In-depth Q&A: The IPCC’s sixth assessment on how to tackle climate change

Multiple Authors

04.05.22Limiting global warming to 1.5C or 2C would mean “rapid and deep” emissions reductions in “all sectors” of the global economy, says the latest report from the United Nations’ Intergovernmental Panel on Climate Change (IPCC).

Instead, emissions have continued to rise – albeit at a slowing rate – and it will be “impossible” to stay below 1.5C with “no or limited overshoot” without stronger climate action this decade, says the new document, which forms part of the IPCC’s sixth assessment report (AR6).

-

WG1

- In-depth Q&A: The IPCC’s sixth assessment report on climate science

- Scientists react: What are the key new insights from the IPCC’s WG1 report? WG2

- In-depth Q&A: The IPCC’s sixth assessment on how climate change impacts the world

- Scientists react: What are the key new insights from the IPCC’s WG2 report? WG3

- In-depth Q&A: The IPCC’s sixth assessment on how to tackle climate change

- Scientists react: What are the key new insights from the IPCC’s WG3 report?

It outlines how these emissions cuts could be achieved, including “substantial” reductions in fossil fuel use, energy efficiency, electrification, the rapid uptake of low-emission energy sources – particularly renewables – and the use of alternative energy carriers, such as hydrogen.

Over the past decade, rapid cost reductions in key technologies – such as wind, solar and batteries – mean that continuing to use high-carbon energy may be “more expensive” than the alternatives, the report says. Overall, the economy would benefit from limiting global warming, it adds.

Alongside rapid emissions reductions, the report says that carbon dioxide removal (CDR) will be “unavoidable” to reach net-zero. For the first time, it devotes a chapter to the “demand-side”, including diets and consumption patterns. Early action and demand-side solutions can minimise the need for CDR and give more time to bring CO2 emissions to net-zero, it says.

The report follows the publication of the first part of AR6, released in August last year, which set out how and why the Earth’s climate is changing. The second part of AR6, released in February, laid out the impacts of climate change and said the threat being posed to humans and the planet was “unequivocal”.

Over the past two weeks, government delegations have been meeting during a two-week approval session to agree on the high-level “summary for policymakers”. The approval session was the longest ever, spanning more than 150 hours of virtual meetings, as countries struggled to find consensus on some of the language in the report.

The report tracks current efforts to tackle climate change – and what would be needed to limit warming to 1.5C or well-below 2C above pre-industrial temperatures. Its key conclusions include:

- “Global net anthropogenic [greenhouse gas] GHG emissions during the decade (2010-19) were higher than any previous time in human history (high confidence).”

- Although at least 90% of global GHG emissions are covered by climate targets, only 53% are covered by “direct” climate laws.

- Following current climate pledges to 2030 would make it “impossible” to limit warming to 1.5C with “no or limited overshoot” – and “strongly increas[e] the challenge” for 2C.

- “The global economic benefit of limiting warming to 2C is reported to exceed the cost of mitigation in most of the assessed literature (medium confidence).”

- In pathways limiting warming to 1.5C with no or limited overshoot, global CO2 emissions peak “at the latest before 2025” and then fall to 48% below 2019 levels in 2030, reaching net-zero by the “early 2050s”. Global GHGs fall 43% by 2030 and 84% by 2050.

- All scenarios limiting warming to 2C or below include “greatly reduced” fossil fuel use, with unabated coal being “completely” phased out by 2050.

- “The deployment of carbon dioxide removal (CDR) to counterbalance hard-to-abate residual emissions is unavoidable if net-zero CO2 or GHG emissions are to be achieved.”

- Accelerated climate action is “critical” to achieving sustainable development.

In a video message at the launch of the report, UN secretary-general António Guterres said it was a “file of shame, cataloguing the empty pledges that put us firmly on track towards an unlivable world”. He added:

“Climate activists are sometimes depicted as dangerous radicals. But the truly dangerous radicals are the countries that are increasing the production of fossil fuels…[The report] sets out viable, financially sound options [for cutting emissions] in every sector that can keep the possibility of limiting warming to 1.5C alive.”

In the in-depth Q&A below, Carbon Brief unpacks the key findings of the report. Please use the links to navigate between the sections.

- What is the Working Group III report?

- How have global emissions been changing?

- How do current policies and pledges compare to scenarios assessed by the IPCC?

- What would it take to limit warming to 1.5 or 2C?

- How can shifting peoples’ demand for products and services cut emissions?

- What impact can the food system and dietary choices have on emissions?

- How must global energy systems change to limit warming?

- How does land add to climate change and how can it help soak up CO2?

- What does the report say about CO2 removal and solar geoengineering?

- What role can cities and buildings play in cutting emissions?

- What needs to happen in the transport sector to cut CO2?

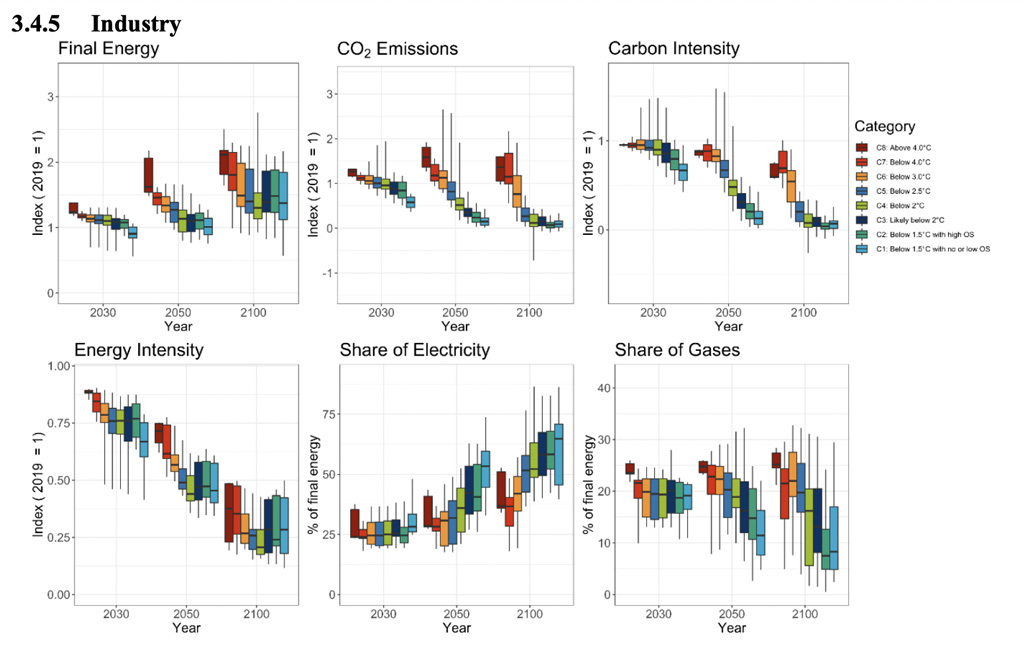

- How can industry be decarbonised?

- What climate policies are being implemented and are they working?

- Are the Paris Agreement and climate finance helping cut emissions?

- What are the costs and benefits of efforts to cut emissions?

- How much innovation and new technology is needed to hit climate goals?

- Will meeting climate goals help or hinder sustainable development?

1. What is the Working Group III report?

The new report is the third part of the IPCC’s latest assessment cycle – the sixth set of “assessment reports” since its foundation in 1988. The previous set – the fifth assessment report (“AR5”) – was published in 2013-14. (See Carbon Brief’s coverage here.)

The IPCC’s efforts for AR6 are divided into three “working groups”:

- Working Group I (WG1): The physical science basis

- Working Group II (WG2): Impacts, adaptation and vulnerability

- Working Group III (WG3): Mitigation of climate change

Back in September 2017, the IPCC agreed outlines for all three working groups. And, in April 2018, the IPCC announced the authors who had been selected – more than 700 in total, who all work on a voluntary basis.

The WG3 report is the third of these to be published, following the WG1 report in August 2021 and the WG2 report in February this year. The final part will be a synthesis report, which is slated for September.

In addition to the full assessment reports, the IPCC’s sixth assessment cycle has also included shorter “special reports” on three topics:

- Global warming of 1.5C (“SR15”) in 2018

- Climate change and land (“SRCCL”) in 2019

- The ocean and cryosphere in a changing climate (“SROCC”) in 2019

(In addition, the IPCC has published a 2019 “methodology report” on guidelines for national greenhouse gas [GHG] inventories.)

A key message from these reports “is the urgency to mitigate GHG emissions in order to avoid rapid and potentially irreversible changes in natural and human systems”, the new report says.

-

WG1

- Media reaction: IPCC’s new climate science report and what it means for the world

- Analysis: What the new IPCC report says about when world may pass 1.5C and 2C

- Explainer: What the new IPCC report says about extreme weather and climate change

- IPCC: How the AR6 WG1 summary for policymakers compares to its predecessor WG3

- Analysis: What the new IPCC report says about how to limit warming to 1.5C or 2C

- Guest post: How not to interpret the emissions scenarios in the IPCC report

- Guest post: Why estimates of the ‘cost’ of climate action are overly pessimistic

For WG3 specifically, the aim is to assess “the current state of knowledge on the scientific, technological, environmental, economic and social aspects of climate change mitigation”. It takes into account “new literature, methodological and recent developments, and changes in approaches towards climate change mitigation since the IPCC AR5 report was published in 2014”.

The “global science and policy landscape on climate change mitigation has evolved since AR5”, the report notes. In particular, the Paris Agreement and the UN Sustainable Development Goals (SDGs) have been adopted globally, the authors note, which have “set out a globally agreed agenda within which climate mitigation efforts must be located”.

At the same time, climate mitigation policies around the world “have grown in both number and shape”, the authors say, and the “average rate of annual increase of CO2 emissions has declined”.

However, “GHG emissions globally continued to rise, underlining the urgency of the mitigation challenge”, the authors note.

In addition, “strong differences remain” between which countries have the responsibility and capability to take climate action, they add:

“These differences, as well as differences in the impact of climate change, point to the role of collective action in achieving urgent and ambitious global climate mitigation in the context of sustainable development, with attention to issues of equity and fairness as highlighted in several chapters of the report.”

Over the course of the report-writing process, three drafts have been reviewed by numerous experts and governments, and the authors have addressed almost 60,000 comments.

With the main report complete, the final step has been a line-by-line agreement of the short summary for policymakers (SPM) document by government delegates. This approval meeting has been carried out virtually over the past two weeks, although it overran into the final weekend, pushing the report’s publication back by six hours.

This was the longest #IPCC approval Plenary in the 34-year long history of @IPCC_CH. Due to end on April 1st (probably a bad date😉), it will formally end on April 4. The world will have to wait a little more than expected to read it but it will be another landmark #ClimateReport

— Prof. Jean-Pascal van Ypersele (@JPvanYpersele) April 3, 2022

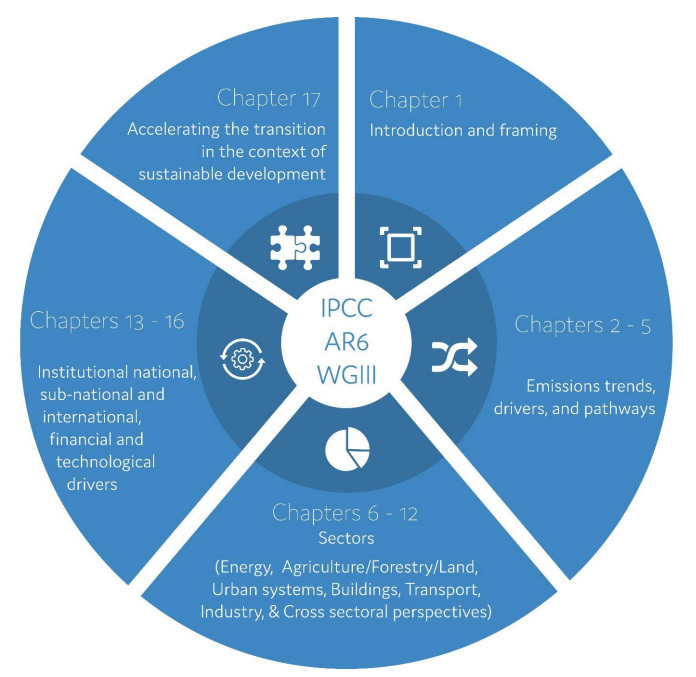

The final report is made up of 17 chapters, which are divided into five main parts (see figure below):

- Introduction and frameworks;

- Emission trends, scenarios and pathways;

- Sectors;

- Institutional dimensions including national and international policy, financial and technological mitigation drivers; and

- Conclusions.

It also comes with a summary for policymakers (SPM), technical summary and various annexes. While the WG1 and WG2 reports clocked in at more than 3,000 pages, the WG3 comes in just below this figure.

For the first time, the WG3 report includes “chapters dedicated to cross-sectoral perspectives, demand, services and social aspects of mitigation and innovation, technology development and transfer”, the authors say. It also gives “greater attention than AR5 to social, economic and environmental dimensions of mitigation actions, and institutional, legal and financial aspects”.

The report describes collaboration with the other IPCC working groups, which is reflected in a series of “cross-working group boxes”. These cover topics such as the economic benefits from avoided impacts as a result of mitigation, climate change and urban areas, mitigation and adaptation through the “bioeconomy”, and solar radiation modification.

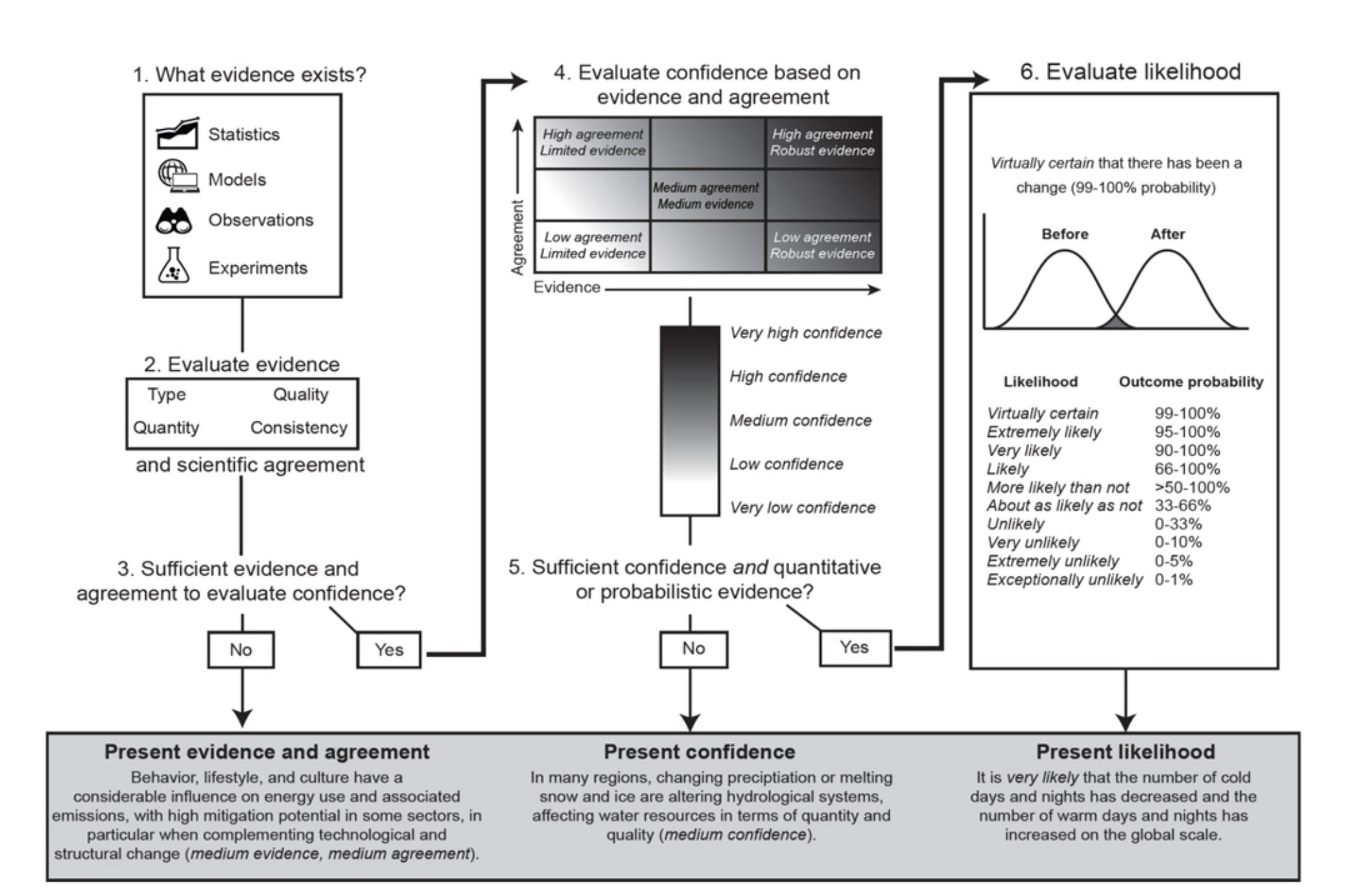

The WG3 report follows the same set of “calibrated language” that AR5 used to communicate levels of certainty behind the statements it included.

