institute and Imperial College London suggests new nuclear would help to keep costs down as the UK approaches zero emissions. Work by Aurora Energy Research finds that a highly renewable energy system in 2050, with no new nuclear added after Hinkley C, might have similar overall costs as a high nuclear pathway.

In this in-depth Q&A, Carbon Brief looks at what the Wylfa news means for the UK’s climate goals and what role nuclear might play in future.

What has happened?

The Japanese conglomerate Hitachi has shelved the planned new nuclear plant at Wylfa on Anglesey in Wales. The 2.9 gigawatt (GW) dual-reactor project would have cost a reported £20bn, according to the Financial Times, while others say it would have cost £16bn. [The difference is likely due to whether the figure includes financing costs or not.]

Hitachi will write off £2.1bn already put towards the project. Its UK subsidiary Horizon has also suspended work on the 2.9GW Oldbury new nuclear plant in Gloucestershire, BBC News says.

The news follows Toshiba’s decision, in November 2018, to wind up its NuGen subsidiary in the UK. NuGen was to have built the 3.3GW Moorside new nuclear plant in Cumbria.

The door remains open to Hitachi resurrecting the schemes, but according to the Japanese newspaper Asahi Shimbun: “Analysts and investors viewed the suspension as an effective withdrawal.”

Why does it matter?

Together, the three planned plants at Wylfa, Moorside and Oldbury would have had a combined capacity of 9.1GW and generated 72 terawatt hours (TWh) of near-zero carbon power per year. This is roughly what the UK’s existing nuclear fleet produces, generating around a fifth of the country’s electricity last year.

Generating this amount of electricity with gas would lead to emissions of roughly 29 million tonnes of CO2 each year (MtCO2), around 8% of overall UK emissions in 2017. This level of emissions would be even more significant in the context of shrinking UK carbon budgets.

There are eight nuclear power stations operating in the UK today, with a total capacity of 8.9GW. With the exception of Sizewell B in Suffolk, these were all built in the 1970s and 1980s.

These older reactors are due to retire during the 2020s and are shown in shades of grey in the chart, below. Sizewell B (black) was built in 1995 and is due to retire in 2035, though operator EDF wants to extend its life by as much as 20 years until 2055.

Some six new nuclear plants had been under development around the UK, totalling 18GW (coloured chunks in the chart). The Hitachi news means three have now been shelved (red).

Current and expected capacity of nuclear plants around the UK, gigawatts, between 2018 and 2030. The final column includes proposed plants with no government contract or time schedule. Operating sites are shown in shades of grey. Schemes still under development are in blue and those that have been shelved are in red. Source: World Nuclear Association and Carbon Brief analysis. Chart by Carbon Brief using Highcharts.The government has also pledged to phase out by 2025 the UK’s six remaining large coal plants, totalling nearly 11GW. These continue to play an important role during periods of peak demand, but operate for relatively few hours across the year and generated 17TWh in 2018 (5% of the UK total).

New nuclear formed a key part of government plans to replace retiring reactors and coal. BEIS has some 7GW of new nuclear being built by 2030 in its latest energy and emissions projections. This is equivalent to Hinkley C in Somerset, plus at least three additional reactors at one or more sites.

Published a year ago, these projections scaled back the pace of nuclear new build compared to earlier outlooks, but, nevertheless, included steady growth throughout the 2020s and beyond.

Can the UK still meet its climate goals?

The sheer scale of the now-shelved nuclear schemes leaves a large hole in UK climate plans. But legally binding carbon budgets to 2030 could still be met without any additional new nuclear plants, according to analysis from the CCC.

Last year, the CCC published updated scenarios for the power sector through to 2030. These plot a range of pathways to meeting the UK’s 2030 climate goals, only some of which add new nuclear beyond the Hinkley C plant that is already being built in Somerset.

The chart below compares nuclear’s contribution to UK generation in 2018 (red chunk, left-hand column) with a range of scenarios for 2030 (remaining columns). Each scenario limits power sector carbon intensity in 2030 to 100 grammes of CO2 per kilowatt hour (gCO2/kWh) or below.

The CCC’s “central renewables” and “high renewables” scenarios meet the 2030 carbon target without new nuclear beyond Hinkley C. In these scenarios, nuclear generation in 2030 is 35TWh – the estimated output of Hinkley C plus Sizewell B, each running for 90% of available hours.

The UK’s current electricity generation mix and carbon intensity (2018 actual, left-hand column) compared with scenarios for 2030 from BEIS and the CCC (remaining columns). Electricity generation in terawatt hours (TWh) is broken down by fuel into nuclear (red), fossil fuels (shades of grey), renewables (shades of blue), imports (light grey) and carbon capture and storage (CCS, purple). The carbon intensity for each scenario is shown above the columns. Source: Carbon Brief analysis, BEIS energy and emissions projections 2017 and CCC Progress Report 2018. Chart by Carbon Brief using Highcharts.Note that each of the 2030 scenarios supplies enough electricity to meet projected demand, meaning the lights would not “go out”. Gas would still supply 20-25% of electricity, most of which would be used to cover peak demand during winter or to fill gaps in variable renewable output.

The CCC scenarios out to 2030 all massively expand renewables, whether or not additional new nuclear plants get built. The renewable share of the mix increases from 33% in 2018 to at least 58% in 2030. Nuclear’s share falls from 18% in 2018 to between 10% and 17% in 2030. At the low end, where no new nuclear is added after Hinkley C, it is renewables that make up the gap.

[The CCC says: “We do not consider [the BEIS 2030] pathway credible.” This pathway sees nuclear’s share hold steady, though, as BEIS notes, this is “not based on [nuclear] developers’ proposed pipeline”. BEIS also assumes imports via electricity interconnectors reach 21% of the total while the CCC assumes net-zero imports, with interconnectors helping balance supply and demand.]

The CCC says expanding wind and solar is a “low-regrets” option as renewables are likely to be cheaper than new gas, with similar costs to running existing gas plants or raising imports, even after accounting for the costs of integrating their variable output onto the grid. The CCC adds:

“If new nuclear projects [beyond Hinkley C] were not to come forward, it is likely that renewables would be able to be deployed on shorter timescales and at lower cost.”

Replacing the output of the shelved new nuclear plants at Wylfa, Moorside and Oldbury with renewables would be 13-33% cheaper, including the costs of balancing variable output, according to quickfire analysis from the Energy and Climate Intelligence Unit.

Note that reductions in per-capita electricity generation have saved the UK the equivalent of four Hinkley Cs of demand since 2005, according to recent Carbon Brief analysis. The CCC assumes continued efficiency improvements to 2030 are offset by demand for electric vehicles and heating.

What about the UK’s 2050 target?

The route to meeting the UK’s climate goals in 2030 is relatively clear, with or without the likes of the Wylfa new nuclear plant. Looking out to 2050, however, the path becomes much more uncertain – not least because the UK is set to raise its targets in line with the Paris Agreement.

Other reasons for caution around longer-term pathways include fundamental uncertainty about the future, the need for extra electricity to help decarbonise heat and transport, and an expectation of rising costs to integrate variable renewables as their share grows beyond 50 or 60%.

As Clark told MPs:

“The government continue to believe that a diversity of energy sources is the best way of delivering secure supply at the lowest cost and that nuclear has an important role to play in our future energy mix…Having a substantial mix of technologies has an insurance quality. We should recognise that, but there is a limit to what we can pay for the benefit, which is reflected in my statement.”

Several recent analyses have investigated the UK’s electricity mix to 2050, in light of these challenges, uncertainties and the recent renewable cost reductions.

First, there is the modelling from the Energy Technologies Institute (ETI) published in late 2018. This suggests the least-cost path to 2050 includes 7GW of new nuclear by 2030 and 21GW by 2050.

The ETI notes this may not be “realistic”, but still emphasises the need for “low carbon baseload capacity [such as nuclear or CCS] to complement renewable generation”. It adds: “The scale of the requirement will depend on progress in developing storage and demand side flexibility.”

Second, there is the modelling for the CCC carried out by Imperial College London and published in summer 2018. This includes the option to balance seasonal variations in renewable output using “power-to-gas”, where electricity is used to make hydrogen that can be stored for later use.

This modelling suggests nuclear’s role in the future energy mix could be replaced using power-to-gas, with stored hydrogen being used to fill the gaps in variable renewable power output. However, Imperial says this would be around 10% more expensive than a 2050 scenario including nuclear or another source of “firm low-carbon capacity”, meaning one that can be turned on at will.