These terms fall into two categories. The first is “confidence”, which reflects the authors’ qualitative judgements on the soundness of a particular finding or statement. The second is “likelihood”, which is used when the uncertainties around a statement can be quantified. These sorts of probabilistic judgments can be based on methods such as statistical analysis or expert judgments.

These statements of confidence and likelihood – shown in the figure from the WG2 report below – are presented in italics in the report and in this article, too.

For example, the technical summary of the report says – with high confidence – that “global net anthropogenic GHG emissions during the decade (2010-19) were higher than any previous time in human history”.

Meanwhile, it adds with medium confidence that “the lifestyle consumption emissions of the middle income and poorest citizens in emerging economies are between 5-50 times below their counterparts in high-income countries”.

2. How have global emissions been changing?

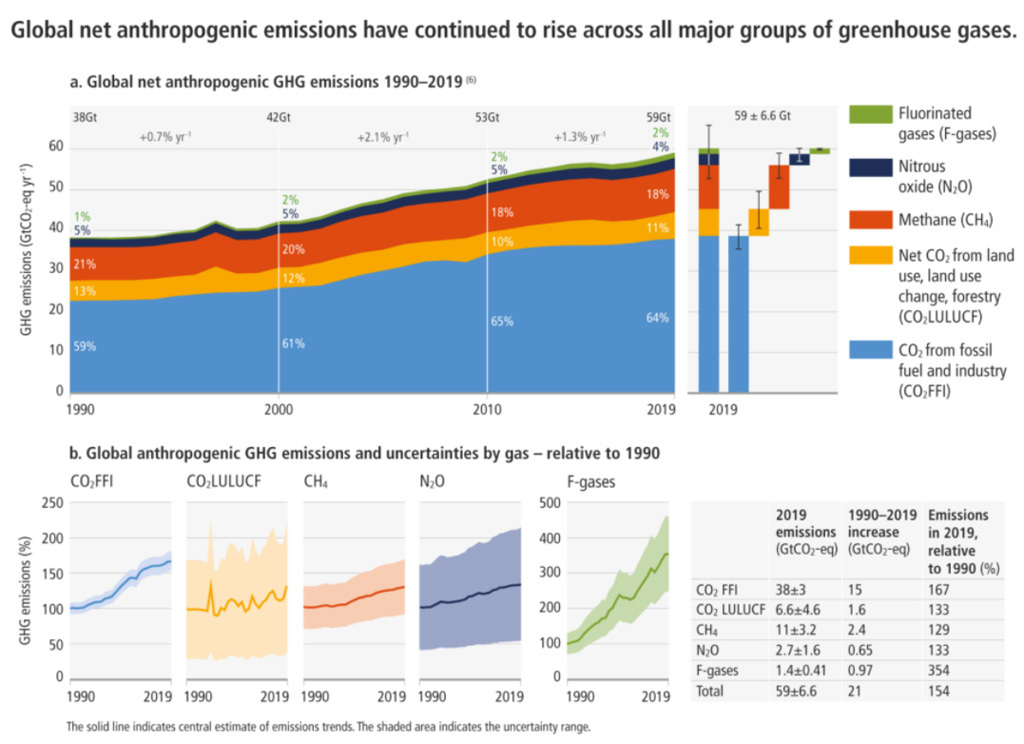

During the decade spanning 2010-9, human-driven emissions of greenhouse gases (GHGs) “were higher than at any previous time in human history”, the report states with high confidence.

In 2019, humanity emitted 59.6bn tonnes of carbon dioxide equivalent (GtCO2e) with a range of uncertainty of ±6.6GtCO2e. There is medium confidence that the net CO2 emissions over the past decade are “about the same size as the remaining carbon budget for keeping warming to 1.5C”, meaning another decade of similar emissions would use this budget up.

The growth in emissions has “varied, but persisted” for all GHGs during the past decade. However, there is also high confidence that the annual growth rate over this decade was lower than it was in the prior one – 1.3% per year for 2010-9, as compared to 2.1% per year for 2000-9.

The chart below shows the growth of the four GHGs (or classes of GHGs) that are tracked in the report between 1990-2019, as well as the changes in their relative contributions to the overall emissions (CO2 is divided into emissions from fossil fuels and industry, FFI, and emissions from land use, land-use change and forestry, or LULUCF).

The chart also shows the level of CO2e emissions as calculated using the values that different IPCC reports estimated for GWP100 – the 100-year global warming potential used to standardise the emissions of different greenhouse gases into CO2e.

The major non-CO2 GHGs discussed in the report are methane, nitrous oxide and fluorinated gases – although this last category excludes chlorofluorocarbons and hydrofluorocarbons, which are covered by the Montreal Protocol, but not the Paris Agreement.

In 2019, methane emissions were 11±3.2GtCO2e, nitrous oxide emissions were 2.7±1.6GtCO2e and fluorinated gases were 1.4±0.41 GtCO2e.

Since 1990, methane emissions have grown by 29% and nitrous oxide emissions by 33%. Emissions of CO2 from fossil fuels and industry have grown by 67% over that same period.

Meanwhile, emissions of fluorinated gases have grown by 254% since 1990, but the report notes that this growth “occurred from low levels”. It adds that fluorinated gas emissions “are no longer negligible”.

One of the major uncertainties in calculating the world’s emissions is the contribution of LULUCF. These sectors “have shown little long-term change” and the uncertainties associated with measuring these emissions “preven[t] the detection of statistically significant trends”.

On average, the estimates of LULUCF emissions show a slight increase, but different estimates have diverging trends. For example, the Global Carbon Project last year reanalysed historical LULUCF emissions, finding they have been declining by an average of 25% over the past decade – resulting in effectively flat overall CO2 emissions over that time period, albeit with significant uncertainty.

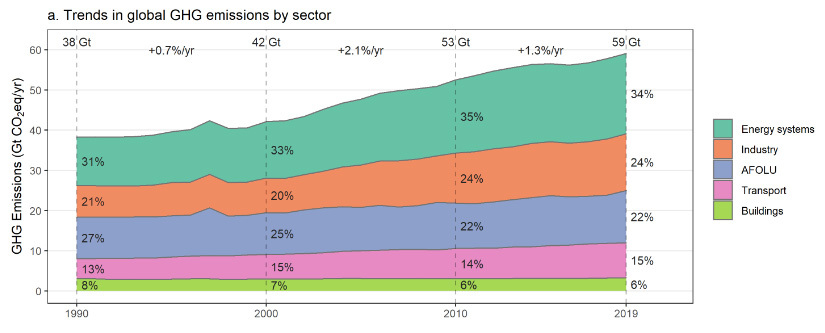

For the year 2019, about 20GtCO2e – or one-third of annual emissions – were attributable to the energy sector, while the direct emissions from industry contributed about one-quarter of the total, 14GtCO2e. The other major contributing sectors were agriculture, forestry and land use, known as AFOLU (13GtCO2e, or 22%), transport (8.7GtCO2e, or 15%) and buildings (3.3GtCO2e, or 6%). The category of AFOLU includes all CO2 emissions from LULUCF as well as non-CO2 emissions from agriculture, such as livestock emissions and those from fertiliser use.

When emissions from electricity and heat are added to direct emissions from various sectors, industry’s share climbs to 34% and that of buildings leaps to 16%.

The strongest drivers of increased emissions from fossil fuel combustion were increases in per-capita GDP and population growth, the report says, responsible for emissions gains of 2.3% and 1.2% per year, respectively.

Improved energy efficiency in certain sectors has led to some “decarbonisation gains”, with the energy needed to generate each unit of GDP falling by 2% per year. But these gains “have been largely wiped out by increases in demand for goods and services”.

Similarly, annual gains of 0.3% in the carbon intensity of the global economy – the emissions per unit of energy use – have been insufficient to offset rising demand.

There is high confidence that emissions rose “across all sectors and subsectors”, with transportation and industry showing the most rapid growth. Average annual growth in the transport sector was about 1.8% over the past decade, with direct emissions from industry growing annually by 1.4% and those from the energy sector by 1%.

The report notes that these patterns are “different to growth patterns observed in the previous decade”. Between 2000-9, annual growth in the transport sector was also about 1.8%, but over that time, industry grew annually by 3.4% and energy by 2.3%.

The charts below show global emissions by sector, as well as the overall emissions growth rate for each decade from 1990-2019. The lower panels show emissions in each sector divided among 10 world regions.

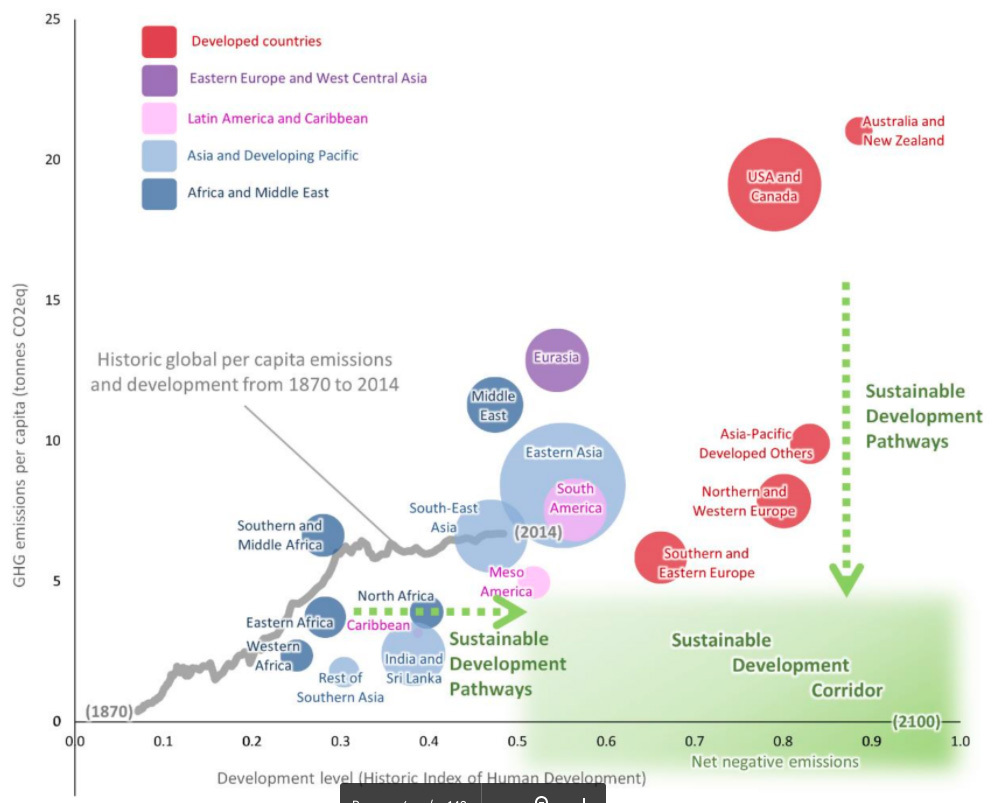

Total emissions, per-capita emissions and emissions trends all “diverge starkly” between countries and regions. So-called “developed countries” have “sustained high levels” of per-capita emissions – more than double the per-capita emissions of Asia and the Pacific, Africa or Latin America. The group of least-developed countries has the lowest emissions per capita and has “contributed only a negligible proportion of historic GHG emissions growth”.

Developed countries, on the whole, “have not managed to reduce GHG emissions substantially” over the past several decades, the report states, while the bloc of “Asia and the Pacific” has “rapidly increased [its] share of global GHG emissions” since 1990, and “particularly since the 2000s”.

With the exception of eastern Europe and west-central Asia, emissions growth slowed “across all regions” of the world in 2010-9 as compared to 1990-2010. The slowing of global emissions growth “was primarily triggered by substantial reductions” of emissions growth in China.

Emissions from fossil fuel combustion in the three “developing regions” of Asia and the Pacific, Africa and Latin America grew by 26% over the past decade, as compared to 260% growth in the prior two decades. The fossil fuel combustion emissions of developed countries shrank by about 10% over both of those periods.

However, emissions also vary widely with income level within a country. There is robust evidence and high agreement that the wealthiest 10% of people are responsible for 34-45% of consumption-based household emissions. The report notes that this 10% is found on all continents.

In countries that have succeeded in reducing their emissions, it has been a combination of “both climate and non-climate policies and factors, including structural changes” that have led to these decreases, the report finds. Most of the reductions occurred in the energy and heating sectors, while transportation emissions have continued to rise after peak emissions were reached “in many cases”.

Understanding how socioeconomic factors affect mitigation efforts is “crucial”, the report writes. It notes a “long-standing discussion” on decoupling – that is to say, if economic growth can be sustained without further growth in carbon emissions or use of natural resources. Some studies have found it “feasible” at the national level, while scepticism remains over “whether absolute decoupling can be achieved at a global scale”, the report adds.

The report cites a few examples of countries that have managed “absolute decoupling” of their consumption-based emissions from GDP growth over the first half of the decade – including the US, Cuba and some EU countries – but makes note of the “short observation period” over which this decoupling occurred.

It also calls for further research on how consumption-based drivers of emissions “can be mitigated by demand management, alternative economic models, population control and rapid technological transition”.

Between the indirect emissions of producing items and the direct emissions of energy and transportation associated with consumption, household consumption is both the largest component of a country’s GDP and the “main contributor to greenhouse gas emissions”. Consumption patterns and the associated emissions are affected by numerous factors, including socioeconomic status, access to public services and individual choice and values.

In “western countries”, the report says, transportation, housing and food consumption combined have the “largest contribution to the household carbon footprint”. In EU-25 countries, for example, these categories add up to 58.5% of the average household footprint. Meat-eating alone contributes 5.2% of the household footprint in the US.

Urban and rural households also have very different consumption patterns and emissions. Urban households “tend to have higher emissions” than their rural counterparts, but with different patterns – urban households have higher emissions associated with services such as education and entertainment, while rural households have higher transportation and food emissions.

One study cited in the report notes that urbanisation is associated with economic growth and therefore higher emissions. The report also states that “centrality and location” influence urban household emissions and that “higher population density is associated with lower per capita emissions”. It adds:

“Commuting distance and access to public transportation, recreation areas, city centres, public services and shops are other important neighbourhood-specific determinants of carbon emissions.”

The report also discusses emissions embodied in trade (EET) – those associated with producing goods exported from or imported into a country. An increase in trade volume over the past four decades has meant rising EET since the 1980s, with a peak in 2006.

As of 2014, about one-quarter of global emissions are “embodied in the international trade of goods and services”. Developed countries are a major net importer of CO2 emissions, while Asia and the Pacific is the largest net exporter.

Notably, the report states with high confidence that since the peak in 2006, there has been a net reduction in traded CO2 – and in the transfer of embodied carbon from developing to developed countries – as the falling carbon intensity of traded goods has offset higher trade volumes.

3. How do current policies and pledges compare to scenarios assessed by the IPCC?

WG3 draws on a database of more than 3,000 different future emissions pathways. They are primarily generated by integrated assessment models (IAMs) that examine energy technologies, energy use choices, land-use changes and societal trends that cause – or prevent – greenhouse gas emissions. (For more details on how IAMs work, see Carbon Brief’s detailed Q&A).

These scenarios are broadly divided into eight different “climate categories”, labelled C1 through to C8, based on 21st century warming. These assignments are based on the use of climate model emulators called MAGICC and FaIR, as the IAMs do not calculate temperatures themselves.

In addition to the climate categories, seven illustrative pathways (IPs) were defined representing outcomes under policies in place today (Cur-Pol), outcomes if 2030 commitments are met but limited additional climate policies are enacted (Mod-Act), and five deep mitigation strategies that limit warming to below 2C or to 1.5C using different types of approach.

The table below shows a number of key characteristics of each climate category C1-C8 and the relationship between these categories and the illustrative pathways. For each category, it highlights the median value across all relevant model pathways, as well as the range (5th to 95th percentile) across all models in each category in brackets. (More details can be found in Table SPM.1 of the report.)

| Category | Description | IPs | Scenarios | Cumulative CO2 | Peak warming | 2100 Warming | Peak CO2 emissions year | Net-zero CO2 year | Cumulative net-negative emissions |

|---|---|---|---|---|---|---|---|---|---|

| C1 | Below 1.5C with no or limited overshoot | SD, LD, Ren | 97 | 320 (-210 to 570) | 1.6 (1.4 to 1.6) | 1.3 (1.1 to 1.5) | 2020-2025 (all < 2025) | 2050-2055 (2035-2070) | -220 (-660 to -20) |

| C2 | Below 1.5C with high overshoot | Neg | 133 | 400 (-90 to 620) | 1.7 (1.5 to 1.8) | 1.4 (1.2 to 1.5) | 2020-2025 (all < 2030) | 2055-2060 (2045-2070) | -360 (-680 to -60) |

| C3 | Likely below 2C | GS | 311 | 800 (510 to 1,140) | 1.7 (1.6 to 1.8) | 1.6 (1.5 to 1.8) | 2020-2025 (all < 2030) | 2070-2075 (2055 to after 2100) | -40 (-290 to 0) |

| C4 | Below 2C | 159 | 1,160 (700 to 1,490) | 1.9 (1.7 to 2.0) | 1.8 (1.5 to 2.0) | 2020-2025 (all < 2030) | 2080-2085(2065 to after 2100) | -30 (-280 to 0) | |

| C5 | Below 2.5C | 212 | 1,780 (1,260 to 2,360) | 2.2 (1.9 to 2.5) | 2.1 (1.9 to 2.5) | 2020-2025 (all < 2030) | 0 (-160 to 0) | ||

| C6 | Below 3C | Mod-Act | 97 | 2,790 (2,440 to 3,520) | 2.7 (2.4 to 2.9) | 2030-2035 (all < 2090) | 0 | ||

| C7 | Below 4C | Cur-Pol | 164 | 4,220 (3,160 to 5,000) | 3.5 (2.8 to 3.9) | 2085-2090 (some > 2100) | 0 | ||

| C8 | Above 4C | 29 | 5,600 (4,910 to 7,450) | 4.2 (3.7 to 5.0) | 2080-2085 (some > 2100) | 0 |

The Cur-Pol pathway, where current policies are continued, turns out to be tricky to categorise. The scenario ends up with a best-estimate warming of almost precisely 3C in 2100, making it overlap with both the 2.5C-3C (C6) and 3C-4C (C7) categories, either on the high end of the former or the low end of the latter.

More broadly, as WG3 lead author Prof Detlef van Vuuren tells Carbon Brief, current policy scenarios assessed by WG3 range from 2.2C to 3.5C in 2100, “consistent with the C5-C7 categories”.

WG3 provides a look at possible futures which is informed by progress that the world has made in enacting climate policies and making clean energy cheaper. Rather than wind back the clock to imagine a world without any climate policy, the scenarios considered are increasingly incorporating implemented climate policies.

The WG3 authors suggest that no-climate-policy reference scenarios can be an important tool for assessing mitigation costs, but that “as countries move forward with climate policies of varying stringency, no-climate-policy baselines are becoming increasingly hypothetical”.

However, the range of outcomes under current policies still pose significant risks to human and natural systems. Climate system uncertainties are large enough that it is difficult to fully rule out warming above 4C in the absence of stronger future climate policy. The report makes it clear that a failure to peak and reduce emissions this decade will put Paris goals increasingly “out of reach”.

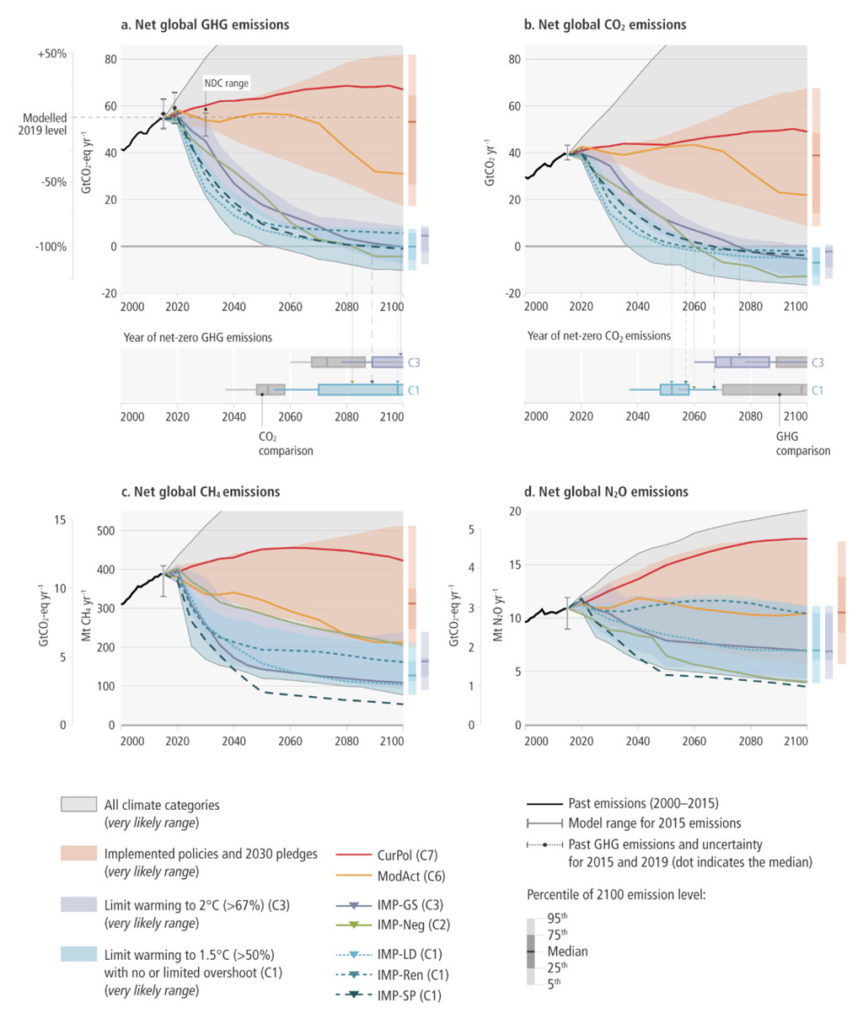

The figure below shows both CO2 emissions (left) and total greenhouse gas emissions (right) for the illustrative pathways (coloured lines), as well as the broader range of current policy scenarios (grey wedge), C3 (orange wedge) and C1 (green) scenarios.

The current policy scenarios assessed in the AR6 WG3 (including Cur-Pol) imply a relative flattening of emissions in the future compared to the growth over the past few decades, with CO2 emissions in 2100 anywhere between 25% below and 33% above current levels.

However, current policies represent something of a moving target and older modelling exercises may not capture commitments made in the lead-up to or at the COP26 conference, for example.

In addition to the scenarios in the WG3 database, the report cites two recent reviews of current policy scenarios. The first, by Sognnaes et al, finds that current policies would see warming reach a median level of between 2.2C and 2.9C. The second, by Höhne et al, finds a range of 2.2C to 3.2C; however the upper end of this range came from the 2020 UNEP Emissions Gap Report, which was revised downward in its 2021 version to a range of 2.1C to 3C.

These ranges suggest that there are “deep uncertainties involved with modelling temperature outcomes of 2030 policies through to 2100”, making it difficult to precisely determine the likely warming outcomes implied by policies in place today, the report says.

Countries have made nationally determined contribution (NDC) commitments for 2030 under the Paris Agreement that go beyond policies in place today, creating what the report refers to as an “implementation gap”.

Implementing these commitments – in the absence of strong future mitigation later in the century – would likely result in warming of around 2.4C, based on commitments up to and including COP26, or around 2.7C in the Mod-Act illustrative pathway in WG3.

The report says there is also an “emissions gap” of 19-26GtCO2e per year by 2030, between the 2030 NDCs and a scenario consistent with limiting warming to 1.5C with no or limited overshoot.

In effect, if NDCs are not strengthened the world will likely overshoot 1.5C by between 0.15C and 0.3C, the report explains, requiring a heavy reliance on net-negative CO2 emissions via carbon dioxide removal (CDR) later in the century to bring temperatures back down below 1.5C by 2100. It states with high confidence:

“[F]ollowing current NDCs until 2030…[would make] it impossible to limit warming to 1.5C with no or limited overshoot and strongly increas[e] the challenge to likely limit warming to 2C.”

Even limiting warming to 2C becomes difficult in this scenario, as it would imply a rate of emissions reductions after 2030 that is a full 70% higher than scenarios that assume immediate action to reduce emissions, the report says.

The emissions gap between 2030 NDCs and scenarios that likely limit warming to 2C is assessed to be between 10 and 16GtCO2e in 2030. Without strengthening, the NDCs risk “lock-in into carbon-intensive infrastructure and increased risk of stranded fossil fuel assets” that would “exacerbate the socio-economic strain of implementing the transition, leading to an increased risk of overshooting the warming and a higher risk of climate change impacts”.

The past few years have seen a proliferation of longer-term pledges by countries to reach net-zero CO2 or GHG emissions in the latter half of the 21st century. Promises from 77 countries now cover at least 76% of global greenhouse gas emissions.

The report suggests that the literature on these commitments is still developing and it is unclear what their aggregate effect would be – presuming that they are all met. A number of studies were released after the WG3 literature cutoff date (the date at which studies had to be published to be included in the report), suggesting these long-term net-zero commitments could limit global temperatures to below 2C by 2100 – though researchers warned these should be discounted until reflected in near-term pledges.

4. What would it take to limit warming to 1.5 or 2C?

The WG3 report assesses a wide range of scenarios associated with 1.5C (C1 and C2) and 2C (C3 and C4) outcomes. The lowest of these scenarios (C1), where warming is limited to 1.5C with no or limited overshoot, has become notably more difficult to achieve since the IPCC special report on 1.5C was published in 2018, due to four years of flat or modestly increasing global emissions. These scenarios are now associated with higher peak warming in most models, leading to a lower likelihood of limiting warming to 1.5C, the WG3 report says.

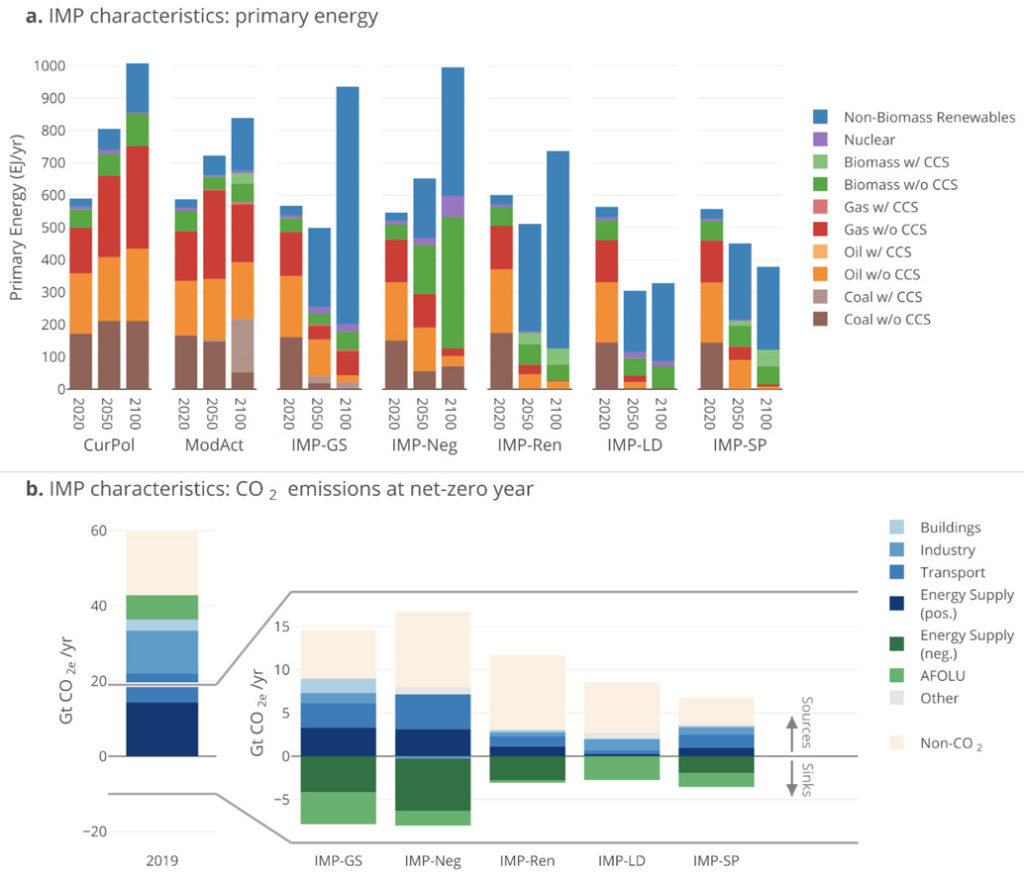

The report features five different illustrative mitigation pathways that explore different ways the world might limit warming to 1.5C or below 2C – in addition to the Mod-Act and Cur-Pol pathways discussed above.

Three of the illustrative pathways – “shifting development pathways” (SP), low demand (LD) and high renewables (Ren) – produce climate outcomes that limit warming to 1.5C with “no or limited overshoot” (C1).