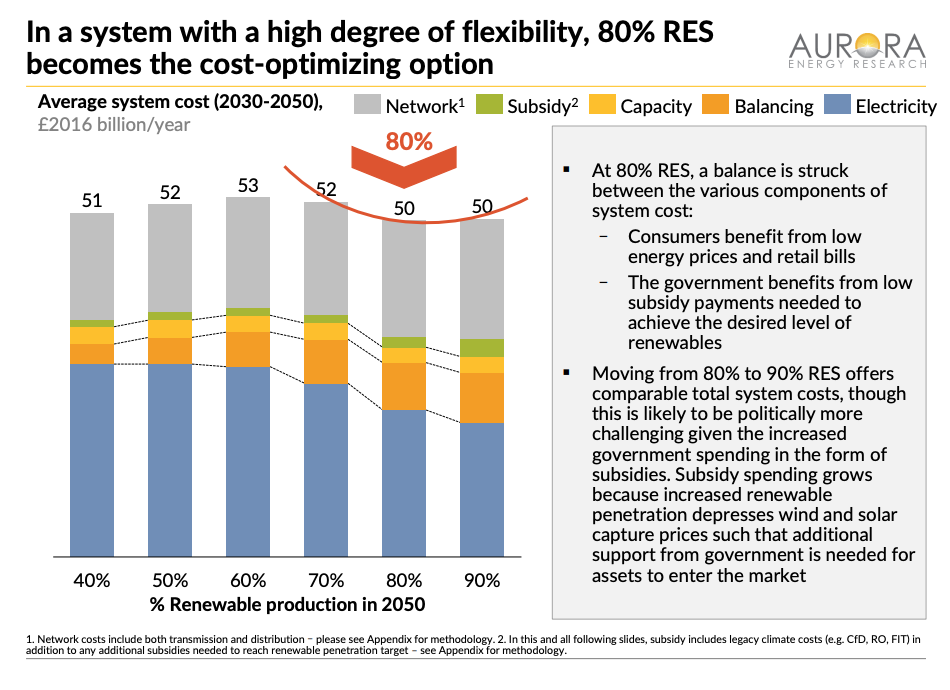

Third, there is the modelling for the National Infrastructure Commission (NIC) carried out by Aurora Energy Research and also published in summer 2018. Aurora finds that a highly renewable system in 2050 (right-hand columns, below) would have similar overall costs to a highly nuclear one (left).

Average electricity system costs 2030-2050 in scenarios meeting UK climate goals. Reading from left to right, the columns show overall system costs (£bn/year) with an electricity mix that is 40-90% renewable. At lower renewable shares the remainder is supplied by nuclear and, to a lesser extent, imported electricity. Source: Aurora Energy Research for the National Infrastructure Commission.

Aurora’s work includes hourly balancing of modelled supply and demand. It formed the basis for the NIC recommendation that the UK contract for no more than one extra nuclear plant before 2025, in addition to the Hinkley C scheme.

However, its findings come with a number of caveats. The most important is that the modelling assumes a highly flexible electricity system, with plenty of interconnectors to other countries, smart charging of electric vehicles, demand-side response and batteries. Aurora explains:

“In a flexible system, reaching 70-80% renewable production by 2050 is the cost-optimising option, with no new nuclear beyond Hinkley Point C needed to meet carbon targets. In a less flexible system, more than 40% renewable production by 2050 increases the cost to consumers.”

Aurora also cautions that a 90% renewable mix “may be more vulnerable to extreme winter system stress events”. For example, a prolonged windless cold snap. [The “Beast from the East” in March 2018 was cold, but windy.] Such a system would be reliant on imports during stress events, but supplies could also be tight in exporting countries, due to internationally correlated weather.

Another point to note with the Aurora modelling is that it allows for net electricity imports to the UK in 2050, whereas the CCC assumes demand is met purely from domestic resources.

This spring, the CCC will publish its advice on raising the UK’s long-term climate goals in line with Paris. This advice is expected to include pathways to reaching the higher targets.

How has the media responded?

The news of Hitachi’s Wylfa decision sparked a series of newspaper editorials and opinion pieces.

“New nuclear plants may not be worth the cost,” says the Financial Times leader, adding that the decision “all but sounds the death knell for the UK’s 2013 energy strategy”. It says:

“Hitachi’s decision…should prompt the government to re-examine whether nuclear power is needed and if so whether the inevitable cost to taxpayers is justifiable. A comprehensive, independent and strategic review of energy policy should establish whether the case for nuclear power – based on the intermittency of renewables and the need for a zero carbon base load – survives these recent project failures.”

The FT says this review should also consider the falling cost of renewables and should look for “better incentives”. It adds that more direct government investment in new nuclear might be a “sensible” alternative to Chinese funding, given “legitimate security concerns”.

For the Times editorial, the news leaves the UK with a “headache”. It adds: “Pressing ahead without new nuclear capacity is plausible, but not without a considerable expansion of renewable energy and its storage capabilities.”

The Guardian editorial says current UK energy policies “don’t add up”. It says: “The challenge for all those in the UK who see this as good rather than inconvenient news – because cheap, green energy that doesn’t create toxic waste is what the planet needs – is to explain how demand will be met when existing nuclear power stations have been wound down, at times when there is no sun or wind, until we have the technology we need to store electricity.”

The Daily Mail editorial calls the Wylfa news “deeply worrying”, noting nuclear plants supply a fifth of UK electricity, yet will mostly retire by 2025. “With coal being phased out, no new gas-fired stations under way and fracking unpopular, how on earth will [government] fill this vast energy shortfall,” it asks, saying the UK could become “dangerously dependent” on nuclear built by China or gas from Russia. [The UK currently gets much less than 1% of its gas directly from Russia.]

The Observer editorial says the news leaves the UK’s energy policy “in ruins”. It says: “The nation needs to know, very quickly, how ministers intend to make up for this lost capacity.” Despite higher costs than renewables, the Observer says: “[Government] need[s] to reopen talks with Hitachi and Toshiba to hammer out a sensible electricity pricing mechanism for power from their plants and so allow building work to resume.” It also calls for more investment in renewables and CCS.

Is there another way to fund new nuclear?

The Wylfa deal collapsed despite a “significant and generous” package of support being offered by government, according to Clark. In a sign of the lack of investor appetite for the deal, Hitachi’s shares jumped 13% on news the project was being shelved, according to Reuters.

The package on offer included a fixed price of up to £75 per megawatt hour (MWh) for Wylfa’s electricity under the Contracts for Difference (CfD) scheme for low-carbon power. It also included the government taking a one-third stake in the project and providing all necessary debt finance.

The key problem with the deal appears to have been the fact that Hitachi would have assumed essentially all of the risk related to building the Wylfa plant on time and to budget. It would not have received any payments until the plant started to operate. Indeed, this was a central selling point of the CfD deal secured for Hinkley C, according to then-secretary of state Ed Davey.

[Some commentators have argued that government preoccupation with Brexit is also putting off potential investors, with Nick Butler in the Financial Times writing: “International business has begun to distrust the UK as a place to invest.”]

In 2017, the National Audit Office (NAO) criticised the Hinkley deal and argued that government taking on a share of construction risk could have resulted in a lower price for consumers:

“Alternative financing models would have exposed consumers and/or taxpayers to the risks of the project running over budget…But our analysis suggests alternative approaches could have reduced the total project cost. The department did not assess whether the reduced cost balanced against the increased exposure to risk would have resulted in better value for money for electricity consumers.”

The NAO’s report explored alternative financing models, including versions of a “regulated asset base” deal (RAB). This model is already used to finance major infrastructure projects, including electricity transmission lines or London’s “supersewer” under the Thames.

Put simply, RAB would see the owners of a new asset (the new nuclear plant) being paid a regulated return on their investment. Crucially, payments would begin during the construction phase of the project, whereas CfDs only start once electricity is being generated.

The government has been exploring RAB for new nuclear since mid-2018 and has the chief financial officer of the supersewer advising it on the matter. The idea has prominent supporters, including Prof Dieter Helm, author of a recent report for government on the costs of energy.

Two new nuclear reactors at the Vogtle plant in Georgia, US, are being built under a RAB. However, the project has been in financial difficulty as a result of cost overruns and delays.

Interestingly, the then-Department of Energy and Climate Change (DECC) considered, but rejected a RAB model for new nuclear in 2011. At the time, DECC said the idea would “transfer construction risk, which generators are better suited to manage, to the consumer” and called it “high risk”.

Blast from past re latest UK govt plan to finance nuclear via a “regulated asset base” model…

…back in 2011 the, er, UK govt said RAB “not attractive”:

* construction risk on consumer

* “sacrifice mkt benefits”

* “radical change…high risk”https://t.co/HkD6nPKX3b pic.twitter.com/KlxANW4z5A— Simon Evans (@DrSimEvans) November 22, 2018