A pathway featuring extensive use of net-negative emissions (Neg) results in warming below 1.5C in 2100, but with “high overshoot” during the 21st century (C2), while a pathway characterised by a gradual strengthening of current policies (GS) likely (>66% chance) limits warming to below 2C by 2100 (C3). The Mod-Act pathway – in which countries meet their 2030 commitments, but with little additional climate action – likely results in warming of between 2.5C and 3C by 2100 (C6).

Although the report outlines various ways to limit warming to 1.5C by 2100 (C1-C2), all of these pathways show deep emissions reductions over the next few decades, with both global CO2 and all GHG emissions peaking “between 2020 and at the latest before 2025” and CO2 emissions declining between 25% (Neg) and >50% (LD) by 2030 relative to 2020 levels.

Overall, in scenarios staying below 1.5C with no or limited overshoot, global GHG emissions fall to 43% below 2019 levels by 2030 and 84% by 2050. In these scenarios, global CO2 falls 48% by 2030 and to net-zero “in the early 2050s”, says the report. Methane emissions fall 34% by 2030.

The more intermediate GS pathway, which likely limits warming to 2C but not 1.5C, has global emissions declining by around 14% by 2030 relative to 2020 levels. More broadly, it says keeping warming below 2C means cutting CO2 emissions 50% “in the 2040s” and to net-zero “around the early 2070s”.

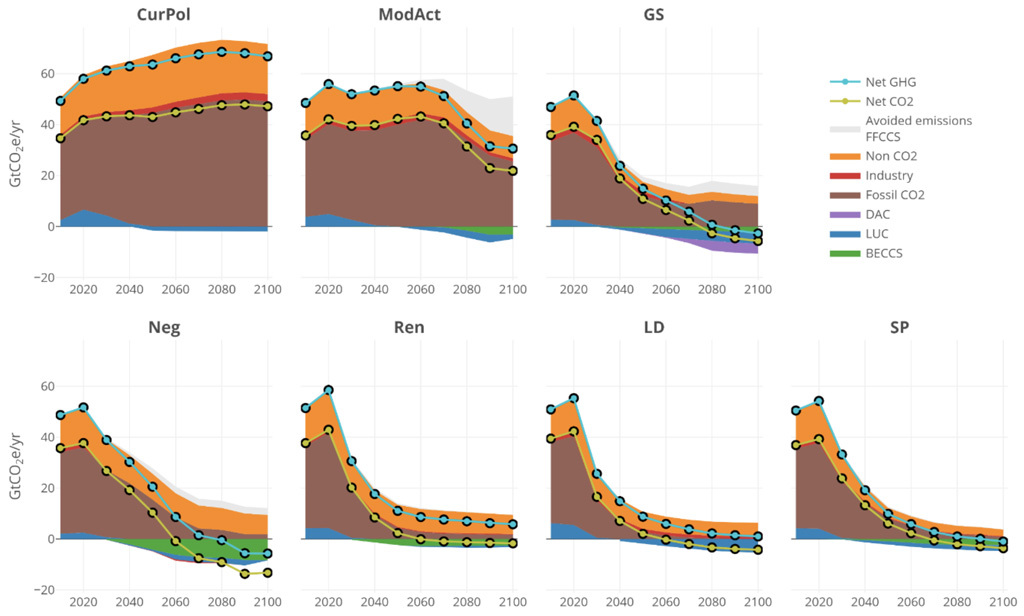

Each of the five mitigation-focused illustrative pathways has a somewhat different approach to cutting emissions, energy use and energy production. GS has a relatively slow phase-out of fossil fuels compared to the others, with high future energy demand primarily met by renewables and a fair amount of CDR deployed late in the century – including lots of direct air capture.

Neg relies heavily on biomass and bioenergy with carbon capture and storage (BECCS) for CDR, and also has a relatively slow phase out of fossil fuels and high future energy demand. Ren has a rapid phaseout of fossil fuels, more moderate future energy demand that is primarily met by renewables, and more limited deployment of CDR.

Finally, LD and SP both have large reductions in future energy demand and rapid fossil fuel phaseouts, with LD including an even faster fossil fuel use exit with limited negative emissions other than land use change (LUC), while SP has more reliance on late-century CDR.

The figure below shows the amount of positive emissions (orange, red, and brown) and CDR (purple, blue, and green) over time in the illustrative pathways.

Each illustrative pathway and climate category has a range of possible climate outcomes, depending on two areas of uncertainty. First, the uncertainty in emissions across all scenarios in a climate category. Second, climate system uncertainties that depend on how sensitive the climate is to CO2 and other GHG emissions and how carbon cycle feedbacks might change as the Earth warms.

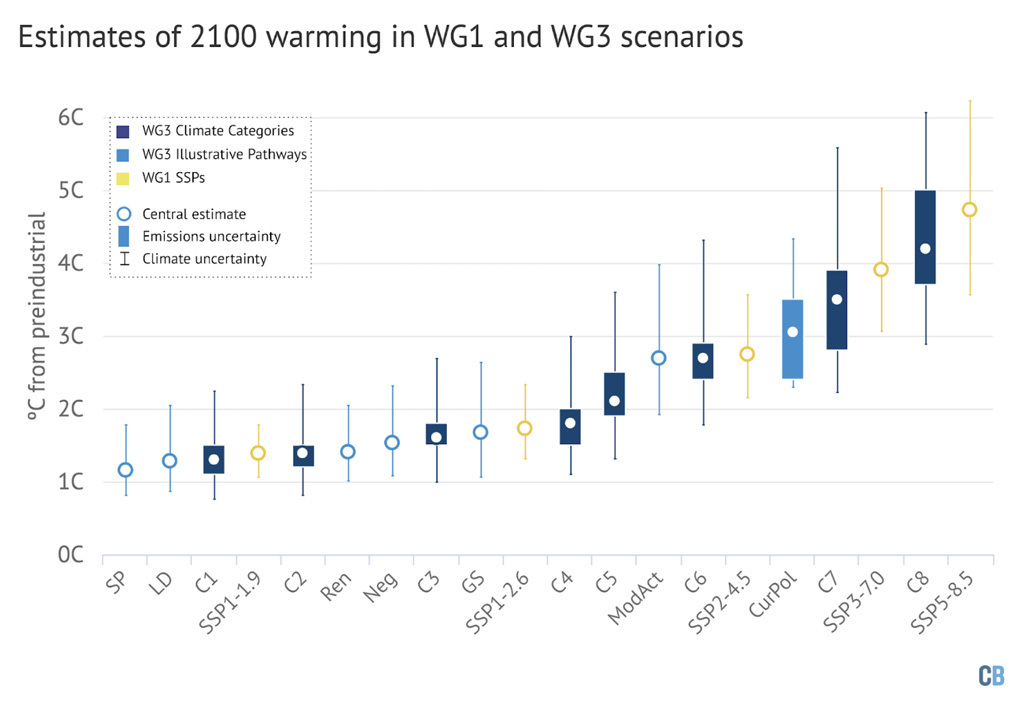

In addition to these new WG3 scenarios, the IPCC WG1 provided “assessed warming” estimates for five different future climate scenarios based on Shared Socioeconomic Pathways (SSPs). The SSPs reflect five specific emissions scenarios with differing end-of-century outcomes and are used by complex earth system models to simulate various aspects of the changing climate.

The WG3 scenarios, by contrast, explore a much wider variety of possible emissions futures, but are evaluated using simpler climate model emulators that only provide global average temperature changes.

The figure by Carbon Brief below provides a comparison between the possible amount of warming that may occur in the year 2100 under each of the different IP, climate category and SSP scenarios. The colour of the bar indicates the type of scenario (IP, climate category, or SSP), the dot gives a central warming estimate, the bars (when available) show the range of warming across different emissions scenarios in the category and the whiskers show the range of warming accounting for climate system uncertainties.

The climate categories and illustrative pathways provide a detailed look at a wide range of scenarios (SP to C4) that are “more likely than not” to limit warming to below 2C by 2100, similar to SSP1-1.9 and SSP1-2.6.

The report notes that while net-zero CO2 emissions are expected to lead to relatively flat temperatures, net-zero GHG emissions result in declining global temperatures.

In practice, pathways reaching net-zero GHGs tend to balance out residual non-CO2 GHG emissions with net-negative CO2 emissions. Net-zero CO2 emissions are generally reached by models around 10 to 40 years before net-zero GHG emissions, for those scenarios reaching net-zero GHGs in the 21st century.

While most scenarios that limit warming to well-below 2C (C1-C3) employ significant amounts of net-negative emissions, not all do. Scenarios with more immediate emissions reductions tend to have no or low overshoot and limit the amount of late-century CDR needed.

However, even in the most ambitious emission reduction scenarios (C1), most pathways still have a limited amount of overshoot, with the median model in that category having a 2 in 3 risk of overshooting 1.5C at some point in the 21st century.

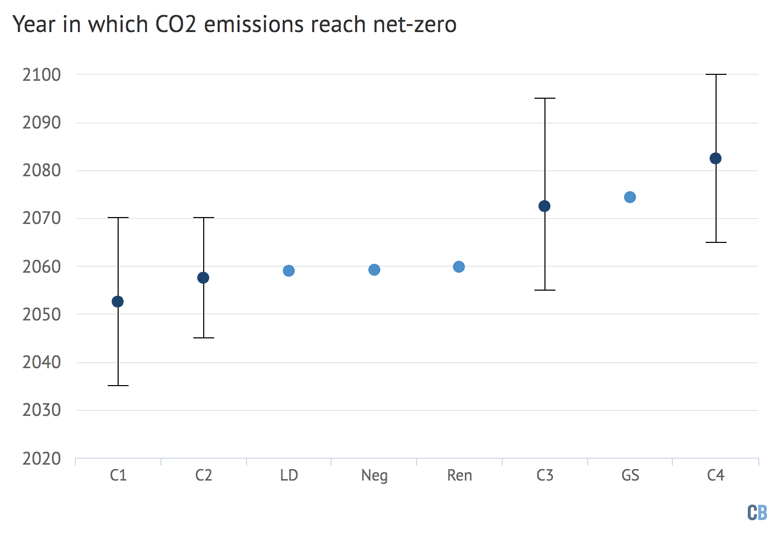

Pathways that limit warming to 1.5C with no or limited overshoot (C1) reach net-zero CO2 emissions “between 2050-2055” on average, with a range of between 2035 and 2070 across all the scenarios assessed.

C2 scenarios, on average, reach net-zero between 2055 and 2060 with a range from 2045 to 2070, while C3 scenarios reach net-zero “between 2070-2075” with a range of 2055 to 2100 or later. The median net-zero year and range across all the scenarios are shown for each climate category and illustrative pathway limiting warming to below 2C in the Carbon Brief chart below.

The fact that some of these models have a later net-zero emissions date does not imply that emissions reductions can be delayed, or that we “have more time to rapidly reduce current emissions levels compared to SR1.5”.

Rather, the scenarios with the latest peak year are often the ones with largest near-term emissions reductions, as they reserve more of the remaining carbon budget for later years.

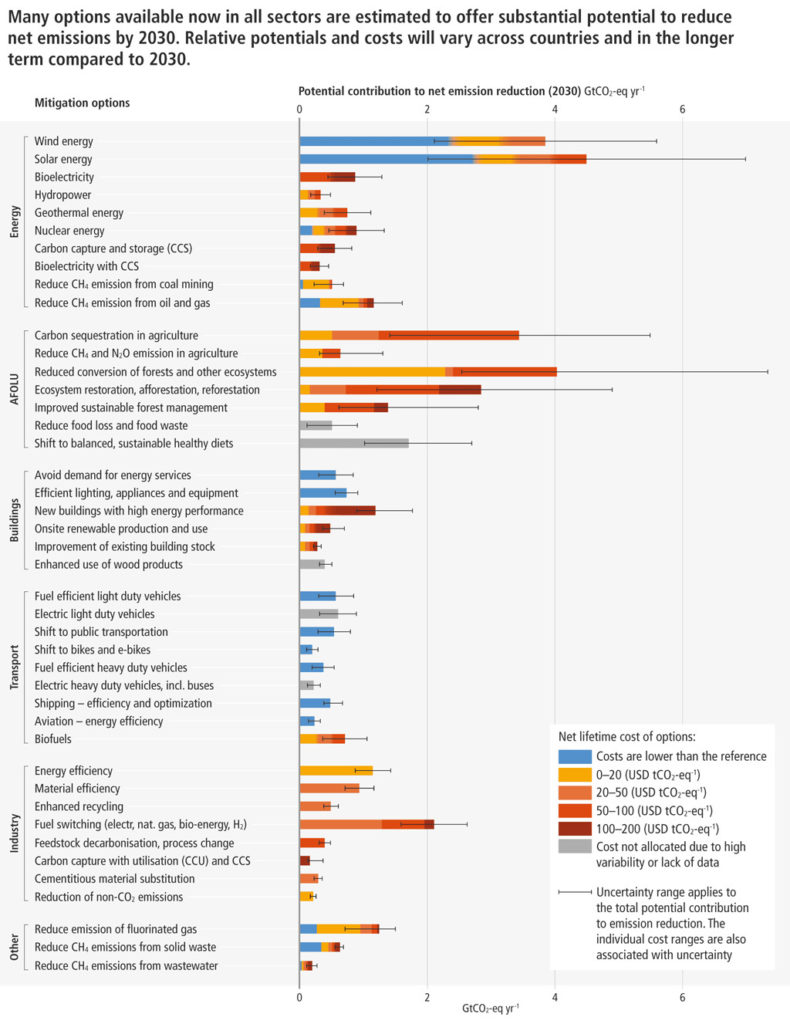

There are different mitigation strategies that can be employed to limit warming to well-below 2C, as shown by the illustrative pathways. Some have a heavy reliance on renewables (Ren), a strong emphasis on energy demand reductions (LD), wide-spread deployment of CDR (Neg), or focus mitigation in the context of sustainable development (SP).

In some scenarios, a small part of the energy system is still based on fossil fuels in 2100 (Neg), while, in others, fossil fuels are almost or completely phased out (Ren).

However, all mitigation pathways show “greatly reduced” fossil fuel use, with the three that limit warming to 1.5C with no or limited overshoot (Ren, LD, SP) unabated coal use “completely” phased out by 2050. While the GS and Neg scenarios rely heavily on CDR, its use is purposely restricted in the other illustrative pathways focused on deep mitigation (Ren, LD, and SP). These mitigation scenarios tend to feature a widespread electrification of the global energy system, as direct combustion of fuels in buildings and vehicles are increasingly replaced with electric alternatives.

The figure below shows the energy use over time by source in the illustrative pathways (top part), as well as the amount of positive GHG emissions and CDR at the net-zero year, compared to 2019 (bottom part).

One area where there is a lot of new focus in WG3 compared to previous reports such as the 2018 SR15 is low-demand scenarios. These involve a significant decoupling of material and energy demands from economic growth, resulting in very low per capita demand for energy compared to present due to increased energy efficiency and less energy intensive lifestyles.

Illustrative pathways taking this approach – LD and SP – have the lowest peak and 2100 warming of all pathways considered, though it is unclear how possible these pathways would be to achieve in practice as they require energy efficiency improvement rates considerably above those previously experienced.

Similarly, the high level of CDR used in scenarios like Neg has large challenges; as the report notes, “CDR ramp-up rates and absolute deployment levels are tightly limited by techno-economic, social, political, institutional and sustainability constraints”.

5. How can shifting peoples’ demand for products and services cut emissions?

For the first time, this IPCC WG3 report includes a chapter dedicated to the “demand, services and social aspects of mitigation”, which explores the social science literature to assess how people’s behaviour – and the choices they are offered – can cut emissions.

“Demand-side” climate measures are those that reduce the use of high-emitting goods and services by targeting uptake of technologies and people’s consumption patterns. Examples include making it easier for people to use cleaner forms of transport, or eat more plant-based foods.

Behavioural and cultural changes represent a “substantial overlooked strategy” that have been left out of many transition pathways and scenarios, the report says.

While this means there is only medium evidence on the role they could play, it notes that there is high agreement among researchers that such changes “hold up to gigaton-scale CO2 emissions reduction potentials”.

Crucially, the SPM adds with high confidence that such efforts to reduce demand would “significantly reduce” the challenge of mitigation overall, dependence on CO2 removal (CDR, see: What does the report say about CO2 removal and solar geoengineering?), pressure on land (see: How does land add to climate change and how can it help soak up CO2?) and carbon prices needed to meet climate goals.

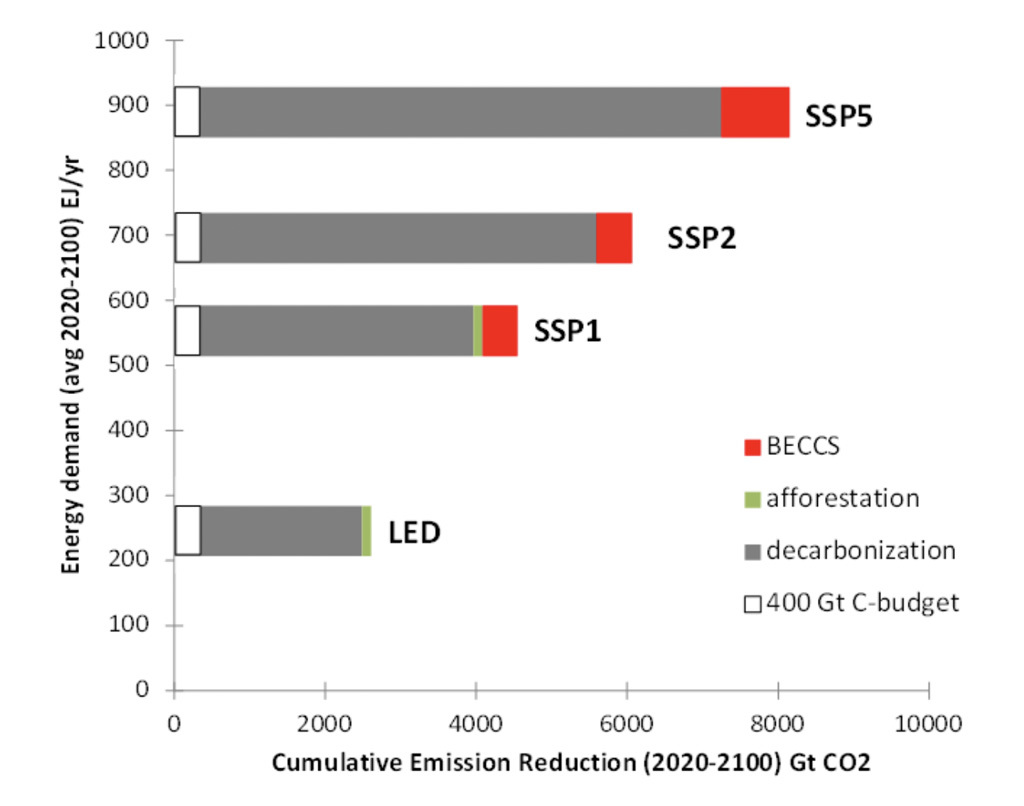

The report states that low-demand pathways “eliminate the need for technologies with high uncertainty, such as BECCS [bioenergy with carbon capture and storage]”. This can be seen in the chart below, which shows that such a scenario also requires less decarbonisation efforts than a selection of “Shared Socioeconomic Pathways” (SSPs), in order to limit warming of 1.5C.

While previous IPCC reports made little use of low energy demand scenarios, this one references 12 relevant global scenarios and another 10 that look at specific regions.

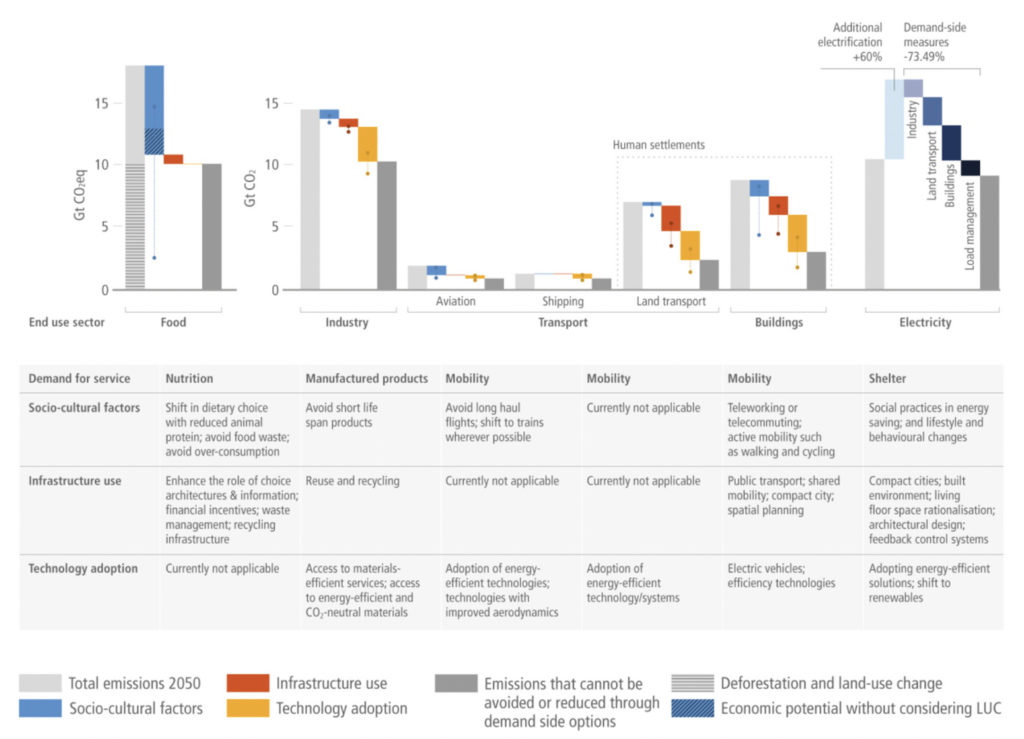

Overall, the report concludes with high confidence that, by 2050, demand-side strategies could cut global greenhouse gas emissions by 40-70% “compared to baseline scenarios”. It also notes with high confidence that Covid-19 lockdowns “demonstrated that behavioural change at a massive scale and in a short time is possible”.

The chart below shows how this could break down between sectors, with the coloured bars indicating emissions that could be avoided in 2050 by shifts in behaviours (light blue), infrastructure use (red) and clean technology adoption (orange). The dark grey bars are the remaining emissions that will not be affected by these changes.

The greatest potential – 8bn tonnes of CO2 equivalent (GtCO2e) avoided in 2050 – comes from changes in food demand (see: What impact can the food system and dietary choices have on emissions?). Land transport provides the second-biggest opportunity for emissions savings, at 6.5GtCO2e.

The report uses the avoid-shift-improve (ASI) framework to explore options for demand-side measures, through a combination of socio-cultural, infrastructural and technological changes.

In the transport sector, for example, emissions could be avoided by eliminating unnecessary travel to work and working from home instead; remaining journeys could be shifted from a car to a bus; and the bus itself could be improved by replacing it with an electric model.

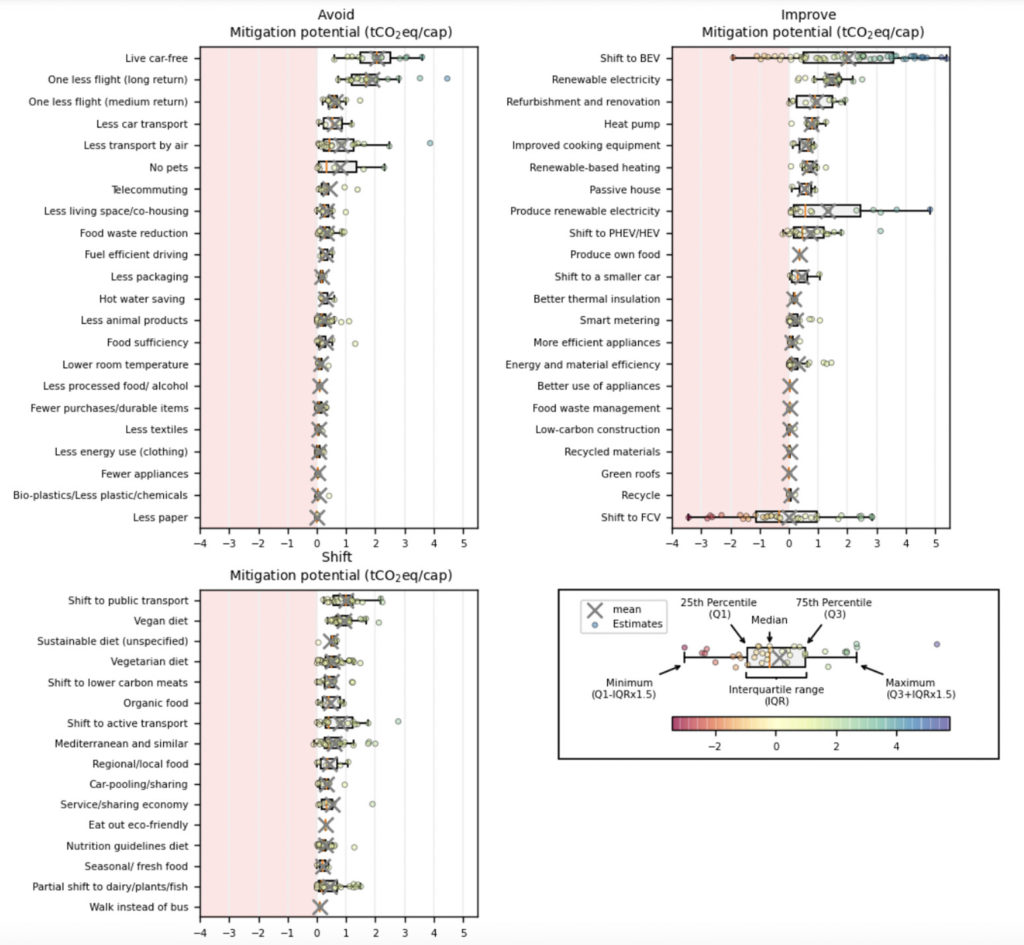

The report highlights a major review of options to reduce emissions from individual activities, which identified 6,990 journal papers and distilled 61 consumption options from them.

A breakdown of these activities and their emissions savings can be seen in the chart below. If the results extend into the pink area, this indicates that there is potential for the activity – for example switching to a hydrogen fuel-cell vehicle (FCV) – to backfire and result in more emissions.

Overall, the report notes that choosing low-carbon options could reduce an individual’s carbon footprint by up to 9tCO2. Effective “avoid” options include not using a car and cutting back on flights, effective “shifting” includes switching to plant-based diets and using public transport, and effective “improving” includes purchasing an electric car or a heat pump.

As demand-side solutions require both motivation and capacity for change – and motivation by people worldwide to change their energy consumption is “generally low” – the report states that:

“Individual behavioural change is insufficient for climate change mitigation unless embedded in structural and cultural change.”

The report says there is high evidence and high agreement that “choice architecture” – referring to interventions or “nudges” based on how choices are presented to people – can shape their energy-related decisions.

Behavioural nudges can be used to encourage the uptake of everything from food waste reduction to using geothermal for district heating, the report concludes. It highlights effective measures including “green defaults”, such as automatic enrolment in clean energy provision, and clear labelling of products with climate-relevant information.

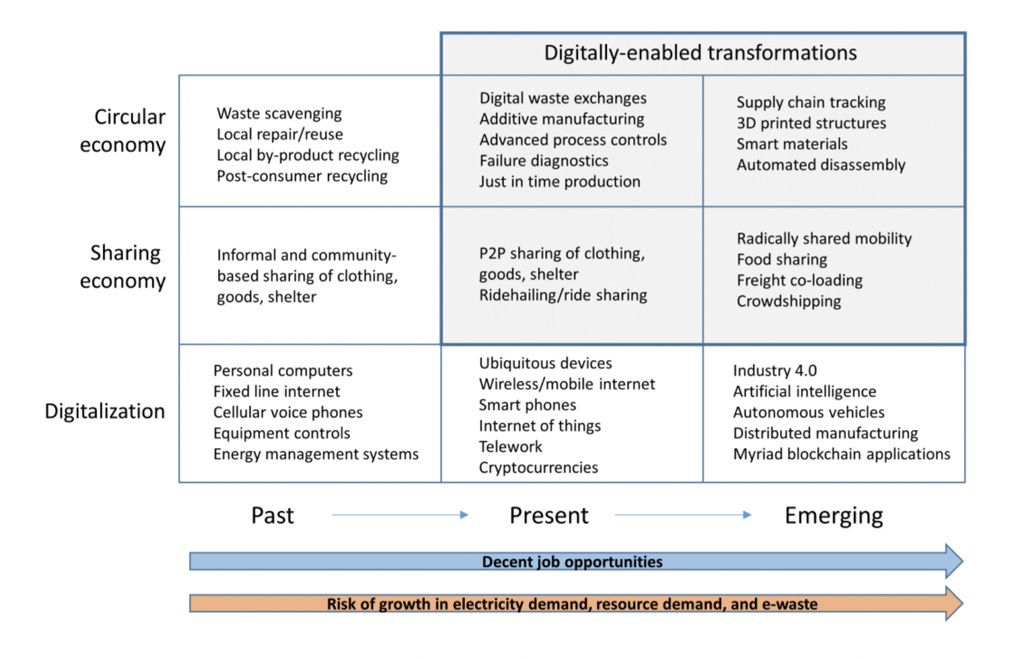

In its section on demand-side measures, the report also considers proposed “transformative megatrends”, namely the “sharing economy”, the “circular economy” and “digitalisation”. Examples of these ideas, including those that already exist and those that are emerging, are shown in the figure below.

While all of these ideas have received “much attention from the research, advocacy, business models and policy communities”, the report concludes that to date they have “made a limited contribution to climate change mitigation”. There is only medium evidence for such systems having a marked impact on emissions.

Crucially, the SPM notes with high confidence that demand-side measures are “consistent with improving basic wellbeing for all”.

A key concern about policies focused on cutting emissions is that they may reduce people’s quality of life, but the report finds, with medium confidence, that “decent living standards” – a benchmark of minimum material conditions for human wellbeing – for everyone are “achievable through the implementation of high-efficiency low demand mitigation pathways”.

The report cites a low energy demand scenario that delivers universal decent living standards while cutting final energy demand by 40% between 2018 and 2050.

It adds that addressing inequality supports climate change mitigation efforts and notes with high confidence that demand-side measures come with “multiple interacting benefits” – for example, improvements to nutrition and health.

Moreover, it says that high status – and, therefore, often high carbon – consumption patterns “may be reduced by taxing absolute wealth without compromising wellbeing”.

While the report acknowledges that “only a few” countries with low economic growth rates have cut both territorial and consumption emissions, they have done so “typically by switching from fossil fuels to renewable energy”. It adds:

“High deployment of low/zero carbon fuels and associated rapid reduction in demand and use of coal, gas and oil can further reduce the interdependence between economic growth and greenhouse gas emissions.”

6. What impact can the food system and dietary choices have on emissions?

“Food systems” are associated with roughly 42% of global greenhouse gas emissions, states the report, even as “there is still widespread food insecurity and malnutrition”. Between 1990 and 2018, greenhouse gas emissions from food systems grew from 14 to 17GtCO2e per year.

Looking at households’ carbon footprints, the food sector “dominates in all income groups”, even more than energy use. Globally, it counts for 28% of these footprints on average, with rice and cattle being the “major contributors”.

Food also accounts for 48% and 70% of household impacts on land and water resources, respectively, and these impacts rise with incomes driven by higher consumption of meat, dairy and processed food, says the report.

There is high agreement that mitigating food-sector emissions to their full potential “requires change at all stages, from producer to consumer and waste management” via integrated packages of policy including supply- and demand-side measures.

Sustainable food systems that provide healthy diets for all are within reach, state the report’s authors after assessing literature on health, diets and emissions. However, they require “significant cross-sectoral action”, from better agricultural practices, consumers changing their diets, and food producers, distributors, retailers and consumers reducing food waste.

Shifting consumption towards plant-based diets has “high mitigation potential”, says the report. There is robust evidence that “diets high in plant protein and low in meat and dairy” make for lower GHG emissions.

The report estimates with high confidence that shifts to sustainable healthy diets have a “technical potential” to reduce emissions by 3.6GtCO2e, with a range of 0.5 to 8GtCO2e. This is the amount of emissions that could be saved if financial and other constraints are ignored.

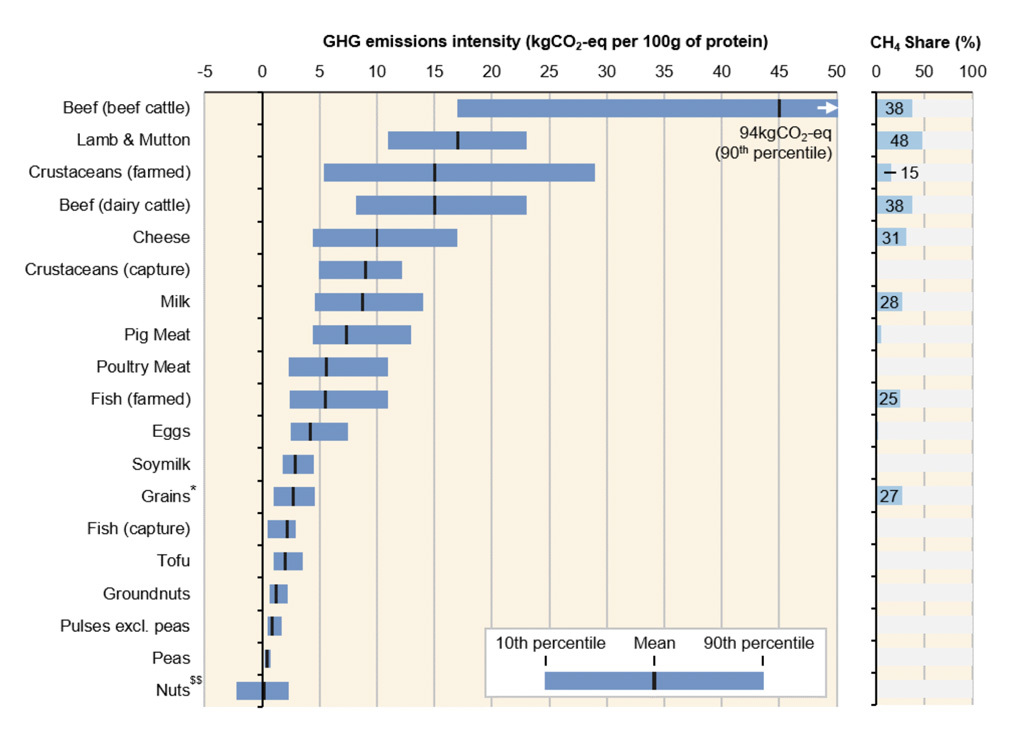

Meats from ruminants such as sheep and cows have the highest GHG intensity. However, the report observes that beef from dairy systems is less emissions-intensive than beef reared in herds purely for meat, with emissions of 8-23kgCO2e per 100g protein and 17-94kgCO2e per100g protein, respectively.

It acknowledges the widely varying estimates, attributing this to the difference in production systems: intensive livestock rearing where cattle are largely fed grain versus pastoral practices, where herders move livestock from summer to winter pastures, or rear them on rangelands.

This is illustrated in the figure below, which shows the emissions intensity of different protein-rich foods, in kgCO2e per 100g protein from the highest (beef from beef cattle) to the lowest (nuts).

In addition to “substantial[ly]” lowering emissions from the food system, diets with a higher share of plant-based protein and reduced intake of “added sugars, salt and saturated fats” would cut land use and nutrient losses to the environment, as well as offering health benefits, the report says.

Beyond dietary changes, the report says there is limited evidence – but high agreement – that a suite of “emerging technologies” could bring “substantial reduction in direct GHG emissions from food production”. These include plant-based alternatives to animal products, cultured meat and “controlled environment agriculture”, which it describes as ”hydroponic or aquaponic cultivation systems that do not require soil”.

These technologies typically have lower water, land and nutrient footprints, but as some of them are energy-intensive, they need to have access to low-carbon energy.

Food waste is another aspect the report draws attention to. According to studies assessed by the report’s authors, roughly 20-40% of food produced worldwide is wasted before it reaches the market, or goes to waste in households. It estimates that global food loss and waste accounted for 8-10% of total GHG emissions between 2010 to 2016.

Reducing food loss and waste globally has the technical potential to cut emissions globally by 2.1GtCO2e, with a range of 0.1-5.8GtCO2e, the report estimates with medium confidence.

Global food supply chains have a strong influence on per-capita food consumption emissions, particularly for red meat and dairy, the report notes, such that the highest per-capita food-related emissions “do not correlate perfectly with the income status of countries”. In other words, even relatively poorer countries may have a high per-capita food footprint.

As a result, the report says “it is crucial to focus on high-emitting individuals and groups within countries, rather than only those who live in high-emitting countries, since the top 10% of emitters live on all continents and one third of them are from the developing world”.

Changes in the food sector would have broad implications. Reducing food waste, coupled with dietary shifts, can “further reduce energy, land and resource demand” and result in “substantial” benefits in places where food is grown, putting food security there under less strain.

Both measures “have highly relevant repercussions” for land-use emissions, the report says, because they can free up land for other uses, such as afforestation or bioenergy. Moreover, shifts in diets and lowered pressure on land are also “reflected in reductions of land degradation” and reduced deforestation, says the report.

Key enablers for these shifts could include creating “novel narratives” in the media and entertainment industry to “help to break away from the established values, discourses and the status quo”. These might portray plant-based diets as healthy and natural, for example.

The report explores other measures that could be used to influence choices in the food sector, including taxes or carbon pricing on food, both of which it says would be “regressive”, meaning they disproportionately burden poorer members of society. Instead, it points to options including marketing regulations, procurement policies, dietary guidelines, labelling and “nudges”.

7. How must global energy systems change to limit warming?

The energy supply sector is the largest source of greenhouse gas emissions, accounting for some 20GtCO2e or 34% of the total in 2019, the report says. It states with high confidence:

“Warming cannot be limited to 2C or 1.5C without rapid and deep reductions in energy system CO2 and GHG emissions.”

This means it is “essential” to cut energy supply sector emissions in order to limit warming and, consequently, the energy systems of the future will be “very different”. It adds: “Achieving and responding to these changes presents an impressive range of challenges and opportunities.”

Some 4GtCO2e of the sector’s emissions are due to fugitive emissions from fossil fuel production, which are potentially “underestimated” and remain subject to a “high degree of uncertainty”.

However, the largest share – some 14GtCO2e – relates to the generation of electricity and heat. These emissions must be all but eliminated even as demand increases, it says, because all scenarios staying below 2C involve “increased electrification of buildings, transport and industry”.

(In scenarios limiting warming to 2C, electricity’s share of final energy increases from today’s level of 20% to at least 42% in 2050 and 60% in 2100, with even higher levels for 1.5C.)

While the challenge is large, the report says that a shift to low-carbon energy could save money, thanks to rapid cost reductions in key technologies over the past decade. (See: How much innovation and new technology is needed to hit climate goals?) It states:

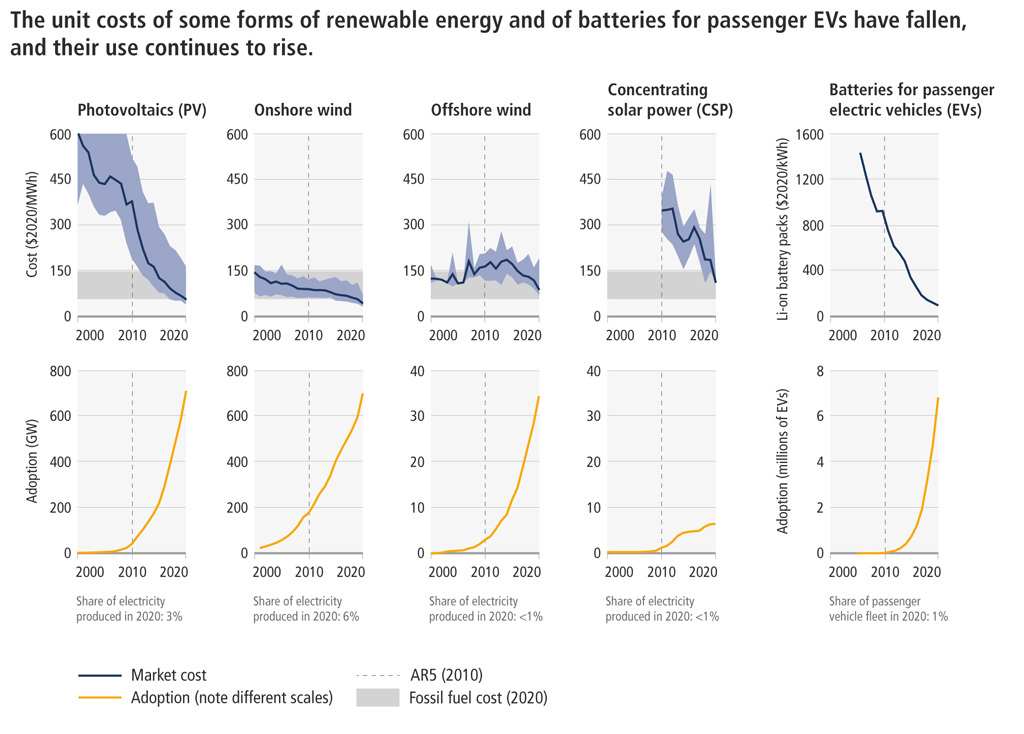

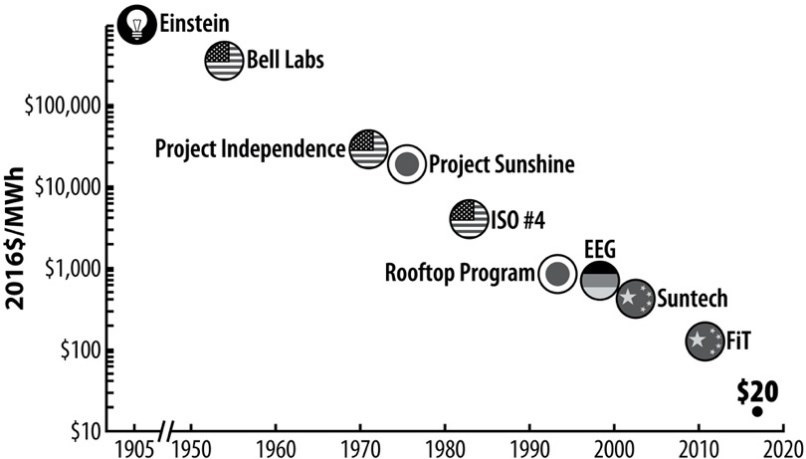

“Unit cost reductions in key technologies, notably wind power, solar power, and storage, have increased the economic attractiveness of low-emission energy sector transitions through 2030. Maintaining emission-intensive systems may, in some regions and sectors, be more expensive than transitioning to low-carbon systems. Low-emission energy sector transitions will have multiple co-benefits, including improvements in air quality and health.”

These cost reductions mean that in “many parts of the world”, solar power is cheaper than electricity from fossil fuels and in “some” places below the cost of continuing to operate existing coal or gas power plants, the report says with high confidence. Similarly, it says that electricity from onshore wind is cheaper than from fossil fuels “in a growing number of markets”.

Moreover, the report says with medium confidence that evidence has emerged since the previous fifth IPCC assessment report (AR5) suggesting that “future energy transitions may occur more quickly than those in the past”.

One stumbling block highlighted by the report is the weight of emissions likely to be created by existing and currently planned fossil fuel infrastructure. It warns:

“Estimates of future CO2 emissions from existing fossil fuel infrastructures already exceed remaining cumulative net CO2 emissions in pathways limiting warming to 1.5°C (>50%) with no or limited overshoot (high confidence).”

Given the “long lifetimes” of these assets, they “may influence the rate of transformation substantially and lock societies into carbon-intensive lifestyles and practices for many decades”. It adds:

“Decommissioning and reduced utilisation of existing fossil fuel installations in the power sector as well as cancellation of new installations are required to align future CO2 emissions from the power sector with projections in these pathways.”

If warming is kept below 2C, fossil fuel resources and fossil fuel-related infrastructure “could” be “strand[ed]”, the report says, though it adds that the use of CCS, where available, “could allow fossil fuels to be used longer” and reduce the risk of stranding.

It says, with medium confidence, that the combined discounted value of these assets is projected to be around $1-4tn between 2015-2050 and “will be higher” if warming is kept below 1.5C. Coal assets would be most at risk this decade but oil and gas would be too, “toward mid-century”.

The report says that limiting warming to 2C or below “requires a rapid shift” away from coal use without carbon capture and storage (CCS), and will “require cancellation of new coal power projects and accelerated retirement of existing coal plants”. Opportunities for more rapid action this decade also include “limiting the construction of new gas-fired power plants”, it adds.

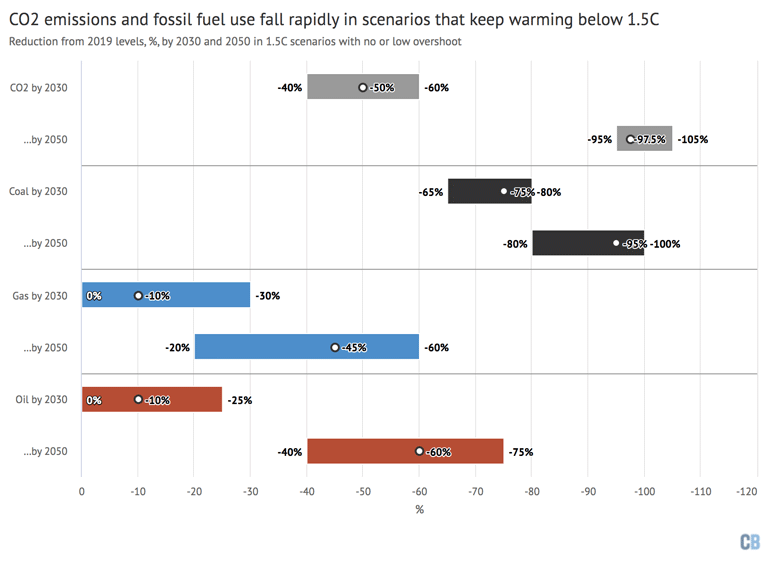

The Carbon Brief figure below shows how global CO2 emissions and primary energy supply from fossil fuels falls rapidly in scenarios that keep warming below 1.5C with no or limited overshoot.

Indeed, the report says that using “far less fossil fuel than today” is “fundamental” to limiting warming. Specifically, coal use falls to 75% below 2019 levels by 2030 and 95% by 2050 (black bars), while gas falls 10% by 2030 and 45% by 2050 (blue), and oil by 10% and 60% (red).

Although there are many different pathways to keeping warming below 2C, the report points to a number of key characteristics that are shared across all such scenarios. These include:

- Electricity systems that produce no CO2 or remove it from the atmosphere;

- Widespread electrification including for “light-duty” transport, heating and cooking;

- “Substantially” lower fossil fuel use than today;

- Use of alternative “energy carriers”, such as hydrogen, bioenergy and ammonia, in sectors where electrification is not possible;

- More efficient use of energy than today;

- Greater integration between different parts of the energy system, such as heating, transport and electricity, as well as between regions;

- Use of carbon dioxide removal (CDR) to offset residual emissions.

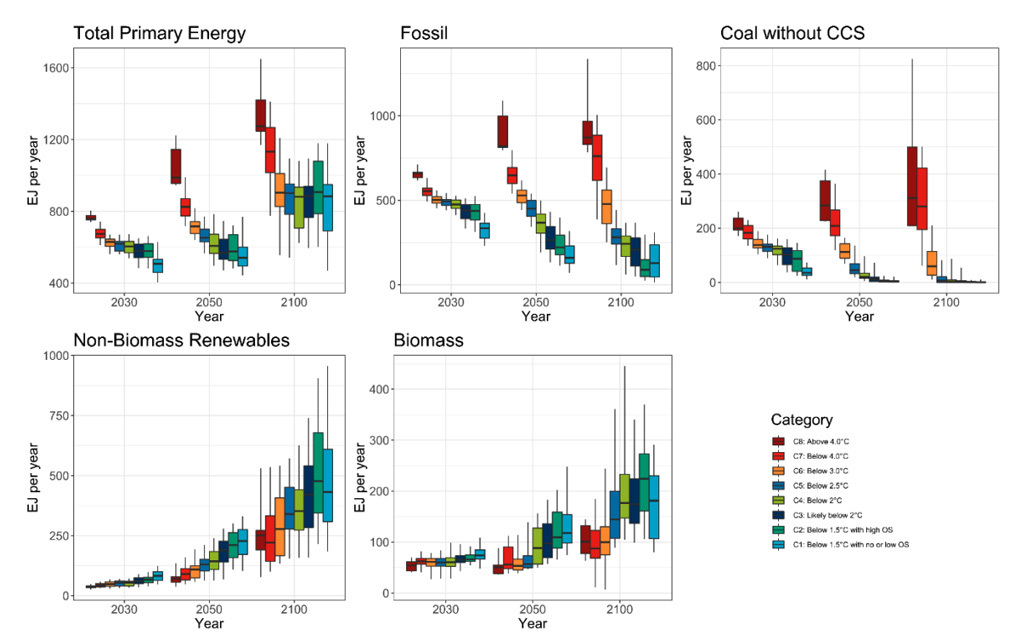

These are illustrated in the figure below, which shows how the energy system changes under a range of scenarios from high warming (red bars) to those staying below 1.5C (blue). The figure shows global primary energy supply (top left) and contributions from fossil fuels (top middle), coal without CCS (top right), non-biomass renewables (bottom left) and biomass (bottom middle).

The report says that pathways successfully limiting warming “show reductions in energy demand” compared with current policies, through a “diverse set of demand-side interventions”. (See: How can shifting peoples’ demand for products and services cut emissions?)

At the same time, low-carbon energy sources increase rapidly in below-2C pathways, meeting 88% of primary energy supply (with a range of 69-97%) in 2100.

Renewable energy, including wind, solar and bioenergy, supplies 30-70% of energy in below-2C pathways and “clearly above 40%” for 1.5C, the report says.

It notes that while scenarios have been published with 100% renewable energy at a global scale, there is “debate in the literature on whether [this] is possible to achieve”. It adds:

“It is unlikely that all low-carbon energy systems around the world will rely entirely on renewable energy sources.”

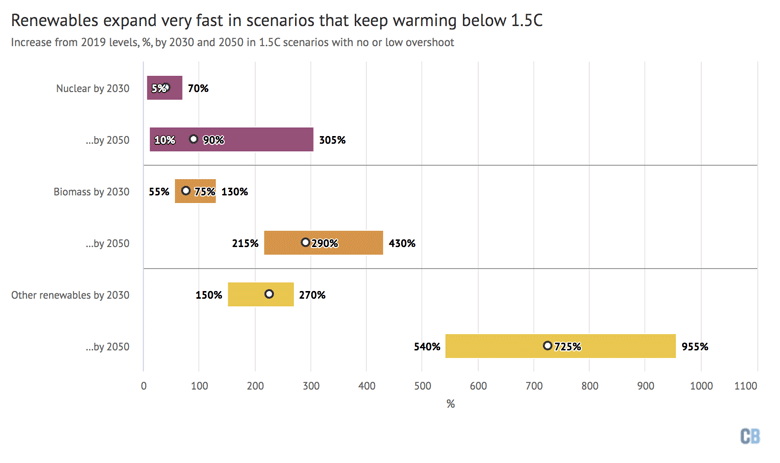

Regardless of these debates, non-biomass renewable energy – primarily wind and solar – expands very fast in scenarios keeping warming below 1.5C with no or limited overshoot, as shown in the figure below (yellow bars). In contrast, 1.5C scenarios show greater variation in the adoption of nuclear and biomass energy, the report shows (purple and orange bars).

The contribution of biomass has “absolute limits”, the report says. (See: How does land add to climate change and how can it help soak up CO2?)

It says with high confidence that nuclear “can deliver low-carbon energy at scale”, but that doing so “will require improvements in managing construction of reactor designs that hold the promise of lower costs and broader use”. It adds:

“[N]uclear power continues to be affected by cost overruns, high upfront investment needs, challenges with final disposal of radioactive waste, and varying public acceptance and political support levels (high confidence).”

In contrast to the rapid recent cost reductions and adoption of “modular” technologies, such as wind, solar and batteries, which have happened “much faster than anticipated by experts and modelled in previous mitigation scenarios”, the report says that nuclear energy and CCS has been “slower than…anticipated”.

Moreover, it says with medium confidence that evidence since AR5 indicates “small-scale technologies (e.g. solar, batteries) tend to improve faster and be adopted more quickly than large-scale technologies (nuclear, CCS)”.

Another important technology is CCS, with a “considerable amount” being used in the “majority” of below-2C scenarios, the report says. Notably, however, some of the 1.5C pathways highlighted by the report include little or no CCS. (See: What would it take to limit warming to 1.5 or 2C?)

Box TS.9 in the Technical Summary compares hydrogen to electrification in areas such as transport, heating and industry. It says:

“As a general rule, and across all sectors, it is more efficient to use electricity directly and avoid the progressively larger conversion losses from producing hydrogen.”

Box TS.9 in the Technical Summary compares hydrogen to electrification in areas such as transport, heating and industry. It says:

“As a general rule, and across all sectors, it is more efficient to use electricity directly and avoid the progressively larger conversion losses from producing hydrogen.”

Nevertheless, as Box 12.5 explains, there has been growing interest in the use of the fuel, with the word “hydrogen” appearing five times more often in AR6 than AR5. It points to the use of hydrogen in sectors that are hard to decarbonise, such as parts of transport and industry, as well as for storage in low-carbon electricity systems.

The report also addresses a range of challenges for low-carbon energy systems to overcome. For example, it says that integrating large amounts of “variable renewable energy” (VRE), particularly wind and solar, presents “economic and technical challenges to electricity system management”.

These challenges “can be addressed” by using batteries, hydrogen and other storage, as well as greater “demand-side responses”, it says, meaning that “[e]lectricity systems powered predominantly by renewables will be increasingly viable over the coming decades”.

Furthermore, the addition of “flexible/dispatchable” generation technologies, such as gas, hydrogen or nuclear plants, can “enabl[e] more secure and cost-effective integration of VRE generation and end-use electrification”, the report adds.

While expansion of solar, wind and EVs will increase demand for critical minerals, the report says “there are alternatives” and that recycling can boost supplies. The report also gives short shrift to the idea that wind power is not low carbon, saying that “all wind power technologies repay their carbon footprint in less than a year”.

Finally, the report says that while climate change will alter hydropower output, bioenergy yields, the efficiency of fossil and nuclear power plants, and demand for heat and cooling, it “will not affect wind and solar resources to the extent that it would compromise their ability to reduce emissions”.

8. How does land add to climate change and how can it help soak up CO2?

Around 22% of global greenhouse gas emissions came from agriculture, forestry and other land use (AFOLU) in 2019, the report says.

The proportional contribution of AFOLU to total emissions varies regionally, the report says. It is highest in Latin America and the Caribbean, where 58% of total emissions come from AFOLU and lowest in Europe and North America, where 7% of emissions come from AFOLU.

CO2 emissions from AFOLU are largely driven by land-use change, with deforestation accounting for “about half” of total emissions, the report adds.

It says with medium confidence that levels of deforestation generally declined between 2010 and 2019. However, over this time, there were overall losses in tropical forests – which are key for carbon storage and biodiversity – and gains in temperate and boreal regions.

The loss of mangrove forests – coastal swamps found in the tropics that hold vast stores of carbon – has been particularly severe over the past few decades, the report says.

From 1990 to 2020, one million hectares of mangrove forests were lost across the world, largely due to conversion for agriculture and aquaculture, according to the report. (There are around 15m hectares of mangrove forests globally.)

In 2020, the total global forested area stood at 4bn hectares, representing 31% of the total Earth surface, it adds. Countries with the most forest within their borders include Russia, Brazil, Canada, the US and China.

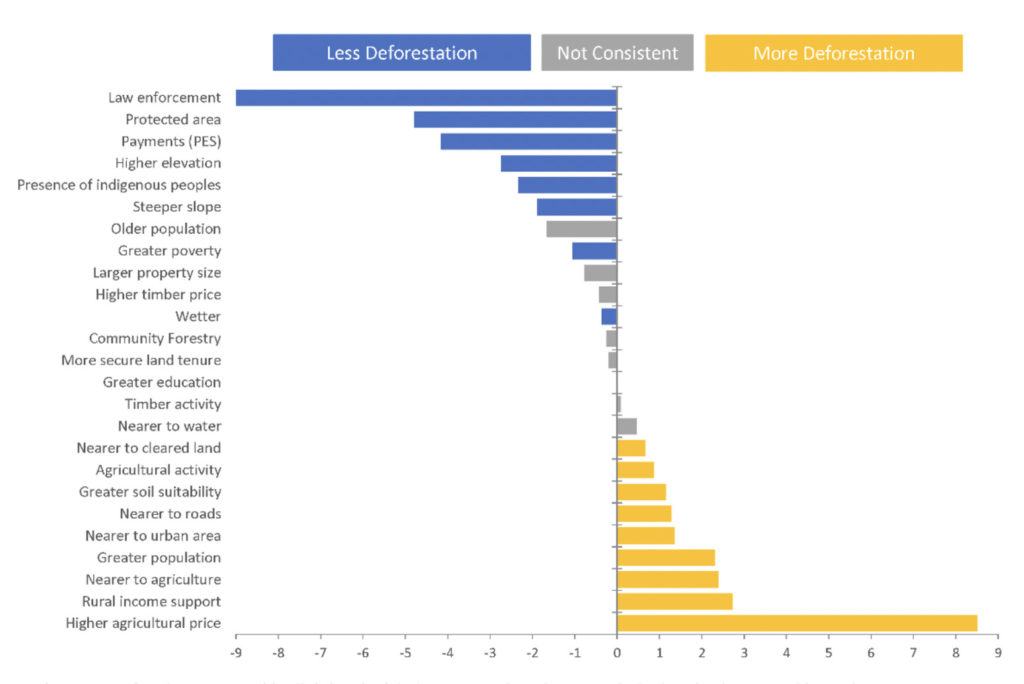

The chart below explores the drivers of higher deforestation and lower deforestation, based on a global scientific review published in 2017.

The analysis explored whether drivers were consistently associated with higher deforestation (yellow), lower deforestation (blue) or neither (grey). Results are given in ratios. (For example, a ratio of -4 indicates that a driver is associated with lower deforestation four times as often as it is associated with higher deforestation.)

The chart shows that factors such as law enforcement, protected areas, payment for ecosystem services and the presence of Indigenous people were consistently associated with lower levels of deforestation.

By contrast, higher agricultural prices and close proximity to agriculture, urban areas and roads were consistently associated with higher levels of deforestation.

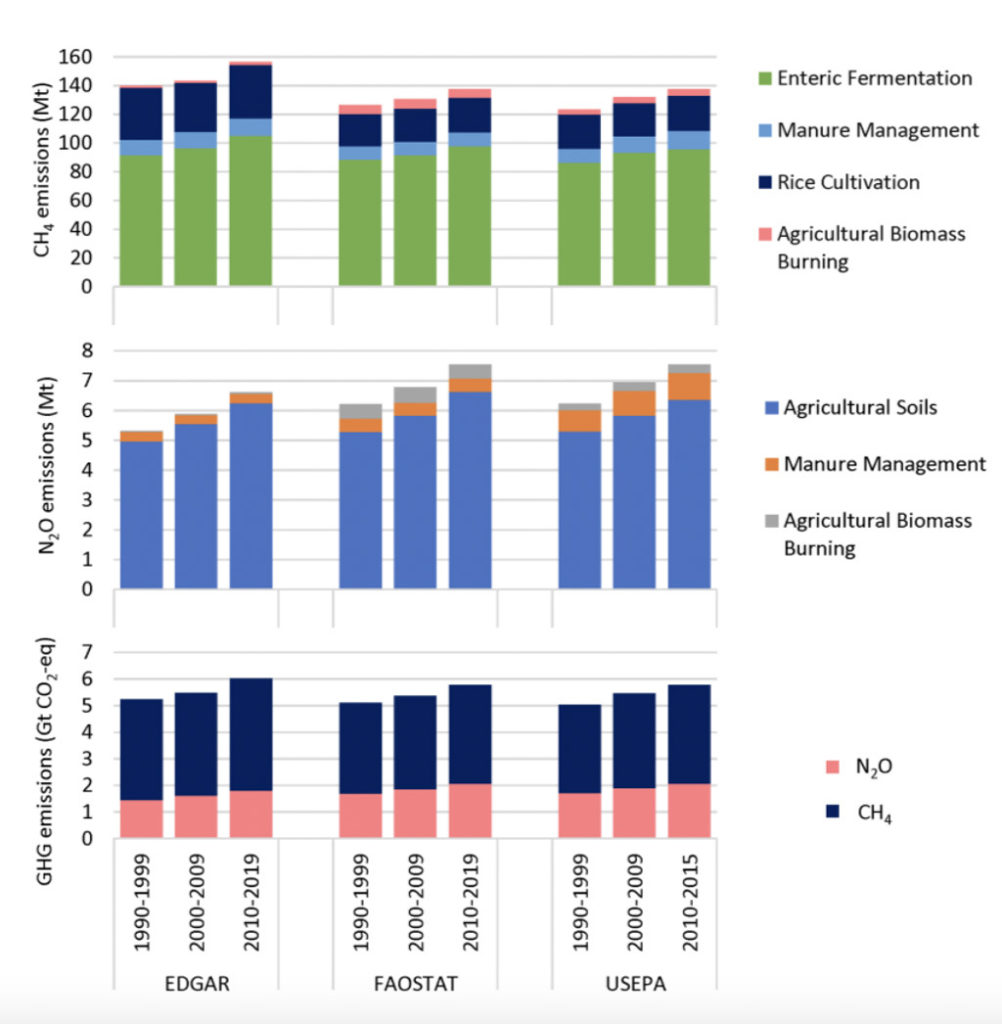

In addition to CO2, the report also examines how the AFOLU sector is driving emissions of the second- and third-most polluting greenhouse gases, namey, methane and nitrous oxide.

Methane emissions from AFOLU increased between 2010 and 2019, with the “main source” being belching and manure production from livestock, the report says with high confidence.

Nitrous oxide emissions are also on the rise, “dominated by agriculture, notably from manure application, nitrogen deposition and nitrogen fertiliser use”, the report says with high confidence.

The chart below shows estimated global mean agricultural methane (top) and nitrous oxide (middle) emissions for the period 1990 to 2015, based on three different data sources (EDGAR, FAOSTAT and USEPA). The bottom chart shows an aggregation of global mean agricultural methane and nitrous oxide emissions.

On the top chart, green represents methane emissions from “enteric fermentation” (the digestive process of cows and sheep), light blue represents manure management, dark blue represents rice cultivation and orange represents agricultural biomass burning.

On the middle chart, blue represents nitrous oxide emissions from agricultural soils, orange from manure management and grey from agricultural biomass burning.

(Read Carbon Brief’s in-depth breakdown of the emissions of different types of food.)

Despite dramatic land-use change, the world’s intact terrestrial ecosystems acted as a carbon sink between 2010 and 2019, absorbing around a third of all human-caused CO2 emissions, the report says with medium confidence.

The report says that the AFOLU sector offers “significant opportunities” for tackling climate change while providing food, wood and other resources – if it can adapt to the impacts of warming.

It states with high confidence that rapid deployment of land-based measures for reducing emissions is “essential in all pathways” for keeping global warming to 1.5C.

There is “robust evidence” that the AFOLU sector could provide 20-30% of the global greenhouse gas reductions needed for a 1.5C or 2C pathway by 2050, the report says. However, it notes that strategies for how AFOLU can help achieve climate targets are “highly variable” (see: What would it take to limit warming to 1.5 or 2C?)

AFOLU’s contribution to climate targets could come at a “relatively low cost”, the report adds.

It says the AFOLU sector could “economically” remove 8-16GtCO2e every year between 2020 and 2050. This “economic potential” is roughly half the “technical potential” from AFOLU – an estimate of what would technically be possible when constraints such as financing are not considered, the report says.

From now to 2050, protecting and restoring forests and other ecosystems could have the highest potential for economic greenhouse gas removal related to AFOLU, the report says.

Global studies suggest that the protection and restoration of forests, peatlands, coastal wetlands, savannahs and grasslands have the potential to cut emissions by a mean of 7.3GtCO2e per year from 2020 to 2050, the report says.

Agricultural means of reducing emissions, such as soil carbon management and improved livestock rearing, offer the second-largest potential for economic CO2 removal from AFOLU, it says. Such methods could cut emissions by 4.1GtCO2e per year, according to the report.

“Demand-side” measures, such as shifting to plant-based diets and reducing food waste, offer the third largest potential: 2.2GtCO2e a year.

The above measures for slashing AFOLU’s climate impact are “available and ready to deploy”, the report adds, in contrast to other types of CO2 removal, such as carbon capture and storage (CCS), the report adds. (See: What does the report say about carbon dioxide removal?)

“Bioenergy” methods – which involve the burning of crops and wood residues to produce energy – also represent an “important share” of the total greenhouse gas removal potential from AFOLU, the report says.

Bioenergy with carbon capture and storage (BECCS) – a still-emerging technique that involves growing crops, burning them in a power station to generate energy and then capturing the resulting CO2 – could remove an estimated average of 5.9GtCO2e each year from 2020 to 2050, the report says with medium confidence.

However, out of this figure, just 1.6GtCO2e could be removed in a way that is economic, the report adds. With high confidence, the report adds:

“The use of bioenergy can lead to either increased or reduced emissions, depending on the scale of deployment, conversion technology, fuel displaced, and how, and where, the biomass is produced.”

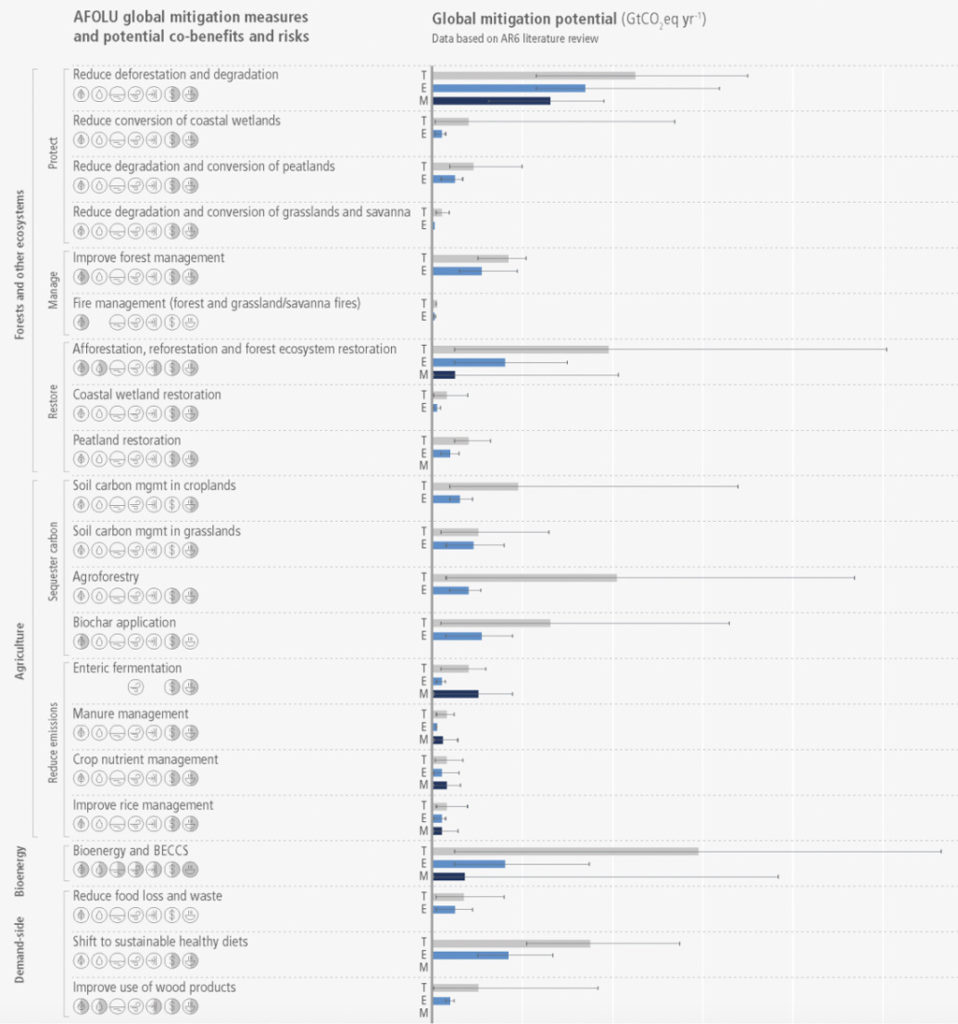

The graphic below shows the global mitigation potential (in billion tonnes of CO2e per year) of 20 land-based climate measures between 2020 and 2050. On the chart, grey bars represent technical potential, light blue bars represent economic potential and dark blue bars represent economic potential according to integrated assessment models (IAMs).

On the graphic, icons represent co-benefits (white) and risk (shaded) for biodiversity, water, soil, air quality, resilience, livelihoods and food security. (Half-shaded icons indicate there is the potential for risks and co-benefits.)

The report says that, when “carefully” implemented, land-based measures for reducing greenhouse gas emissions are “uniquely positioned to deliver substantial co-benefits and help address many of the wider challenges associated with land management”.

However, when deployed “badly”, land-based climate measures can “exacerbate trade-offs with the conservation of habitats, adaptation, biodiversity and other services”. The report adds:

“Depending on local conditions and management strategies, mitigation measures have the potential to positively or negatively impact biodiversity, ecosystem functioning, air quality, water availability and quality, soil productivity, rights infringements, food security, and human wellbeing.”

It states with high confidence that “poorly planned” deployment of biomass production and large-scale tree-planting may “conflict with environmental and social dimensions of sustainability” – echoing the findings of the second working group report of AR6. (On the graphic above, bioenergy and BECCS are found to pose a risk to biodiversity, water, soil, air quality, resilience, livelihoods and food security.)

The report says that, when food security and environmental concerns are considered, bioenergy has the potential to produce 5-50EJ per year and 50-250EJ per year by 2050 for residues and dedicated biomass production systems, respectively. (250EJ per year is equivalent to around 40-45% of current global primary energy demand.)

The report notes that most land-based measures for reducing emissions, such as tree-planting and restoring ecosystems, “have been well understood for decades but deployment remains slow”.

It says that the “economic and political feasibility” of land-based climate measures are “hampered by persistent barriers”.

A lack of available finance “forms a critical barrier” to the rollout of land-based climate measures, the report says.

“Differences in cultural values, governance, accountability and institutional capacity are also important barriers,” it adds.

“Concerted, rapid and sustained effort by all stakeholders, from policymakers and investors to land owners and managers” will be needed if land-based climate measures are to be deployed at the level necessary, the report says with high confidence.

The world currently spends $700m on land-based climate measures each year – well short of the $400bn needed if the AFOLU sector is to deliver up to 30% of the CO2 cuts needed to meet climate targets, the report says with medium confidence. “This estimate of the global funding requirement is smaller than current subsidies provided for agriculture and forestry,” the report adds.

It adds that the deployment of land-based climate measures “depends strongly” on policies that directly address emissions. Examples of “successful policies” include community forestry, biodiversity conservation and payments for ecosystem services.

9. What does the report say about CO2 removal and solar geoengineering?

Methods for removing CO2 from the atmosphere are “unavoidable” if the world is to reach net-zero – both globally and nationally, the report says.

It states with high confidence that net-zero can only be achieved if CO2 removal is used to balance “difficult-to-abate” emissions from sectors that will find it harder to slash their climate impact, such as aviation, agriculture and some industrial processes.

In the longer term, upscaling CO2 removal could provide “net-negative CO2 emissions at the global level”, allowing a “reversal of global warming”, the report says with medium confidence.

However, the role of CO2 removal is often “inflate[d]” in model pathways designed to show how the world could limit warming. This is because of “insufficient representation of variable renewables” such as wind and solar, limited use of demand-side options (see: How can shifting peoples’ demand for products and services cut emissions?) and high discount rates.

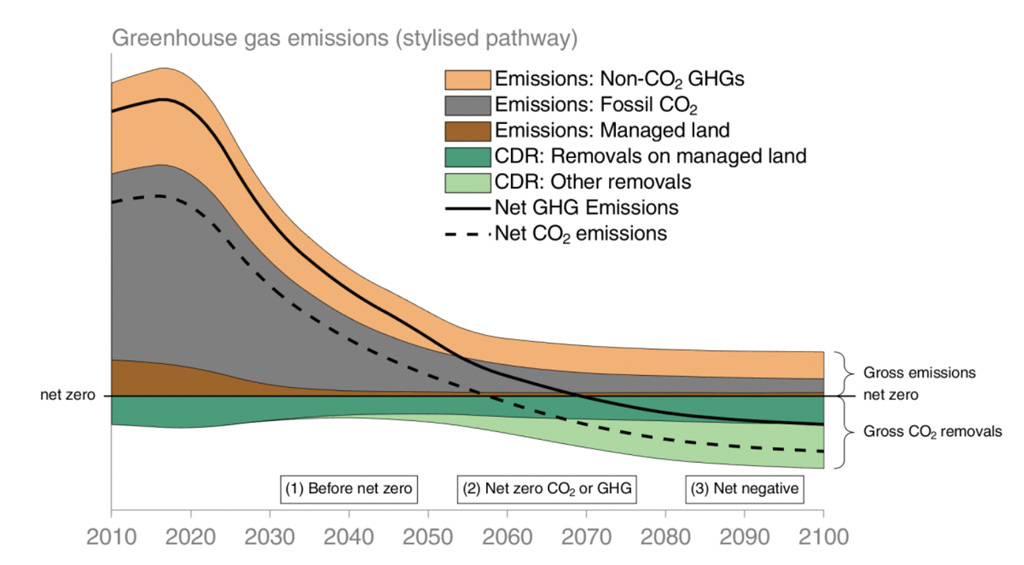

The chart below shows the role of CO2 removal (“CDR”) in a stylised pathway of ambitious climate action. Dark green illustrates CO2 removal from land-based methods and light illustrates removal from ocean and technological methods.

According to the report, it illustrates how CO2 removal could help to reduce greenhouse gas emissions levels in the near-term (1), counterbalance residual emissions to help reach net-zero in the mid-term (2) and help achieve net-negative emissions in the long term (3).

Methods for CO2 removal range from the biological, such as tree-planting and BECCS (see: How does land contribute to climate change and how can it help to soak up CO2?), to the chemical, such as using machines to suck CO2 from air (direct air capture and storage), the report notes. Each method’s ability to store CO2 ranges from “decades to more than 10,000 years”, it adds.

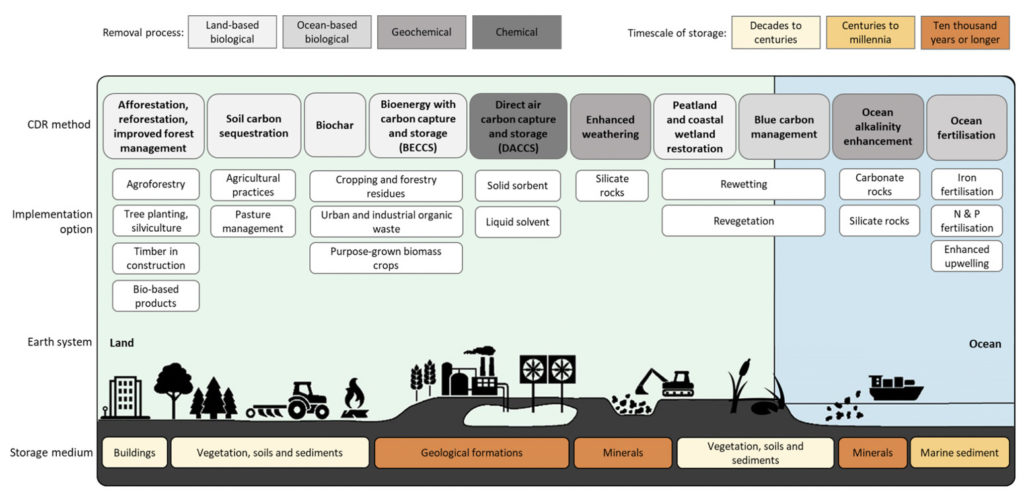

The graphic below sums up various land- and ocean-based methods for removing CO2 from air, including possible implementation and storage options.

(See Carbon Brief’s in-depth explainer of the various methods for removing CO2 from the atmosphere.)

All pathways for limiting global warming to 1.5C and 2C use land-based CO2 removal methods, such as tree-planting, many use BECCS and some include direct air capture and storage, the report says.